To Find Winning Stocks, Investors Often Focus on the Laggards. They Shouldn’t.

These stocks are getting hit for a reason. Instead, focus on stocks that show ‘relative strength.’ Here’s how.

By

KEN SHREVE

Wed, Jun 12, 2024 9:38am 4 min

4 min

Credit: twomeows/Getty Images

A lot of investors get stock-picking wrong before they even get started: Instead of targeting the top-performing stocks in the market, they focus on the laggards—widely known companies that look as if they are on sale after a period of stock-price weakness.

But these weak performers usually are going down for good reasons, such as for deteriorating sales and earnings, market-share losses or mutual-fund managers who are unwinding positions.

Decades of Investor’s Business Daily research shows these aren’t the stocks that tend to become stock-market leaders. The stocks that reward investors with handsome gains for months or years are more often already the strongest price performers, usually because of outstanding earnings and sales growth and increasing fund ownership.

Of course, many investors already chase performance and pour money into winning stocks. So how can a discerning investor find the winning stocks that have more room to run?

Enter “relative strength”—the notion that strength begets more strength. Relative strength measures stocks’ recent performance relative to the overall market. Investing in stocks with high relative strength means going with the winners, rather than picking stocks in hopes of a rebound. Why bet on a last-place team when you can wager on the leader?

One of the easiest ways to identify the strongest price performers is with IBD’s Relative Strength Rating. Ranked on a scale of 1-99, a stock with an RS rating of 99 has outperformed 99% of all stocks based on 12-month price performance.

How to use the metric

To capitalise on relative strength, an investor’s search should be focused on stocks with RS ratings of at least 80.

But beware: While the goal is to buy stocks that are performing better than the overall market, stocks with the highest RS ratings aren’t always the best to buy. No doubt, some stocks extend rallies for years. But others will be too far into their price run-up and ready to start a longer-term price decline.

Thus, there is a limit to chasing performance. To avoid this pitfall, investors should focus on stocks that have strong relative strength but have seen a moderate price decline and are just coming out of weeks or months of trading within a limited range. This range will vary by stock, but IBD research shows that most good trading patterns can show declines of up to one-third.

Here, a relative strength line on a chart may be helpful for confirming an RS rating’s buy signal. Offered on some stock-charting tools, including IBD’s, the line is a way to visualise relative strength by comparing a stock’s price performance relative to the movement of the S&P 500 or other benchmark.

When the line is sloping upward, it means the stock is outperforming the benchmark. When it is sloping downward, the stock is lagging behind the benchmark. One reason the RS line is helpful is that the line can rise even when a stock price is falling, meaning its value is falling at a slower pace than the benchmark.

A case study

The value of relative strength could be seen in Google parent Alphabet in January 2020, when its RS rating was 89 before it started a 10-month run when the stock rose 64%. Meta Platforms ’ RS rating was 96 before the Facebook parent hit new highs in March 2023 and ran up 65% in four months. Abercrombie & Fitch , one of 2023’s best-performing stocks, had a 94 rating before it soared 342% in nine months starting in June 2023.

Those stocks weren’t flukes. In a study of the biggest stock-market winners from the early 1950s through 2008, the average RS rating of the best performers before they began their major price runs was 87.

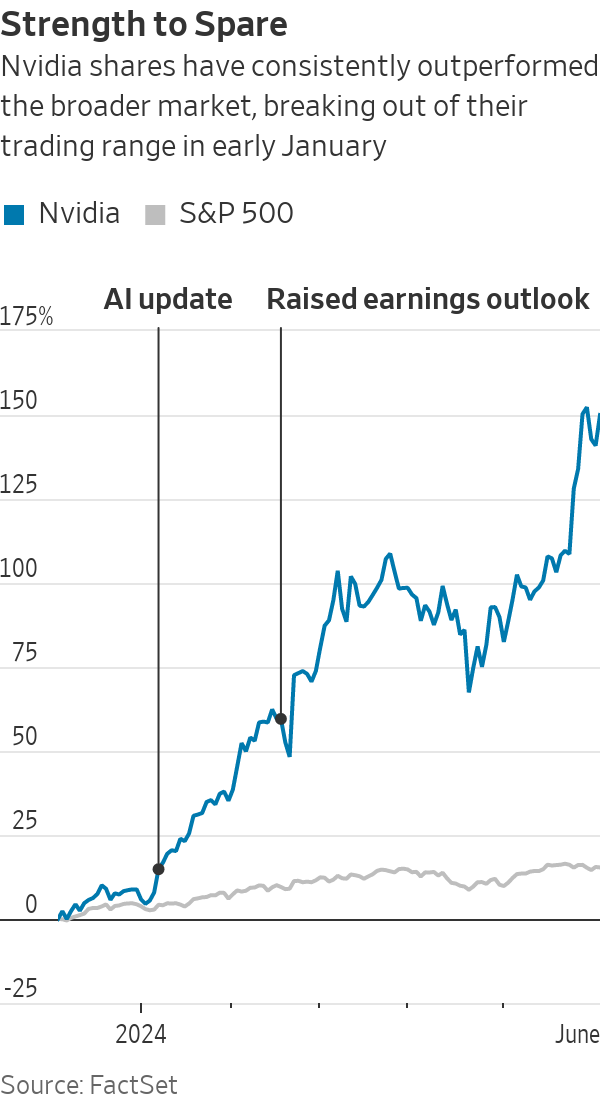

To see relative strength in action, consider Nvidia . The chip stock was an established leader, having shot up 365% from its October 2022 low to its high of $504.48 in late August 2023.

But then it spent the next four months rangebound—giving up some ground, then gaining some back. Through this period, shares held between $392.30 and the August peak, declining no more than 22% from top to bottom.

On Jan. 8, Nvidia broke out of its trading range to new highs. The previous session, Nvidia’s RS rating was 97. And that week, the stock’s relative strength line hit new highs. The catalyst: Investors cheered the company’s update on its latest advancements in artificial intelligence.

Nvidia then rose 16% on Feb. 22 after the company said earnings for the January-ended quarter soared 486% year over year to $5.16 a share. Revenue more than tripled to $22.1 billion. It also significantly raised its earnings and revenue guidance for the quarter that was to end in April. In all, Nvidia climbed 89% from Jan. 5 to its March 7 close.

And the stock has continued to run up, surging past $1,000 a share in late May after the company exceeded that guidance for the April-ended quarter and delivered record revenue of $26 billion and record net profit of $14.88 billion.

Ken Shreve is a senior markets writer at Investor’s Business Daily. Follow him on X @IBD_KShreve for more stock-market analysis and insights, or contact him at ken.shreve@investors.com .

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.