Venture capitalists’ appetite for energy and artificial-intelligence investments is putting Europe’s venture sector on a hot streak.

European governments’ focus on energy security amid heightened geopolitical tensions has helped spur a capital rush, investors and analysts say. That coupled with the emergence of Europe-based AI startups, which can be less expensive than their U.S. counterparts, is also drawing investors.

European startups raised $15.5 billion in the second quarter, up 14% from the first quarter and up 12% from the same quarter of last year, according to Europe-based analytics firm Dealroom.co. Meanwhile, the amount invested into North American startups rose 9.6% in the second quarter from the prior quarter while Asia deal value rose 6.4% over the same period.

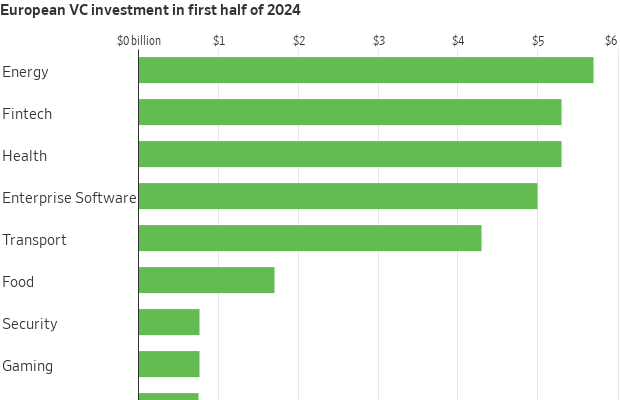

Energy was the most funded sector in Europe in the first half of the year, netting $5.7 billion, while funding raised by AI startups accounted for a record 18% of venture funding in Europe, up from about 11% in 2021, Dealroom.co said. Before last year, energy startups typically raised less capital than fintech, health and enterprise software startups.

Russia’s invasion of Ukraine spurred European governments—which were historically dependent on Russian fossil fuels—to develop greater energy security. Support has reached startups in the form of grants and other government-backed investment opportunities.

“It has been a major shift,” said Orla Browne , head of insights at Dealroom.co. “The exposure of energy-security issues with the invasion of Ukraine has filtered down to startups.”

Large AI deals have also drawn capital to Europe. In May, Wayve, a U.K.-based developer of autonomous driving software, raised $1 billion from investors including SoftBank Group , chip maker Nvidia and Microsoft . In June, French startup Mistral AI raised $646 million from investors including the venture arm of software giant Salesforce , General Catalyst and Lightspeed Venture Partners.

In Europe, investors say they can scoop up shares of startups for less money compared with the prices that their counterparts in the U.S. command. Meanwhile, Europe’s technical universities are supplying promising entrepreneurs, particularly in the AI field.

“We have hired a world-class team at salaries that cost 30% or less than you would get for a similar team in [Silicon Valley] with the caliber being as good,” said Dominic Vergine , chief executive of Monumo in Cambridge, England, which uses AI to make electric motors more efficient.

Europe’s climate regulations have also helped attract funding for energy startups, for example the European Commission’s Innovation Fund.

Danijel Višević, co-founder of Berlin-based World Fund, said funding from countries like Germany and France as well as from the European Union helped push more capital into climate startups. “Europe has started to reap the rewards of the fruits it sowed with climate tech R&D,” said Višević.

He added that given the long-term effects of climate change, funding in the sector is likely to be stable, both from venture-capital firms and governments, for years to come.

Even so, Europe’s venture sector faces some headwinds. In the second quarter, the continent saw $2.2 billion in exits, a third fewer than in the same quarter a year ago and 93% under the second quarter of 2021, a banner year for exits worldwide, according to a report by professional-services firm KPMG. Exits include initial public offerings and mergers and acquisitions and are the primary way venture investors cash out of their startup investments.

High interest rates, which typically encourage investors to divert capital away from venture to fixed-income strategies, have also hurt the industry. European startups’ second-quarter haul is far below the record $34.6 billion they netted during the same quarter of 2021.

Investors are eager for a turnaround. Last year, Planet First Partners, which has offices in London and Luxembourg, raised a €450 million fund, equivalent to $485 million, in part on the thesis that Europe’s favorable climate regulations are a financial tailwind for energy startups.

In March, the firm invested in Sunfire, a German startup developing hydrogen energy technology aimed at reducing reliance on fossil-based energy from oil, gas and coal. The investment came as part of a €215 million Series E equity funding round and included an additional term loan of up to €100 million from the European Investment Bank.

Sergio Carvalho , a partner and head of sustainability at Planet First Partners, said the firm has invested in Sunfire in part for its potential to help Europe become more energy independent. PFP’s first investment in Sunfire was before the invasion of Ukraine. “Europe has been pushing decarbonization systematically,” Carvalho said.

Last year, Sunfire received €169 million from a European Union initiative that funds projects that address EU-wide challenges.

In July, Index Ventures, which was founded in Europe and has offices in London, San Francisco and New York, raised $2.3 billion in new funds—an $800 million venture fund and a $1.5 billion growth fund. Hannah Seal , an Index partner in London who focuses on enterprise AI deals, among other sectors, said she expects roughly half of the venture fund to be used to invest in startups that are based in Europe.

“The first half of this year was one of the busiest we’ve ever had,” Seal said about AI dealmaking in Europe. “We’re seeing a general stabilisation in the global economy which is obviously impacting sentiment.”

4 min

4 min

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.