Rocket Stock Is the New Meme Trade. Move Over, GameStop.

Rocket, the parent of Quicken Loans, has surged 28% this week.

By Orla McCaffrey

Thu, Mar 4, 2021 12:40am 4 min

4 min

4 min

Rocket, the parent of Quicken Loans, has surged 28% this week.

4 min

The individual investors that powered GameStop Corp.’s meteoric rise have a new target: Rocket Cos., the parent company of Quicken Loans.

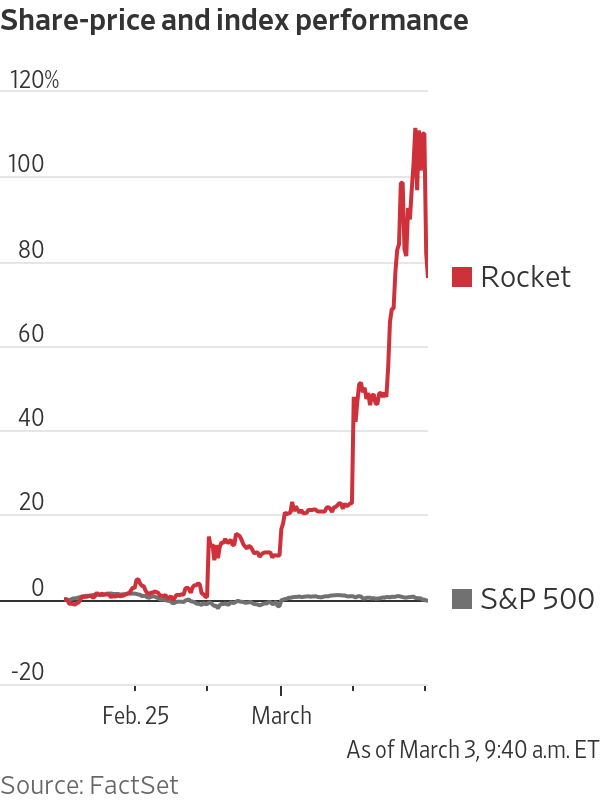

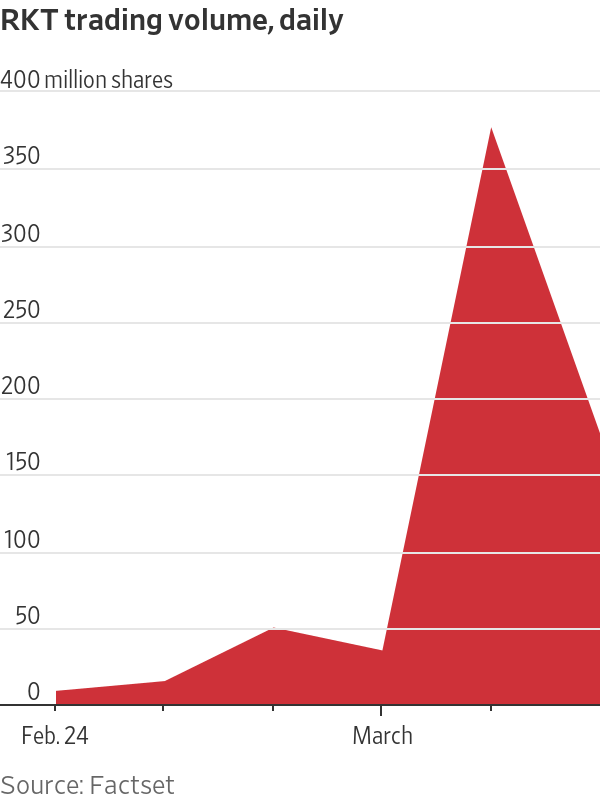

Shares of the mortgage lender surged 28% since the end of last week. Nearly 377 million shares traded hands on Tuesday alone, more than a 10-fold increase from the previous day. After surging 71% on Tuesday, the stock lost some steam on Wednesday, falling 33%, or $13.59, to $28.01.

Like GameStop, Rocket is heavily shorted. As of this week, 46% of its shares available for trading were being shorted by investors betting the price would fall, according to S3 Partners, a data-analytics firm. That was up from about 33% in late January and 17% in mid-September, according to FactSet.

Trading of Rocket shares was halted several times this week because of its volatility.

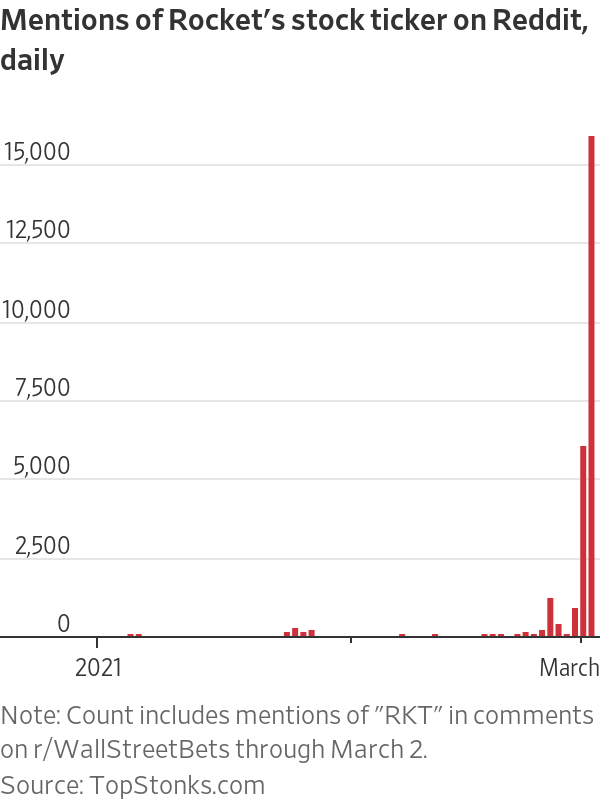

Individual investors on WallStreetBets, the Reddit community that gave birth to GameStop’s rise, have been encouraging each other to buy the stock in recent days and sharing evidence of their own massive gains. They have relished in the company’s name——Rocket——an apt one for their goal of higher prices.

“The $RKT is fueled and ready for liftoff,” one user wrote early this week.

The company stock symbol, RKT, was mentioned in nearly 16,000 Reddit comments on Tuesday, according to data from TopStonks.com, a website that tracks equities mentioned on Reddit. That is up from just over 6,000 on Monday and less than 1,000 on most days last week.

Rocket announced last week it would pay a one-time dividend of $1.11 per share later this month, citing its “highly profitable and capital light business model.” Some investors saw the move as a way to fend off short sellers. Short sellers are obliged to pay any dividends to the broker they borrowed shares from.

The company’s excess capital at the end of the fourth quarter made the dividend possible, Rocket CEO Jay Farner said at a conference Wednesday morning.

“We were pretty proud to be able to offer that to our shareholders,” Mr Farner said. “We think more of dividends as special dividends because we want that flexibility to make the right investment for the long-term growth of the organisation.”

Rocket has other upsides. Rising mortgage rates are boosting earning potential for mortgage lenders just as the crucial spring home-selling season kicks off. The average rate on the 30-year fixed-rate mortgage rose to 2.97% recently, its highest level since August.

Detroit-based Rocket is the largest mortgage lender in the U.S., according to research firm Inside Mortgage Finance. Its $323 billion in home loans in 2020 easily surpassed the $221 billion originated by its closest competitor, Wells Fargo & Co. Its large size and strong brand—it ran two Super Bowl commercials—set it apart from other non-bank lenders.

Before Rocket’s blastoff, shares of nonbank mortgage lenders had done little to impress investors in recent months. Some of the lenders that listed their shares on the public market in recent months significantly downsized their offerings. Some never made it to market because of tepid investor interest.

Shares of Rocket hadn’t strayed too far from their listing price of $18 in the seven months since the company’s IPO. The stock soared to more than $31 in its first month but quickly returned to near $20.

The first sign of liftoff came late last week, when Rocket reported impressive fourth-quarter results. Shares rose almost 10% on Friday. The news of a sizable dividend prompted Rocket’s initial jump in stock price, said KBW analyst Bose George.

“The initial move made some sense, but since then, fundamentals haven’t been driving it,” Mr George said. “It’s other factors that we have a harder time assessing.”

Shortly before its public-market debut last summer, Rocket announced an ambitious expansion target: cornering 25% of the mortgage market over the next decade. Its market share currently stands at about a third of that, according to Inside Mortgage Finance.

Rocket said last week that its mortgage originations more than doubled in 2020. It said it expects continued high origination levels despite weakening margins.

The amount lenders earn when they sell each loan has started to drop. Quicken’s gain-on-sale margin was 4.41% in the fourth quarter, down from the third quarter but well above the 3.41% it recorded a year earlier. It expects its first-quarter margin to be between 3.6% and 3.9%.

Cleveland Cavaliers owner Dan Gilbert helped found Quicken Loans in the 1980s and still holds the majority of its shares.

Ali Habhab has watched the stock’s recent ride with interest but doesn’t plan to sell his shares any time soon. Mr. Habhab, who is 25 years old, instead hopes his returns will bring him closer to his goal of retiring at 40. He bought 1,000 shares in Rocket shortly after the company’s IPO in August.

Mr. Habhab, who works in automotive manufacturing, said he was familiar with Quicken Loans long before parent company Rocket decided to go public. Mr. Habhab lives in Detroit, where Rocket is based, and has friends who started careers at the company or one of its subsidiaries.

“With all that factored in, it was a no-brainer to put some of my money where it belongs and where it will grow,” Mr Habhab said.

Another major nonbank mortgage lender, UWM Holdings Corp. is up 27% so far this week.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.