I Cancelled My Unused Subscriptions. The Money I Saved Paid for a Tesla.

A close look turned up a car’s worth of savings I didn’t know existed

By CHRIS KORNELIS

Mon, Mar 4, 2024 9:02am 5 min

5 min

5 min

A close look turned up a car’s worth of savings I didn’t know existed

5 min

My new Tesla was burning a $511 hole in my monthly budget. So I set myself a challenge: Could I cover the cost just by getting rid of cable, Netflix and other subscriptions I didn’t need?

The financially responsible among us might cancel streaming services between seasons of their favorite shows . I tend to add new ones and forget about the old ones, doing my share to support America’s ballooning subscription economy. People pay about $273 a month for subscriptions, which is almost $200 more than they think they do, according to a 2021 survey . (Since then, services like Disney+ and Discovery+ have raised their prices further.)

But I needed to make room for the first car payment in my 41 years. I had taken the family car-shopping when our 2001 Toyota Camry, which we inherited from my wife’s grandmother, started to go. I’m not a car guy and had never once wished I’d owned a Tesla. I booked a demo drive for the Model Y because I thought our kids would get a kick out of it.

The fact that we liked the car was almost as surprising as the fact that it was cheaper than the electric Volvo, Volkswagen and Hyundai options we saw. It felt like a spaceship compared with the Camry, which has 205,000 miles, a broken tape deck and an interior stained with blue and yellow crayon.

Our new monthly payment covered a 12,000-miles-a-year lease with no down payment. Tesla estimated I would save about $100 a month from replacing gas with electric, though I would need to drive (and charge) the car to know for sure. Tesla’s app tracks my estimated savings. For now, that left us with $411 to cut from our other monthly expenses.

My wife was on board. My kids shrugged. I got out my notebook and started making a list.

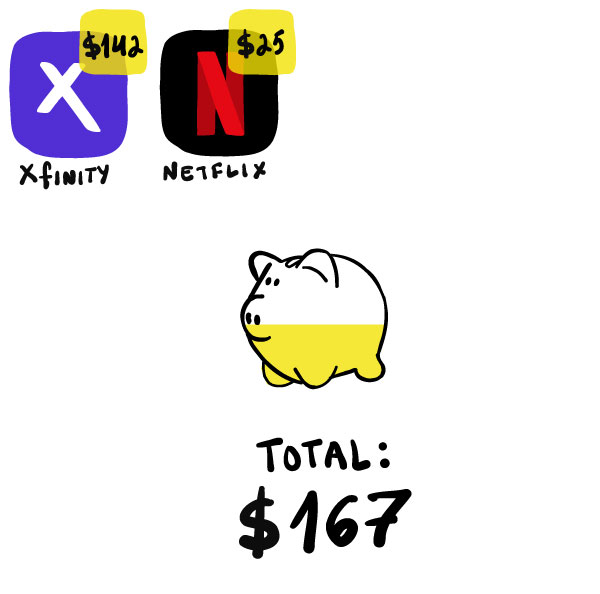

My first stop was my Xfinity bill.

Somehow, it had swelled to $249 a month—basically half the price of the car. In addition to cable and internet, I’d been paying Xfinity for things like a landline because cell service can be spotty in my basement office. So long, landline. After cutting everything but internet, my bill fell to $107. I haven’t dropped a call yet.

Next were the streaming services that I’d been paying for but not watching much. Over the past few years, the only person in the house “watching” Netflix was me. And I wasn’t actually watching it. I was listening to episodes of “Seinfeld” in an earbud when I went to bed. The jokes and the rhythm of their back-and-forths were a pleasant send-off as I fell asleep.

I had joined the growing number of Americans ditching streaming services. I also broke up with BritBox, a streaming service that I’d counted on to watch Agatha Christie’s “Poirot,” as well as Apple TV+. I said goodbye to Hallmark Movies Now, which I’m not ashamed to admit I enjoyed every now and then.

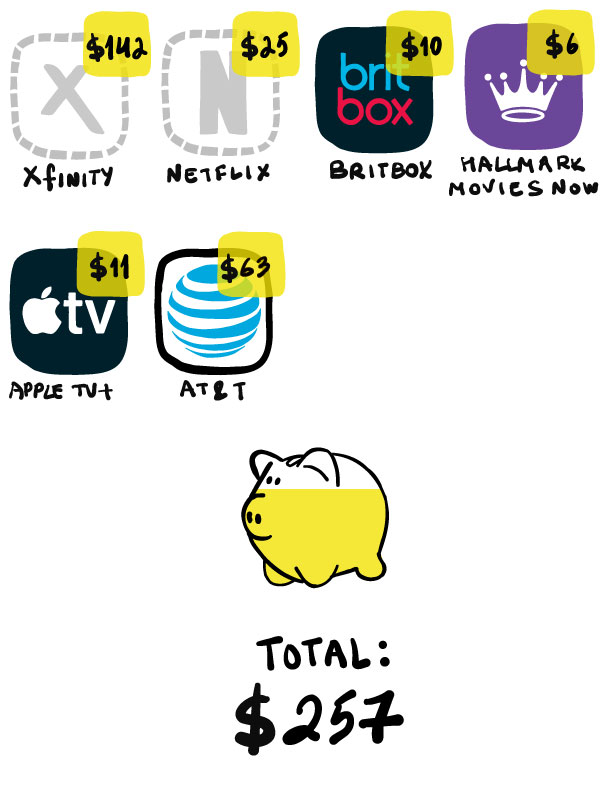

Next up was AT&T .

Paying for cellphone service is like paying the water bill: something I did without protest and never really thought twice about. But I’d started to get curious about the ads I’d been seeing for low-cost services like Boost Mobile and Cricket Wireless. When we agreed to let our 13-year-old son have a phone, part of the deal was that he had to pay for and maintain the account himself. He got a plan with Mint Mobile. It has worked so well for him that we decided to give it a try.

We had been paying AT&T about $128 a month for two lines. Now, we’re paying Mint about $65. If there is a downside to making this move, I have yet to notice it.

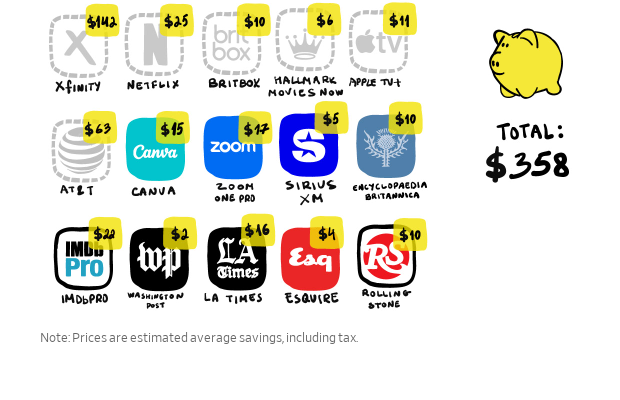

Then my wife and I sat at our dining table going through the last couple months of transactions in our checking account. Seeing how much money we were wasting was painful. We were both paying for subscriptions to Canva, a graphic-design service.

We’ve also been paying for Zoom One Pro, which I probably haven’t used in more than a year. I attempted canceling SiriusXM, but they kept me around by dropping the cost by about $5 a month, which is nice because I have become obsessed with a channel dedicated to country artist and sometimes actor Dwight Yoakam.

Upon further consideration I axed subscriptions to IMDbPro and Encyclopaedia Britannica, which I’m sure I’ve used professionally, but…not for a while. Finally, I cut or got reduced rates on four of my digital subscriptions to news publications. I had been making monthly payments to them more often than I was reading them.

In the end, I was able to cut out about $358 in unnecessary bills and subscriptions. Added to the $100 in estimated gas savings, the cost dropped to $53 for a car we desperately needed.

And since the lease came with six months of free access at Tesla Superchargers, the Tesla app tells me I saved $164 by not pumping gas in January, exceeding the $100 I had estimated. In January at least, my car was free-ish.

“So I love and I hate what you did,” David Bach told me. The author of personal finance books like “Smart Couples Finish Rich” has long preached the merits of cutting out small, fixed expenses. But he’d rather have seen me invest the savings.

“If you’re already a millionaire, go enjoy the Tesla,” he said.

It isn’t like we’ve had to revert to our DVD collection to entertain ourselves. We still have Disney+, Hulu, Max, the language-learning service Duolingo and, of course , Spotify. We get three print newspapers delivered and many more digital news subscriptions.

I’m reacquainting myself with some shows on the services I kept, like Billy Bob Thornton’s “Goliath” on Prime Video—featuring an exceptional performance from Dwight Yoakam.

It is possible we’ll start subscribing all over again. Americans resubscribe to about 23% of the larger streaming services they cut within three months. That share rises to over 40% after a year, according to Antenna, a subscription-analytics provider.

I get it. I subscribed to Paramount+ for Super Bowl Sunday (yes, I canceled it the following Tuesday). And I’m tempted to return to Netflix every time I get ready for bed. I still haven’t found a lullaby to replace “Seinfeld,” but at least I am the master of my (financial) domain.

I need something upbeat but not preachy, familiar, but with enough episodes that I don’t get too sick of them. I tried “Bob’s Burgers,” but Louise Belcher’s screams and the high-pitched strumming of the ukulele between scenes kept me awake.

Oh well. Reliable transportation is worth the $511 monthly payment. Come to think of it, that feels a lot like a subscription.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.