More Americans Than Ever Own Stocks

Pandemic, zero-commission trading ‘created a whole generation of investors’

By HANNAH MIAO

Tue, Dec 19, 2023 9:25am 4 min

4 min

4 min

Pandemic, zero-commission trading ‘created a whole generation of investors’

4 min

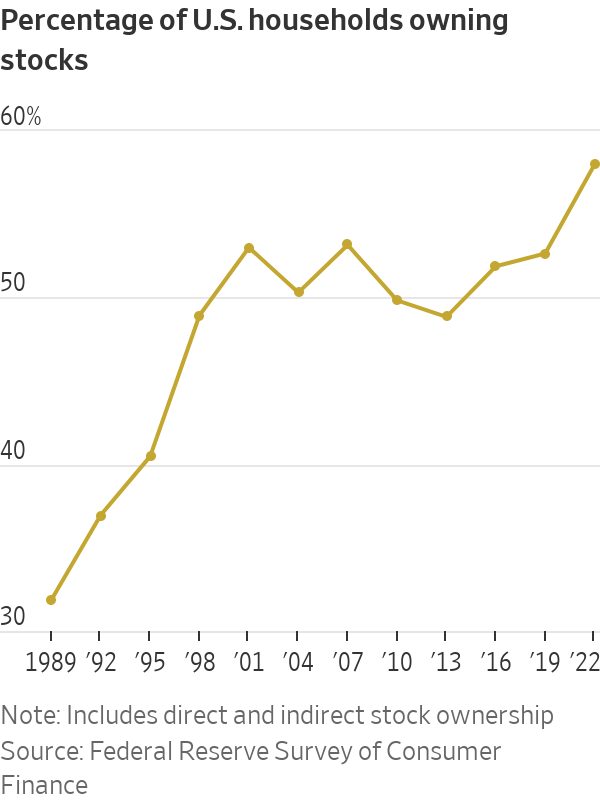

The share of Americans who own stocks has never been so high.

About 58% of U.S. households owned stocks in 2022, according to the Federal Reserve’s survey of consumer finances released this fall. That is up from 53% in 2019 and marks the highest household stock-ownership rate recorded in the triennial survey. The cohort includes families holding individual shares directly and those owning stocks indirectly through funds, retirement accounts or other managed accounts.

The data provide the most comprehensive snapshot yet of how the Covid-era explosion in investing has reshaped Americans’ personal finances. Stuck at home during the pandemic with extra cash, millions jumped into the stock market for the first time. The elimination of commission fees on stock trading across U.S. brokerages made investing cheaper than ever.

“It created a whole generation of investors,” said Anthony Denier, chief executive of mobile brokerage Webull U.S.

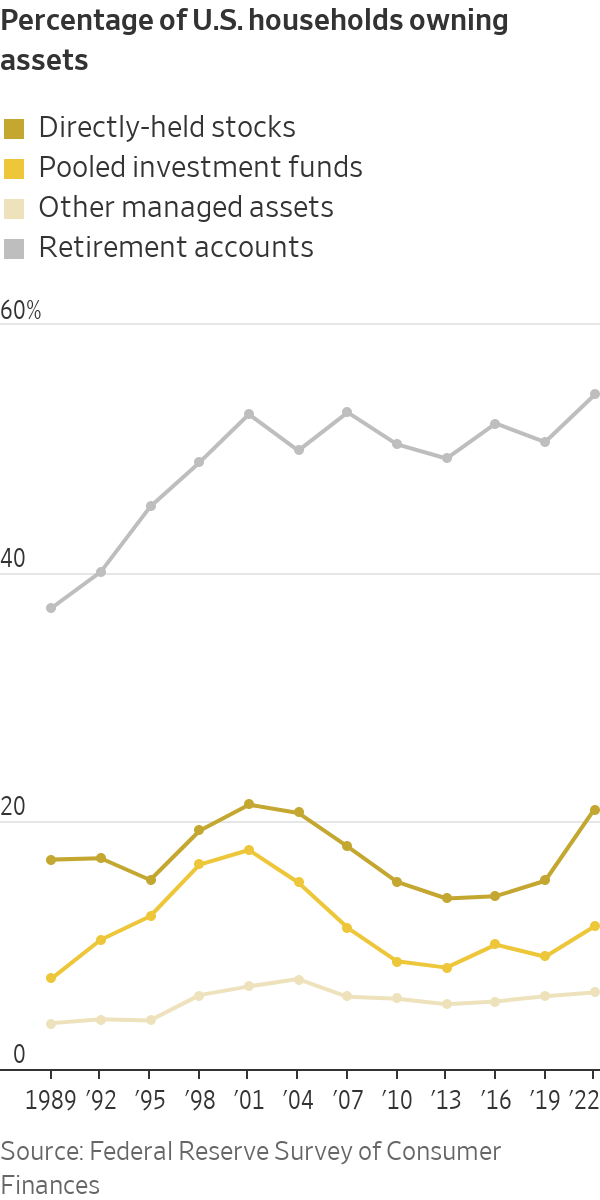

Most households own stocks through a retirement account, such as a 401(k), but more Americans in the past few years have invested in individual shares directly. Direct stock ownership increased to 21% of families in 2022 from 15% in 2019—the largest increase on record since the survey began in 1989.

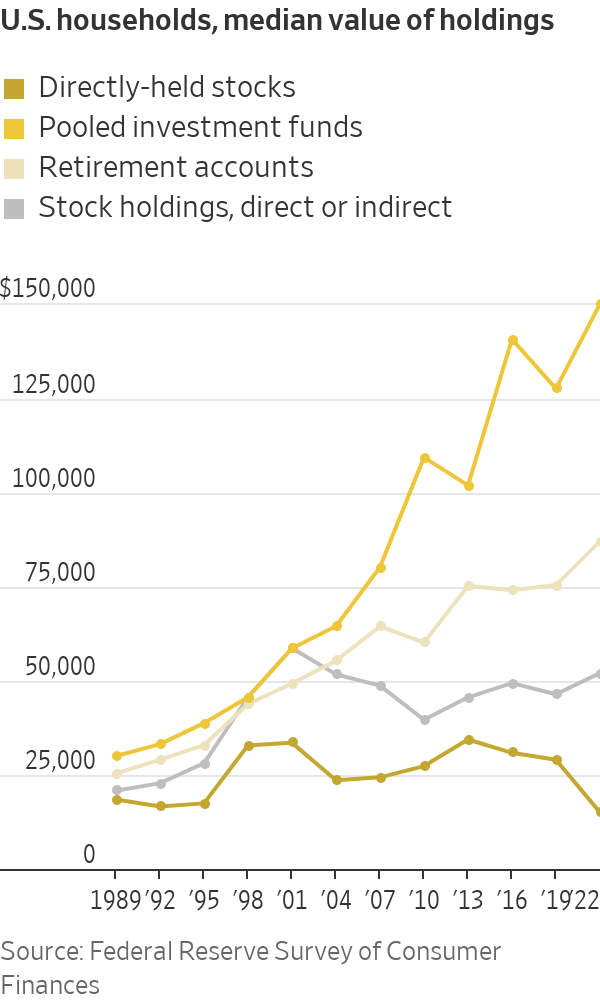

As more households bought individual shares, those newer entrants invested with less money than longtime stockholders. The median value of households’ direct stockholdings nearly halved from 2019 to about $15,000 in 2022, adjusted for inflation.

When the stock market crashed in early 2020, Nick Luczak, then a sophomore at the University of Michigan, used the $57 in his checking account to open a brokerage account on Robinhood and buy whichever stocks he could afford. Once the pandemic forced him off campus to live with his parents, he began researching the market and buying more stocks.

“I said, ‘Well, I have all this spare time. There’s no reason at all I shouldn’t be trying to make the most money possible from this,’” Luczak said.

Luczak and his fraternity brothers started a group chat to discuss markets and stock picks. He said he made a profit investing in Amazon.com and watched his friends make, then lose, thousands of dollars trading meme stocks such as GameStop and AMC Entertainment Holdings in 2021. At one point, he considered becoming a day trader.

Now, Luczak, 24 years old, is focused on long-term investing. A salesman in Dallas, he is studying to become a certified financial planner.

Brokerages in recent years have made trading free and easy. Newer apps like Robinhood and Webull helped popularise zero-commission stock trading on smartphones. Charles Schwab, TD Ameritrade and E*Trade all eliminated commission fees for stocks at the end of 2019. Fidelity and Schwab introduced fractional stock trading in 2020, allowing individuals to buy and sell slivers of shares.

“It’s become more accessible,” said Ashley Feinstein Gerstley, a certified financial planner and founder of The Fiscal Femme. “We’ve been debunking in the last few years the myth that you have to be rich or work on Wall Street to invest.”

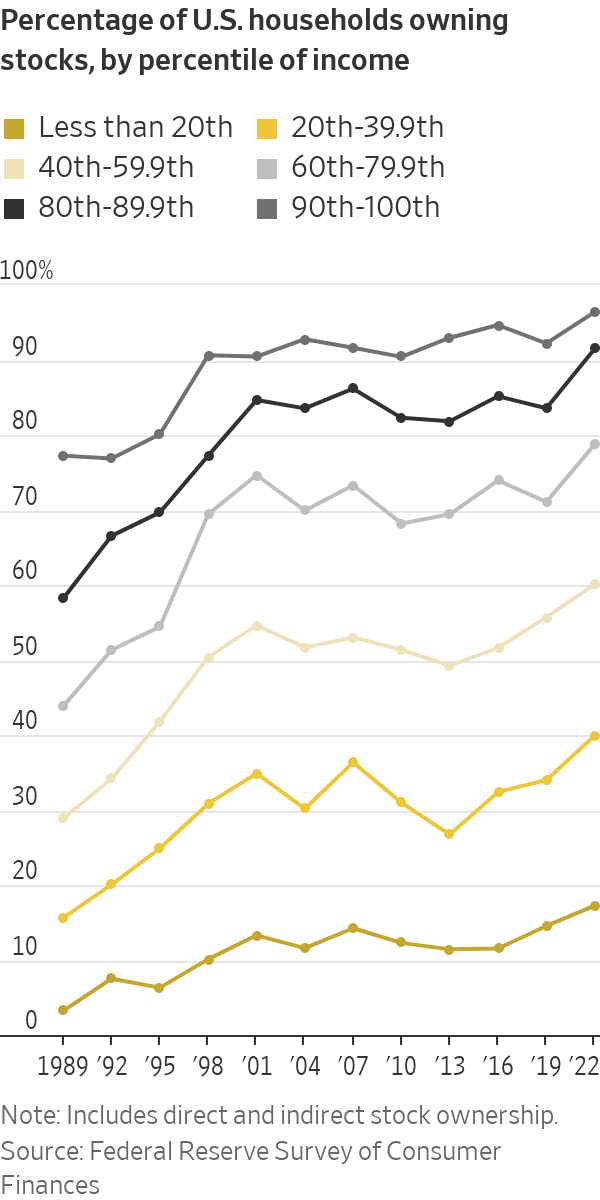

The share of households owning stocks increased across all income levels from 2019 to 2022. Upper-middle-income families recorded the biggest jump in stock ownership.

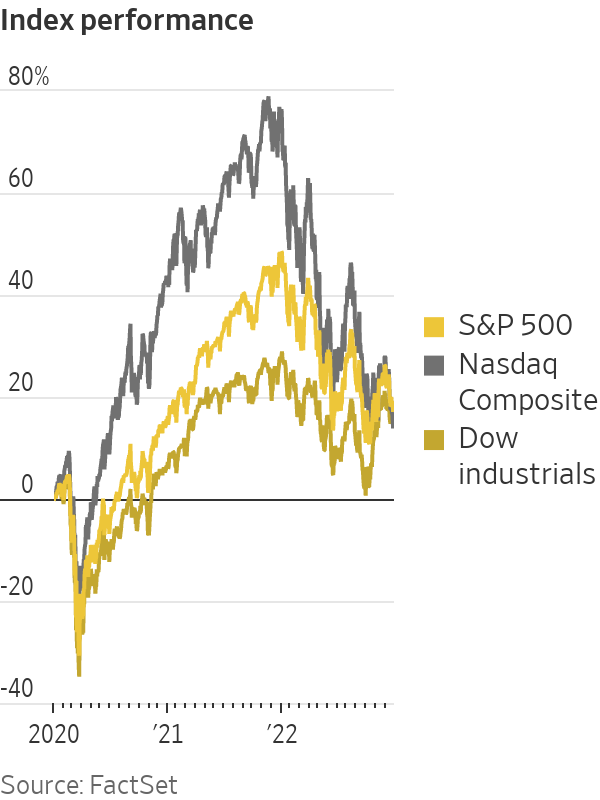

Over those three years, stocks climbed to new highs. The S&P 500 rose 16% in 2020 and 27% in 2021. Even after a 19% drop last year, the benchmark stock index notched gains over the three-year period. The S&P 500 is up 23% in 2023.

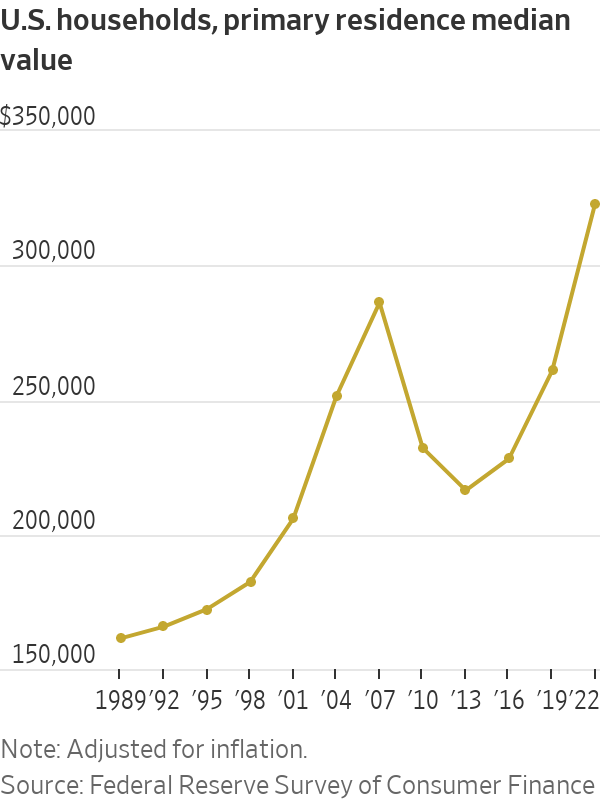

Stock-market gains and rising home prices helped boost household wealth. Households’ median net worth climbed 37% from 2019 to 2022, adjusted for inflation, the largest increase in the survey’s history. The median value of a U.S. household’s primary residence surged to $323,200 in 2022, surpassing levels from before the 2007 housing market crash.

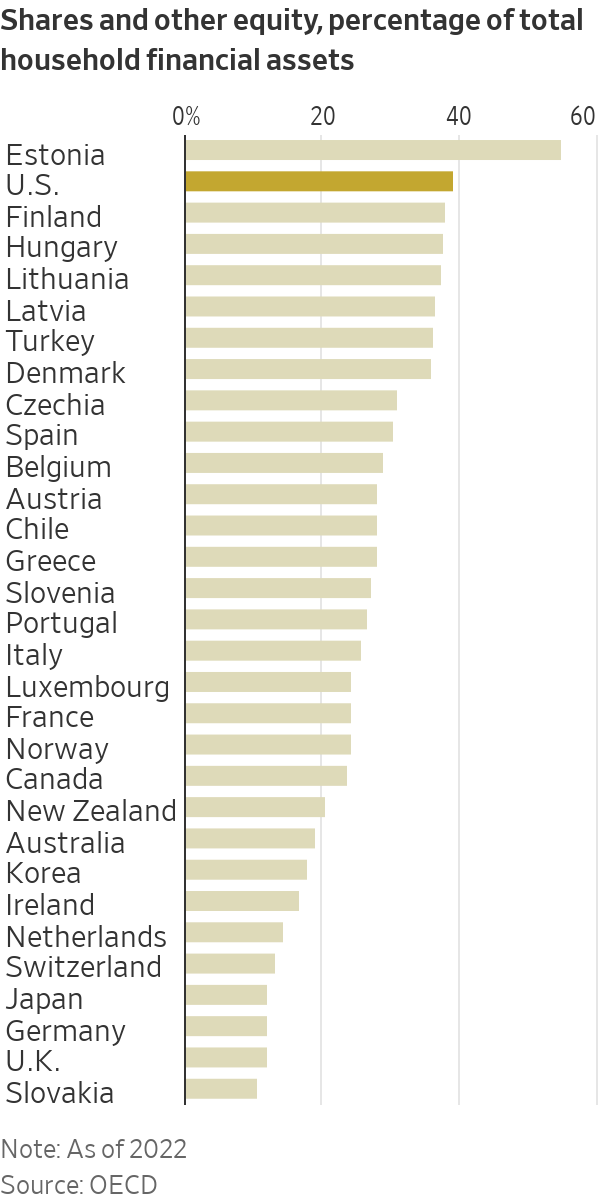

Americans’ penchant for stocks is distinct. U.S. households held about 39% of their financial assets in equities in 2022, according to Organization for Economic Cooperation and Development data, a higher allocation than most other countries in the data set.

That appetite for stocks has been tested since the Fed began raising interest rates last year at the fastest clip since the 1980s and pledged to keep rates higher for longer. Investors have been flocking to assets with little risk such as money-market funds that are now offering some of the highest yields in years. Everyday investors, who rarely own bonds directly, are taking a second look at assets such as Treasurys and corporate bonds.

Fernando Soto, head of private banking in Chicago at Brown Brothers Harriman, said he has fielded more questions from clients about fixed-income investing and more requests from clients to buy bonds in 2023. In his personal portfolio, he increased his allocation to fixed-income this year.

“There’s a big shift,” Soto said. “This is the new normal.”

How has the higher rate environment shifted American household finances? The Fed consumer finance survey in 2025 will likely paint the fullest picture.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.