America Had ‘Quiet Quitting.’ In China, Young People Are ‘Letting It Rot.’

Demoralised by a weak economy and unfulfilling jobs, young Chinese are dropping out, exploring spirituality and becoming more rebellious, presenting new challenges for Beijing

By SHEN LU

Tue, Dec 19, 2023 9:55am 7min

Li Jiajia, 24, says she found herself unmotivated to climb the ranks after she joined a startup in Beijing. PHOTO: GILLES SABRIE FOR THE WALL STREET JOURNAL

China’s ruling Communist Party wants the country’s young people to be ambitious, work hard and prepare for adversity.

Li Jiajia just wants to win the lottery.

Demoralised by a weak economy, unfulfilling jobs and a paternalistic state, young Chinese such as Li are looking for pathways out of the carefully scripted lives their elders want for them, putting themselves at odds with the country’s priorities.

After moving to Beijing from her hometown in southeastern China in April, the 24-year-old Li found her new job as a content creator at a technology startup uninspiring. She said she has no desire to climb the corporate ladder, especially when the number of high-paying Chinese tech jobs is shrinking.

The ever-present role of the state in daily life is stultifying, she said. Though she wanted to be a journalist in high school, she gave up when she realised how heavily the government censors the media.

For Li, scratching lottery tickets offers a moment of escapism. PHOTO: GILLES SABRIE FOR THE WALL STREET JOURNAL

She says she knows she probably won’t win the lottery. But when she plays, at least she can dream of a better life—most likely abroad.

“I want to leave here and live the life I want,” Li said. “It won’t happen overnight, but for now, the thrill of scratching lottery tickets gives me a little break.”

Since China’s government cracked down on disaffected students in Tiananmen Square in 1989, most young people, who came of age in an era of rapid economic growth and rising affluence, have done what they are supposed to do—and been rewarded for it.

They studied diligently to get into prestigious universities, clocked gruelling hours at fast-growing companies and followed traditional expectations of career and family, riding China’s boom to material success.

Many are still doing that. But a growing number of middle-class urbanites in their 20s and 30s in China have begun to question that trajectory, if not reject it entirely, as prospects of upward mobility fade.

More than two years of harsh government Covid controls left some pondering the role of the Communist Party and other sources of authority in their lives, or even the meaning of life and who they aspire to be—questions many had never contemplated before.

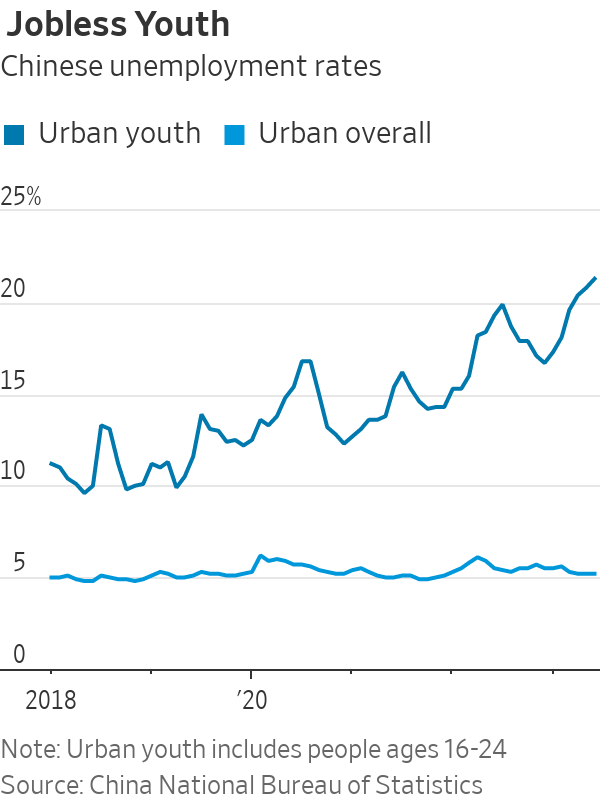

Record youth unemployment that topped 21% this year has further dented confidence in traditional paths to achievement in China. Some, like Li, are also frustrated about other issues, such as violence against women in China or government efforts to prevent people from accessing foreign apps such as Twitter or Instagram.

Many are quitting their jobs and turning to meditation and other forms of spirituality. Some are moving far from China’s megacities to start lives anew in places like Dali, a southwestern city famous within China as a hub for digital nomads and dropouts.

Others are flooding fortune-teller stands and Buddhist temples in mountainous areas, or exploring Chinese and Western philosophers and writers from Laozi to Hermann Hesse. Some are throwing “quitting parties” with banners celebrating their newfound freedom.

“This generation has had a lot of resources invested in them,” said Sara Friedman, professor of anthropology and gender studies at Indiana University, who studies Chinese society.

“They have worked really hard. They have been pushed really hard. And to then say, ‘I’m stepping out of this rat race, I’m opting out,’ is a pretty radical decision to be making.”

Young visitors pray at the Lama Temple in Beijing. PHOTO: GILLES SABRIE FOR THE WALL STREET JOURNAL

From ‘lying flat’ to ‘letting it rot’

Social-media discussions about temple visits and anxiety—a central preoccupation of many young Chinese—have surged in 2023, according to BigOne Lab, a research firm.

About 34% of surveyed respondents in their mid-20s quit or were considering resigning from jobs in China’s consumer internet sector—a major employer of young people—in the first half of 2023, according to China’s job-seeking and social platform Maimai.

Playing the lottery has become especially trendy for 20- and 30-somethings, whose purchases of lottery tickets helped push sales to $67 billion from January to October, a 53% jump from the previous year and averaging $48 per person in China.

Catchphrases describing the mood have worked their way into everyday discourse. First, in 2020, was the arcane sociological term neijuan, or “involution,” which referred to situations in which people work hard and compete without anyone getting ahead.

That was followed by “touching fish.” The phrase, borrowed from a Chinese idiom, referred to executing small rebellions at work, such as taking long toilet breaks, doing online shopping or reading novels in the office.

Next was “lying flat,” a form of mundane resistance that involves dragging one’s feet at work or dropping out of the workforce altogether. Last year, the phrase “let it rot” spread to describe young people who have completely given up.

A survey conducted by Tsingyan Group, a research firm, last year found that approximately 96% of nearly 6,000 respondents in China were aware of people “lying flat” to various degrees in their vicinity. The concept held more appeal among people ages 26 to 40 than other Chinese, the survey showed.

“It’s a very passive form of resistance,” said Silvia Lindtner, an ethnographer at the University of Michigan. “It’s definitely a very difficult moment, but it could also be seen as a hopeful moment where there is pressure, in some ways, on the leadership.”

Echoes of the 1960s

In some ways the ennui resembles the “quiet quitting” phenomenon of postpandemic America—or, going back further, the rejection of social norms by young people across the Western world in the 1960s.

In those days, two decades of fast economic growth and wider affluence gave young people more choices than previous generations. Many responded by challenging their parents’ way of life.

For many young urbanites in cities such as Beijing, traditional paths to success have become less reliable and less attractive. PHOTO: GILLES SABRIE FOR THE WALL STREET JOURNAL

In China, where open protests are rarely possible, young people are now rebelling in other ways.

“Lying flat is a latent resistance to the moral blackmailing of society,” said Amy Yan, a 27-year-old Shenzhen resident who once worked as a buyer for her family’s export business. When the business went bankrupt last year after her parents lost their assets in a financial scam, it reinforced her belief that she should give priority to her spirituality.

Even before the bankruptcy, she had decided that accepting the corporate grind and meeting traditional expectations of marriage and children would interfere with her desire to explore her spirituality.

Following the family crisis, she put her savings of $27,000 into supporting a tiny Taoist ashram she had started with a few fellow practitioners.

Coming into Beijing’s crosshairs

Communist Party leaders have long worried young people could stir unrest, as they did in 1989. The party needs young people to get on board with Beijing’s priorities, not just to keep the economy humming and avoid instability, but to help make China stronger in an era of great-power competition with the U.S.

In a speech at last year’s Communist Party congress, widely quoted in Chinese media, leader Xi Jinping laid out his vision for young people, urging them to have “ideals, courage, a willingness to endure hardship and a dedication to strive” to help “build a modernised socialist country.”

In a 2021 article published in the top party journal Qiushi, he specifically warned against “lying flat.” Discussions of the phenomenon have often triggered censorship online.

If all the young people who had dropped out of China’s labor force and relied financially on their parents were counted, China’s real youth unemployment rate could be as high as 46.5%, according to calculations earlier this year by a Peking University professor.

The Communist Party Youth League—with more than 70 million members—has published commentary on its official WeChat account criticizing college graduates for having too much pride. Job seekers “should not refuse to enter the workforce due to the difficulty of finding a job or choose to ‘lie flat’ out of fear of ‘involution,’” the article read.

Greater affluence—but an uncertain future

Until recently, China’s economic progress seemed to be unstoppable, with per-capita incomes surging to around $13,000 in 2022 from less than $1,000 in 2000, according to the World Bank.

But economic growth has slowed. Many economists worry China could get stuck in the “middle-income trap,” in which a country’s progress plateaus before it gets rich. Per-capita incomes in the U.S. were around $76,000 last year.

Academic research shows that social mobility for many groups in China has stalled, meaning it has become harder for people without connections to get ahead.

Many employers that young people gravitated to, including Alibaba, Tencent and ByteDance, have been shedding staff amid weak growth and government clampdowns on the private sector. Tech salaries have declined in the past three years, according to Maimai, and opportunities for initial public offering payouts have faded, leaving many who used to work “996” schedules—9 a.m. to 9 p.m., six days a week—wondering what the point was.

It is also true that many more middle-class young people—especially those without children and mortgages—can afford to drop out of the rat race today than in previous eras.

Some plan to leave: Net emigration from China, which fell to 125,000 in 2012 as the country’s economy boomed, rebounded to more than 310,000 in the first 11 months of 2023, according to United Nations data.

Others want to stay—but on their own terms.

Huang Xialu quit her high-stress job as a product manager at one of China’s largest video-streaming companies in April, so she could focus more on spiritual retreats. For a long time before that, the 33-year-old said she had struggled with a lack of purpose.

“I had a very urgent sense that if I didn’t listen to my gut and take a break to explore what I truly wanted to do in this world, it would be too late,” she said.

In the months following Huang’s resignation, she traveled to Dali, where she worked on a tarot-reading stand, took a training course in life coaching and learned to make pottery.

To Huang, lying flat is the opposite of being passive—it is a path for taking control of one’s own life when wading through uncertain terrain, she said.

Now she has become a certified life coach, helping individuals who are as confused as she was to find a way forward. Her income is less stable.

But “I haven’t regretted quitting for a second,” she said.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Related Stories

Money

Celebrity-backed fund nears US$50m as investor demand builds

By Jeni O'Dowd 02/06/2026

Money

What Is Artemis II? The NASA Mission to Fly Astronauts Around the Moon

By Micah Maidenberg 30/03/2026

Money

Saudi Arabia Sees a Spike to $180 Oil if Energy Shock Persists Past April

By SUMMER SAID, RYAN DEZEMBER AND DAVID UBERTI 20/03/2026

With US$40 million already committed, the Global Talent Fund is attracting investor attention with a strategy focused on building globally scalable consumer brands alongside high-profile talent.

By Jeni O'Dowd

Tue, Jun 2, 2026 2min

A new investment fund targeting celebrity-founded consumer brands has secured US$40 million in commitments and is rapidly approaching its US$50 million fundraising target, signalling growing investor appetite for alternative opportunities beyond traditional asset classes.

The Global Talent Fund, which has a maximum raise of US$100 million, focuses on building and investing in consumer businesses alongside celebrities, athletes, and influential personalities who play an active role as co-founders rather than simply endorsing products.

The strategy is based on the belief that changes in consumer behaviour, particularly the rise of social media and digital engagement, have fundamentally altered how brands are built and scaled.

GTF founding partner Jeremy Hunt, who is helping lead the fund’s strategy, said consumers increasingly feel connected to personalities they follow online and are more willing to support products developed by those individuals.

“Consumers are searching for content to engage with, and when a celebrity they like or follow takes them on the journey of creating a product or brand, they genuinely feel part of that process,” he said.

The fund is targeting high-growth consumer sectors including wellness, hydration, beauty and recovery, areas Hunt believes continue to benefit from strong global demand and ongoing innovation.

Rather than backing celebrity endorsement deals, the fund is seeking businesses where talent is deeply involved in product development, brand creation and long-term growth.

According to Hunt, authenticity remains one of the biggest differentiators between successful celebrity-backed brands and those that fail.

“The consumer can see clearly if someone is simply being paid to promote a product,” he said. “The winners are typically the brands where the celebrity has genuinely helped build the business from the ground up.”

The model has attracted support from several prominent Australian investors and business families, reflecting broader interest in alternative investments with global growth potential.

Hunt said consumer brands offered a level of tangibility that many investors found appealing.

“Consumer brands are what we touch, feel, smell and taste every day,” he said. “Our investors understand the growth potential in the model, but they also want to be part of the journey.”

The fund’s rapid progress towards its fundraising target comes amid growing recognition that celebrity influence, when combined with strong commercial execution and scalable business models, can create significant enterprise value.

With several high-profile celebrity-founded businesses generating billion-dollar exits in recent years, supporters of the strategy believe the opportunity remains in its early stages.

7 min

7 min

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.