The Improbably Strong Economy

A lot had to go right for the U.S. to avoid a recession. So far, it has.

By JUSTIN LAHART

Mon, Nov 6, 2023 10:09am 3 min

3 min

3 min

A lot had to go right for the U.S. to avoid a recession. So far, it has.

3 min

The economy is still generating jobs. A year ago, a lot of economists and Federal Reserve policy makers thought that it would be shedding them by now.

On Friday, the Labor Department reported that the U.S. added a seasonally 150,000 jobs in October from the previous month, versus September’s gain of 297,000 jobs. Some of that step down was due to auto workers’ strikes, which have since been resolved but temporarily caused workers to not draw paychecks.

Average hourly earnings rose 0.2% from a month earlier, putting them 4.1% higher than a year earlier. That was the smallest year-over-year gain since June 2021, though unlike then wages are now outpacing inflation.

One takeaway is that the job market is moderating, but not buckling—a message reinforced by a variety of other data, including low levels of weekly unemployment claims and layoffs. Another is that the Federal Reserve is probably through with tightening: Futures markets on Friday morning indicated that the chance of the central bank raising its target range on overnight rates at its December meeting was below 10%. The yield on the 10-year Treasury note, which briefly hit 5% less than two weeks ago, continued to retreat Friday, falling to 4.53% midmorning.

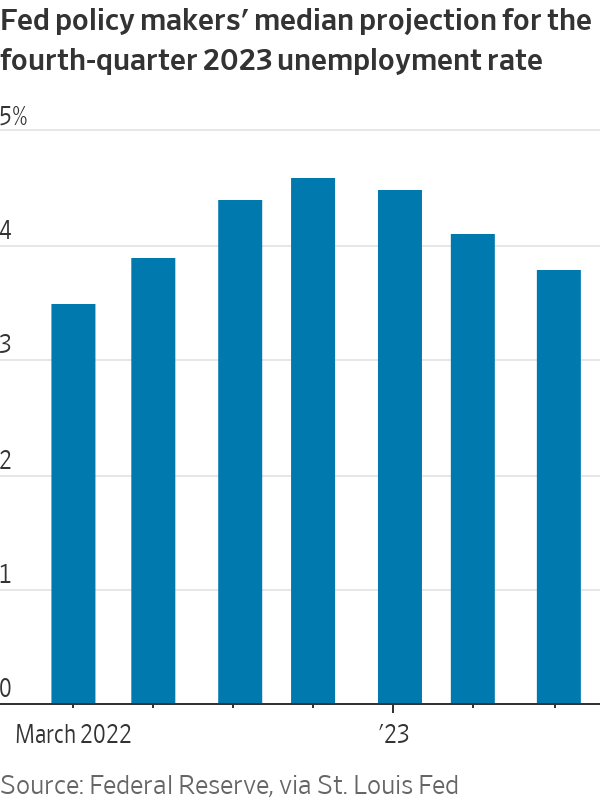

This wasn’t the sort of job market the Fed expected. When policy makers offered projections last December, they forecast that the unemployment rate would average 4.6% in this year’s fourth quarter, versus the 3.7% rate (since revised to 3.6%) they had seen in the November 2022 job report. That was tantamount to a recession forecast, though they didn’t put it that way, since such a large increase in the unemployment rate would count as a strong signal the U.S. is in a downturn. Friday’s report showed the October unemployment rate at 3.9%.

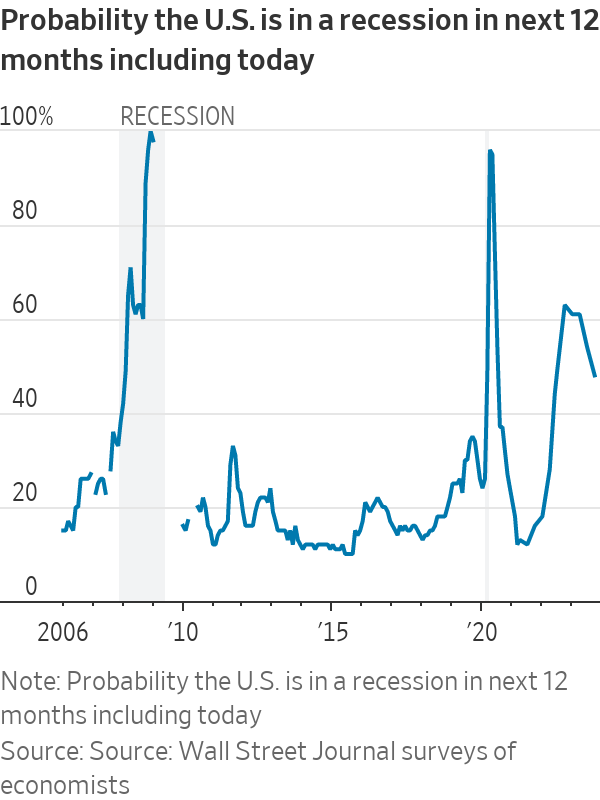

Economists got it wrong, too. In October of last year, forecasters polled by The Wall Street Journal estimated the unemployment rate at the end of 2023 to be at 4.7%, on average. They also put the chances of a recession within the next 12 months at 63%. By last month, they dropped the recession chance to 48%. Available data show that, as a group, economists have never forecast a recession before it has actually started. Now it looks as if the one time they did forecast one, they were either wrong or early.

It is easy to make fun of other people’s past forecasts, but considering the hurdles the economy has had to clear, it really is striking that it has done so well. A year ago there was some hope that the continued recovery in the service sector, and service-sector jobs, might help take up the slack as the goods sector adjusted to slowing demand. But there was also the concern that the service sector could run out of steam before the goods sector found its footing.

Another worry: That the excess savings that Americans had built up after the pandemic struck would run out, and that would cut into their ability to spend. But recent revisions to the available data suggest there was more money left in the tank than thought.

To these, add that inflation has cooled despite the addition of 2.4 million jobs so far this year, and gross domestic product is expanding much faster than economists expected. Plus, at least so far this year, the economy has made it through a regional bank crisis, a sharp increase in both short- and long-term borrowing costs, and the resumption of student-debt payments.

The jury is out on what happens next. The cooling in the job market could turn into a lurch lower, for example, as the full effect of the Fed’s past rate increases begins to take hold. Inflation, which is still too high, could accelerate, prompting the central bank to further tighten the screws.

But the chances of the economy avoiding a recession seem stronger now than they did even a few months ago. A lot of that would be down to luck, but it would nonetheless be something worth celebrating.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.