Is This 1987 All Over Again? What’s Driving the Market Meltdown?

Past routs offer lessons after Black Monday Morning

By JAMES MACKINTOSH

Wed, Aug 7, 2024 9:17am 4 min

4 min

4 min

Past routs offer lessons after Black Monday Morning

4 min")

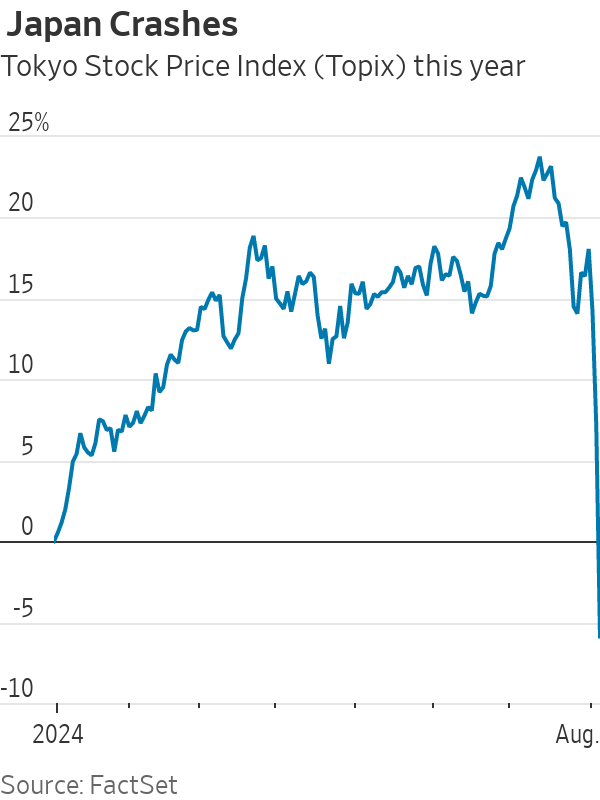

Financial markets are supposed to capture the wisdom of the crowd, but on Monday the crowd ran in all directions waving its hands in the air screaming. Japan’s stock market fell the most in 37 years with a 12% plunge that wiped out all its gains for the year, while in the U.S. the VIX index of implied stock volatility briefly had its biggest rise ever. Panic hit.

The selloff was triggered by Friday’s jobs data prompting a sudden switch in the economic narrative from soft landing to hard landing. Add to the mix a period of deflating hype about artificial intelligence and a Bank of Japan rate rise designed to strengthen the yen. News that Warren Buffett’s Berkshire Hathaway had sold half its Apple shares and boosted its cash pile added to the pain.

But the triggers couldn’t possibly justify the scale of the moves. When a new trigger arrived, in the form of better-than-expected data on the service sector, markets partially rebounded and the Vix fell sharply — again, far more than the data could justify.

The selloff—which at one point had chip maker Nvidia down 15%—was so big because investors had been all-in betting that things would work out well. Now things have calmed a bit, the question is whether the unwind of these bets, and the leverage behind them, is done. If it resumes, will the selloff feed back into higher savings and a weaker economy or, worse, hit the financial system?

The extreme examples of past effects from big market falls are 1987’s crash, 1998’s Long-Term Capital Management blowup and 2008’s global financial crisis. History is never perfect, but so far this looks more like a (much milder) version of 1987 than it does the other two.

In 1987, the stock market had its biggest one-day fall ever, with the S&P 500 down more than 20% on Black Monday in October. Investors had built up excessive leverage after a stunning 39% gain in the year to August’s high, and the crash led both to big margin calls and to badly designed automated trading that exacerbated the selling. But the Federal Reserve poured liquidity into the banks, brokers didn’t default and the market made back all its losses within two years. The economy was fine.

The good news was that 1987 was all about markets: They went up, they went back down, no one else was hurt. The S&P made 36% in the eight months to its August 1987 peak, similar to the 33% it rose in the eight months to the end of June this year. As in 1987, this year’s gains came in spite of tight monetary policy and higher bond yields. Just like today, in 1987 investors were on edge and ready to sell to lock in the unexpected profit. The losses are smaller so far, but lucrative trades have reversed , just as they did for the market as a whole in 1987.

In 1998, the situation was much worse, although stocks recovered more quickly. Highly levered hedge fund LTCM was crushed when Russia’s domestic debt default created a flight to safety. LTCM was big enough that it threatened to bring down Wall Street institutions. The Fed cut rates three times and pulled together a group of banks to rescue the firm and wind down its trades slowly. Stocks took just four months to recover, but the easy money helped stoke the dotcom bubble, which popped two years later and led to a mild recession—and gigantic losses for investors in tech stocks.

We don’t know yet if any hedge funds have been taken out by the big moves in markets, which have brought heavy losses for those engaged in the “ carry trade ” of borrowing cheaply in yen and buying higher-yielding currencies such as the Mexican peso or dollar. Large swings in Treasurys on Monday might also have hurt, given the large positions hedge funds hold. Traders are betting that the Fed will slash rates, with a super-sized cut of 0.5 percentage points priced into futures for the September meeting (and far more earlier in the day).

The really bad outcome would be a repeat of 2008, but it seems highly unlikely. True, some large U.S. banks failed last year, due to bad bets on government bonds. But banks are much less leveraged than they were, and the system is less exposed to a liquidity crisis, as private lenders have taken on much of the risk that used to sit in banks. Big losses are entirely possible, and private funds could hit trouble, but that would take time and wouldn’t create the same system-wide crisis.

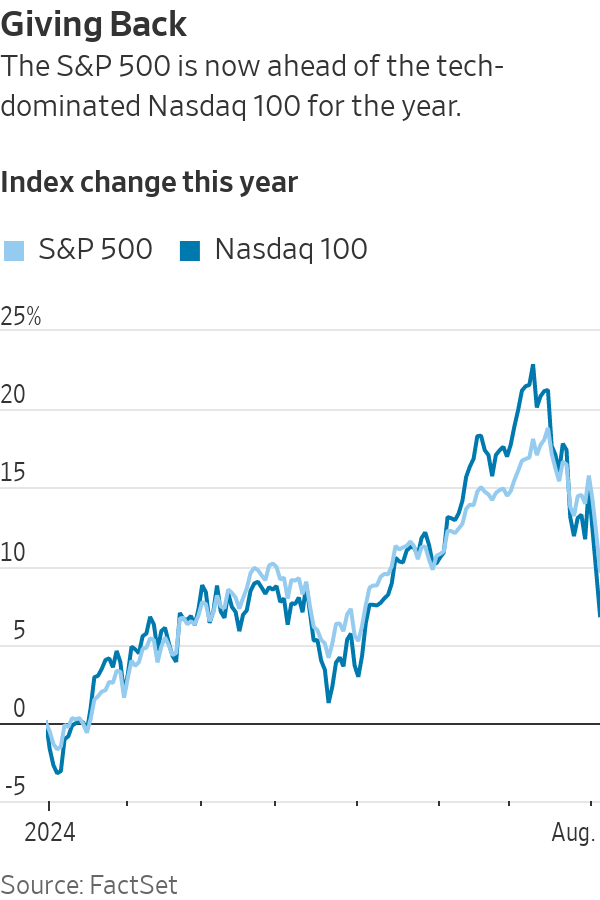

The ideal would be that excess in the stock market unwinds as in 1987 without creating wider trouble, hopefully more gradually than in 1987. AI enthusiasm could deflate stock prices much more—even after falling 30% from its June high, Nvidia has still doubled in price this year. But the market is already much closer to normal, with Monday’s falls leaving the Nasdaq 100 index up only 6% this year, and the S&P 7%.

If panic continues to abate, the Fed cuts and nothing breaks in the financial system, we should count ourselves lucky. But it would be good if investors could remember the sinking feeling they had on Monday morning, and try to be a bit wiser and less speculative.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.