Europe Is Still In The Throes Of Covid-19, But Its Stocks Are Rallying

Certain shares surge as investors look for beaten-down stocks.

By Anna Hirtenstein

Mon, Mar 15, 2021 2:08pm 3 min

3 min

3 min

Certain shares surge as investors look for beaten-down stocks.

3 min

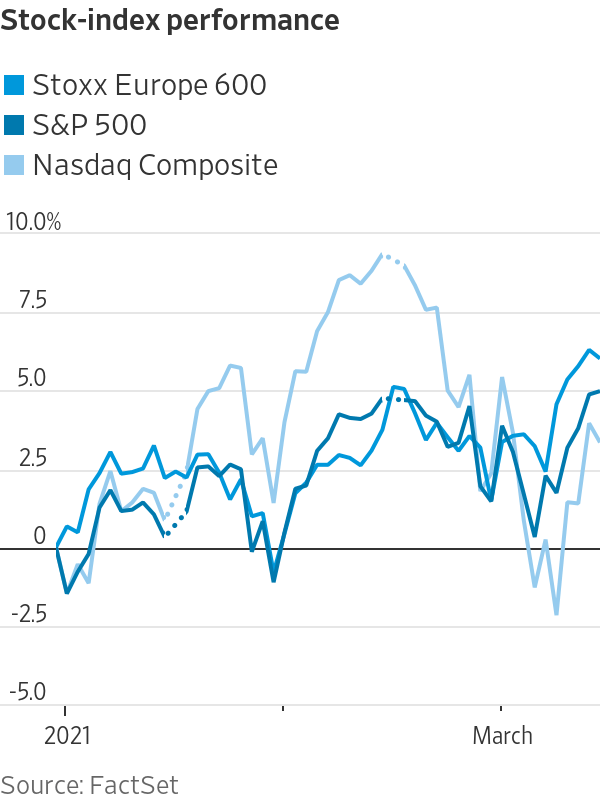

European stocks have been on the rise as international investors reposition their portfolios for the global economy to return to normal—a trade that hinges on smooth reopenings in the region.

The pan-continental Stoxx Europe 600 index has gained 4.5% so far this month, pulling ahead of major U.S. gauges, and on Friday hovered close to its highest point in more than a year. The S&P 500 has added 3.5% in the same period and the Russell 2000, an index of small-cap U.S. companies, has increased 6.9%. The Nasdaq Composite has gained 1% so far this month.

Analysts say this is due to a rotation from growth to value stocks: Investors have been snapping up shares of companies hit hard by the pandemic and selling those that benefited from stay-at-home orders. Europe is emerging as a beneficiary of this trade, which banks on a strong economic rebound.

“Europe is predominantly a value market, the U.S. is predominantly a growth market,” said Kasper Elmgreen, head of equity investing at Amundi. “This rotation benefits Europe disproportionately.”

Value stocks are thought to be trading below what they are currently worth. They are typically in established industries and pay dividends, and include banks, energy and industrial companies, which are also more sensitive to the economic cycle. Growth companies are younger and perceived to be innovative, with potential to do well in the future, such as technology.

But delays to the European Union’s procurement of vaccines is likely to result in its member states keeping social-distancing and travel restrictions in place for longer than countries that are inoculating their populations faster, such as the U.S. and Israel. This might mean that Europe’s economic rebound is slower and weaker. Italy reimposed stricter curbs in several regions last week and plans to lock down nationally over Easter.

“We are finding a little bit more opportunity outside of the U.S. [Value stocks] look cheaper and more undervalued overseas,” said Brent Fredberg, director of investments at Brandes Investment Partners in San Diego. “Now you’ve still got a long way to go in many of these companies, even though they’ve rallied hard.”

A key reason for Europe’s recent strong stock-market performance is the composition of indexes. The Stoxx Europe 600 is more heavily weighted toward industries that are considered to be value, such as financials at 17%, industrials at 16% and energy companies at 5%. Its weighting for technology and communications is 10%, compared with 37% for the S&P 500.

Amundi’s Mr Elmgreen has bought shares of European auto makers and companies that produce construction materials recently, and said he is “significantly underweight” U.S. tech, meaning he owns less than the benchmark he tracks.

Another driver of Europe’s performance is the bond market. The sense of optimism about economic growth has also driven fund managers to dump safe-haven assets such as sovereign debt, causing yields to rise and prices to drop. Government bond yields are used as a reference for the cost of debt in the broader market, including loans to companies. That rise in yields implies higher financing costs, benefiting lenders.

European banks have been among the best performers so far this year. Investors have been expecting the recent rise in yields to improve their net interest income, a key source of revenue. French bank Natixis SA has surged 47%, while Amsterdam-based ING Groep NV and Spain’s Banco de Sabadell SA have both risen 32%.

The Vanguard FTSE Europe ETF is up 5.6% for the year and the iShares Europe ETF has also risen 5.5%. Another iShares ETF that invests in European financial firms has climbed 12%.

Companies in sectors still curbed by government restrictions have also jumped. German travel company TUI AG is the biggest winner on the Stoxx Europe 600 this year, soaring 56%. International Consolidated Airlines SA has added 39% and InterContinental Hotels Group PLC has risen 15%.

But whether these gains are justifiable is still a question, according to Simon Webber, a portfolio manager at Schroders with a focus on global equities. “Travel has fundamentally changed, people are used to working productively, meeting and supporting customers remotely,” he said. Aviation stocks in particular “will be heavily scrutinized,” he added.

He has increased his holdings of European banks, but is also looking at buying more growth stocks such as electric-vehicle companies.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Automobili Lamborghini and Babolat have expanded their collaboration with five new colourways for the ultra-exclusive BL.001 racket, limited to just 50 pieces worldwide.

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

2 min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.