Plymouth County is known for Pilgrims, cranberries—and a top-performing pension fund run by a 65-year-old former schoolteacher.

After a decade of mostly ho-hum performance, the $1.4 billion Plymouth County Retirement Association ranked in the top 10% of U.S. pensions over the past three years. Key to that success was an early—and prescient—bet that interest rates would rise. That buoyed the fund through big chunks of the past two years, when climbing rates hammered both stocks and bonds.

Now markets of all kinds have posted a six-month rally , stocks are hitting records and Plymouth risks falling behind again. But Peter Manning, the fund’s director of investments, is sticking to his guns. The hope that rates will fall soon is misplaced, he said. Another downturn could be coming for Wall Street.

And so, to Manning, the best way to enlarge the pension long term is by avoiding big losses, rather than chasing high returns.

“It ain’t about what you make. It’s about what you keep,” he said.

Beating the big guys

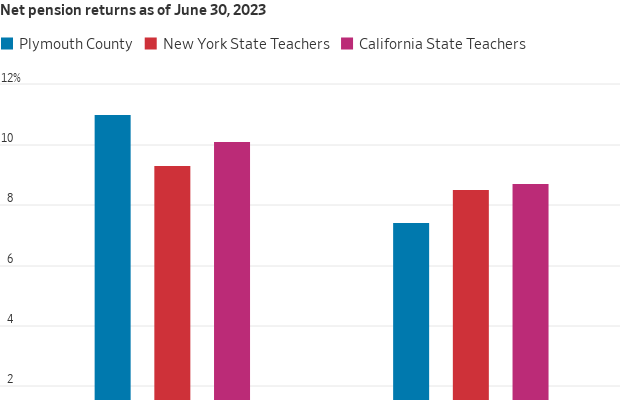

The fund, which manages savings for the county’s firefighters, bus drivers and custodians, delivered average annual net returns of 5.7% in the three years ending Dec. 31. That put it ahead of 92% of pensions nationally. The median U.S. public retirement fund returned 3.7% over the same period, according to Investment Metrics, a portfolio analysis provider.

Plymouth County surpassed bigger peers by slashing exposure to Treasurys and public stocks before they tanked in 2022. The fund then reinvested the money in infrastructure, private equity and inflation-protected debt.

While many other public plans have followed suit , the trades were also unusually quick for pension funds, which often change investments incrementally rather than in bold strokes.

“A lot of our clients made moves on the margin,” said Daniel Dynan, a managing principal at Meketa Investment Group, Plymouth County’s investment consultant. “The difference in Plymouth is the magnitude of the change.”

An unlikely trendsetter

With only 10,500 members, the fund is an unlikely trendsetter. U.S. public pensions guarantee retirement and benefit payments to 34 million members nationally, according to data from the Urban Institute, a nonprofit think tank. Plymouth County, which lies south of Boston, encompasses mostly middle-class suburbs, but also some wealthy enclaves and gritty urban areas. It is split between Democratic and Republican voters.

A decade ago, Plymouth County had only about half of the money it needed to make expected payments for its retirees. An accounting change in 2012 drastically widened shortfalls for most public pensions across the country.

At the same time, the board overseeing the fund, which had spent years relying solely on an outside consultant, was dissatisfied with its investment performance. The approach resembled the classic mix of 60% stocks and 40% bonds popular with ordinary investors.

“We were doing what everyone else was doing, running a 60-40 portfolio and hoping for the best,” said Tom O’Brien, Plymouth County’s treasurer and chairman of the pension board.

From teacher to investor

The county hired Manning to advise the board on investment strategy in 2012. He had never managed a pension fund before.

“I was a schoolteacher [in the 1980s] in a suburb of Boston and one day, after staring at 20 vacuous stares, I had a talk with my Uncle Bill, a currency trader,” Manning said.

He spent two decades trading commodity futures at his uncle’s brokerage in Boston and stocks at brokerages in Chicago. Then he became a financial adviser to wealthy individuals and families at Merrill Lynch on Cape Cod.

The job at Plymouth County involved a small pay cut, but offered the opportunity to run a nine-figure portfolio for public employees. He got a taste of how painful rising rates could be in May 2013, when comments by Fed Chairman Ben Bernanke sent bond prices tumbling in what became known as the “taper tantrum.”

“We lost $20 million in three trading days and it took us 36 months of clipping coupons to make that back,” Manning said. Coupons are the interest payments bondholders receive.

Initially, Manning and O’Brien focused on boosting alternative investments such as private equity and infrastructure, which made up less than 5% of the fund. They were part of a flock of pension funds seeking alternative investments for higher returns .

Plymouth County hired Meketa as a consultant in 2015, and private-equity and infrastructure investments climbed to nearly 15% by 2020, according to fund financial reports. Returns improved.

“They have a level of comfort being different,” said Dynan.

A contrarian call

Markets were on a tear the following year, lifted by the economy’s reopening from the pandemic. But Manning grew concerned in the summer about inflation. While many on Wall Street were calling price increases transitory, he worried inflation would persist, triggering rate increases and declines in stocks and bonds.

“We were going to conferences and being told that inflation was a paper tiger, or ‘this is not your father’s inflation,’” O’Brien said.

Manning consulted Bob Sydow, a high-yield bond fund manager at Mesirow who manages part of the pension’s money. Like Manning, he has worked on Wall Street since the 1980s.

“The money supply grew 43% over 26 months during Covid,” Sydow said. “I called it ‘free-range’ money and I thought it would generate a lot of inflation.”

From October 2021 to February 2022, Plymouth County pension sold about $80 million of its public stocks, or 6% of the fund’s assets, according to an email viewed by The Wall Street Journal. It shifted into real estate and infrastructure as well as short-term and floating-rate debt that is less sensitive to rising rates than traditional bonds, Manning said.

The fund lost 6.5% in 2022 while the median U.S. pension plan lost 14%. That outperformance has helped it stay ahead of other funds, even after it lagged behind the average in 2023.

Now, inflation remains above the Fed’s targets , and analysts’ forecasts for multiple rate cuts this year seem less certain. Plymouth County is keeping its strategy relatively unchanged, betting that rates will remain steady—or even climb.

Many investors are buying back into bonds because yields are at multiyear highs and they expect cuts by the Fed to trigger a rally. Manning takes a different tack. He thinks rates could stay high far longer than the Wall Street consensus, so he is using infrastructure funds to deliver income rather than bonds.

“Why do you have to own bonds at all in 2024?” Manning said. “It’s a legitimate question.”

5 min

5 min