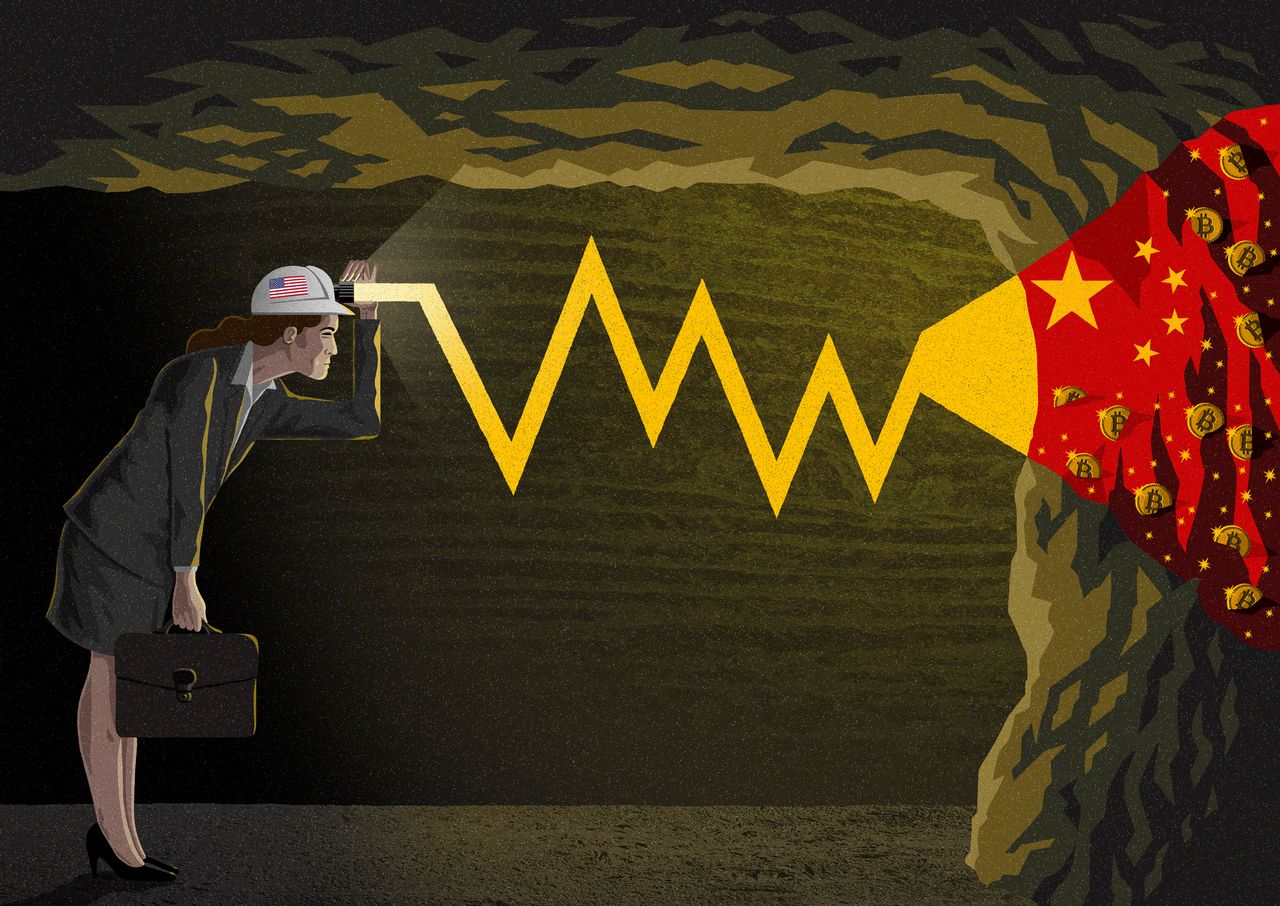

Bitcoin Mining Is Big in China. Why Investors Should Worry.

Why the digital currency’s dependence on China, specifically Xinjiang, is concerning.

By Isaac Stone Fish

Wed, Feb 24, 2021 1:27am 3 min

3 min

3 min

Why the digital currency’s dependence on China, specifically Xinjiang, is concerning.

3 min

Critics of the nearly ubiquitous digital currency Bitcoin often focus on its environmental consequences. After Tesla announced recently that it had bought roughly US$1.5 billion in Bitcoin, sending the cryptocurrency’s value skyrocketing, sustainability investors decried the “level of carbon dioxide emissions generated from Bitcoin mining.” Certainly, “mining”—the energy-intensive process by which computers solve complex algorithmic problems to verify blockchain transactions, for which they’re rewarded in digital currency—is an undeniable environmental offender.

But there is another worrying aspect of Bitcoin, one that should make investors think twice about including it as part of an ethical investing strategy.

A large amount of new Bitcoin comes from Xinjiang, the region in northwest China where more than a million Uighur Muslims and other minorities have been imprisoned in concentration camps. According to the Cambridge Bitcoin Electricity Consumption Index, as of April 2020, China was responsible for 65% of all Bitcoin mining. And of that, 36% takes place in Xinjiang, the largest regional component. Why? Cheap coal means cheap energy to power the machines that mine Bitcoin. Xinjiang has an abundant supply of coal, and the region’s relative remoteness means that it’s far cheaper to use the resource locally than move it to other parts of China. The issue is not that the Chinese government uses forced labour in Xinjiang coal mines—the reporting on that is inconclusive. Rather, because of the atrocities occurring in Xinjiang, any product produced there brings with it high ethical and regulatory risk.

In the camps—which Beijing calls “vocational educational and training centres”—guards try to “deradicalise” Uighurs for crimes such as wearing long dresses, abstaining from pork or alcohol, or praying. While the difficulty of reporting in the region means that concrete evidence is scarce, camp survivors have described systemic torture, forced sterilization, and rape. (Beijing denies committing atrocities.) In January, right before leaving office, Secretary of State Mike Pompeo declared that Beijing was committing “genocide” in the region. His successor, Antony Blinken, agrees.

To summarize: Roughly 20% of new Bitcoin is mined in Xinjiang, the site of some of the world’s most egregious human-rights abuses.

Today, Bitcoin’s association with Xinjiang is barely discussed. But that may change. For public-facing funds considering investing in the notoriously volatile asset, there are two other risks to consider. The first is that because of the concern among the American public about human-rights abuses in Xinjiang, holding assets tied to the region comes at the risk of a public relations disaster.

Already, activists have criticised Olympic sponsors for participating in the “genocide Olympics”—the 2022 Beijing Winter Games. Multiyear campaigns to hive Xinjiang off from the global supply chain are already well under way.

In July, more than 190 organizations, including the AFL-CIO, called for clothing brands to end all sourcing from Xinjiang within the next 12 months. (In 2020, roughly 20% of the world’s cotton came from Xinjiang.) It’s not hard to imagine Bitcoin becoming another frontier in their campaigns.

Investors should be alert for regulatory action. Bitcoin’s Xinjiang relationship gives ammunition to those in the U.S. government who may want to further monitor or restrict the transactions. Analysts expect the Biden administration to pay close attention to Bitcoin. In mid-February, Treasury Secretary Janet Yellen criticised the “misuse” of cryptocurrencies in laundering money or funding terrorism. At the same time, Bitcoin’s Xinjiang connection could put it on the radar of the various arms of the Commerce, State, and Defense departments that are seeking to reduce U.S. dependence on physical and digital Chinese goods. If this trend intensifies, the Treasury Department could sanction the Bitcoin mining firms that have large operations in Xinjiang, or issue advisories that it is “studying” Bitcoin’s links to the region—signalling to global financial institutions another risk of holding the cryptocurrency.

In January, U.S. Customs banned the imports of Xinjiang cotton and tomato products and told U.S. companies to get forced labour out of their supply chains. Extricating Bitcoin from Xinjiang could be far more difficult. Unlike, say, blood diamonds or Iranian crude oil, Bitcoins exist only digitally. While there is a public record of the billions of Bitcoin transactions, it’s exceedingly complicated to determine the geographic origin of a particular Bitcoin. That means all Bitcoin holders can deny any connection to human-rights abuses—but also risk being tarnished by the association.

It has long been ironic that Bitcoin, developed to decentralize power, is so dependent on China, a country ruled by a government obsessed with centralizing it. But depending on China is one thing. Depending on Xinjiang is another. There are many excellent ethical and regulatory reasons not to buy Bitcoin. Add Xinjiang to that list.

Isaac Stone Fish is the CEO and founder of Strategy Risks, a firm that quantifies corporate exposure to China.>

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.