Asics Stock Catches Fire Along With Its Dad Sneakers

Shares in the Japanese running-shoe maker have just about quadrupled

By JACKY WONG

Mon, Jun 3, 2024 9:06am 3 min

3 min

3 min

Shares in the Japanese running-shoe maker have just about quadrupled

3 min

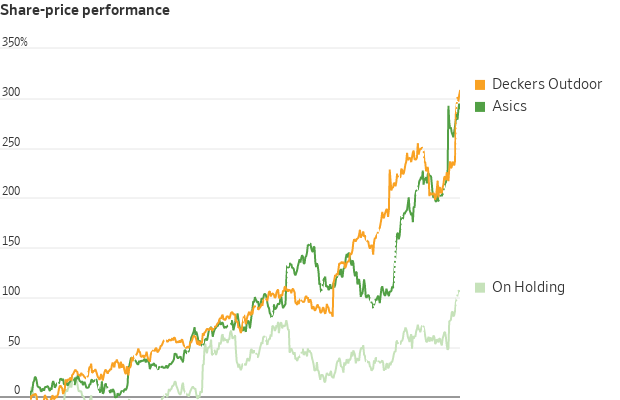

The running-shoe maker’s stock price has quadrupled in total return terms over the past two years. Its financial performance is strong: Revenue in its last reported quarter grew 14% from a year earlier while its operating profit surged 53%.

Asics has long been a well-loved brand among the running community. Around a quarter of 54,000 runners who finished the Paris Marathon sported a pair of Asics, including both winners in the men’s and women’s races, according to the company.

In fact, even Nike can trace its roots back to the Japanese company. Nike began its business in the 1960s by importing and distributing shoes from Asics, then known as Onitsuka, in the U.S. Onitsuka Tiger remains a high-end fashion brand within Asics.

Asics has benefited from the Covid-19 pandemic: More people picked up running as a hobby when they had nothing else to do. At the same time, people working from home began giving priority to comfort in their footwear—discovering that lightweight shoes with cushioned soles designed for running are pretty comfortable for walking around in, too. Running-shoe upstarts such as Hoka and On Holding have also seen explosive growth in the past few years. Hoka’s sales in the quarter ended in March surged 34% from a year earlier, pushing shares of its owner , Deckers Outdoor , to record highs.

The performance running shoes segment is Asics’ largest by revenue, and it has tried to maintain a close-knit community of runners. Asics acquired Runkeeper, a popular fitness-tracking app among runners, in 2016. In recent years, it has been acquiring race-registration companies, including Njuko Sas in Europe and Register Now in Australia. Its loyalty program has nearly 15 million members globally.

But outside of runners and Onitsuka Tiger, Asics was perhaps best known for “dad sneakers” —a style of shoes that are picked more for practicality than aesthetics. Lately, however, some old Asics designs have become unlikely fashion symbols. Youngsters have apparently eschewed conventional beauty standards and embraced the uncool: Crocs and Hoka are some other examples of “ugly shoes” that have seen an explosion in popularity .

Asics has done its fair bit, too. Its collaboration with designers from Vivienne Westwood to Cecilie Bahnsen have generated lots of buzz on social media. For example, its redesign of its 2008 Gel-Kayano 14 sneaker with Canadian design studio JJJJound has been a smash hit . The shoe can sell for more than $1,000 on online marketplace StockX. Asics was the fifth most-traded brand on StockX last year, rising from No. 10 the year before. Revenue for the company’s more fashion-minded SportStyle division grew 52% year over year in the last reported quarter.

Even better news for investors is that the company has been more profitable, too. Operating margin in its quarter ended in March was 19.4%, compared with 9.5% two years earlier. Partly that is because the company has shifted its product mix to more premium products. It has also been selling more directly to customers than through wholesalers. Around 64% of its sales were through wholesale in the first quarter, down from 74% three years earlier. E-commerce sales have risen from 13% to 17% of sales.

Asics trades at 34 times forward earnings, according to S&P Global Market Intelligence. That is a similar multiple as Deckers Outdoor but higher than bigger peer Nike, which trades at 25 times. The premium could be justified if Asics could keep growing its sales with better margins.

Asics is sprinting ahead. It still has room to run.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.