Stocks Are Crashing—That’s a Great Reason to Sit Tight

The sudden sell off in Japanese equities and a surge in the VIX suggest the current rout is being exaggerated by trend chasers

By

JON SINDREU

Tue, Aug 6, 2024 11:51am 4 min

4 min

The red numbers in your 401(k) today might appear to vindicate warnings about an artificial-intelligence bubble and infirm economy. But don’t tilt your portfolio toward full pessimism just yet.

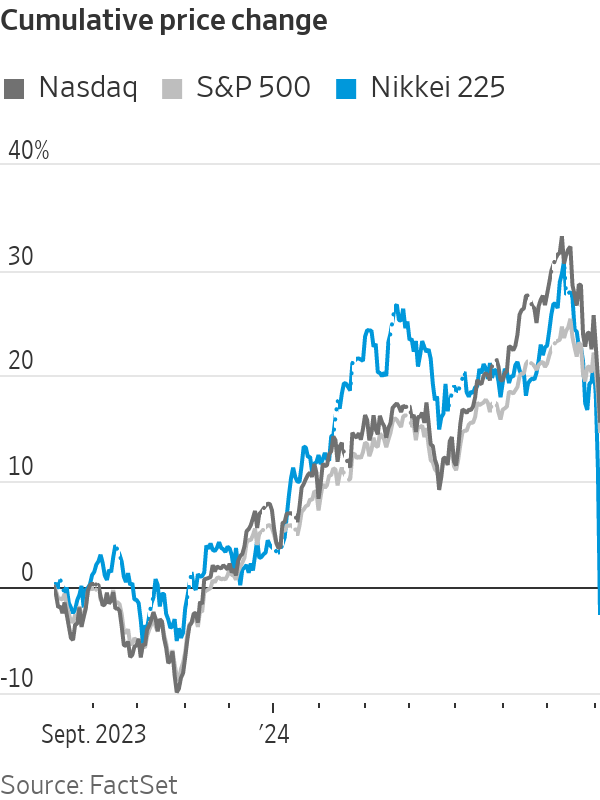

The S&P 500 was down 3% Monday, with the Nasdaq falling even further. Investors have been selling the year’s best performers, concerned that disappointing second-quarter results from big technology companies such as Alphabet , Tesla and Intel are a sign that the AI frenzy is a fad. Also, consumer discretionary stocks have become the worst-performing sector in the S&P 500, as lacklustre labour-market reports have raised worries that the Federal Reserve made a mistake by waiting until September to cut interest rates.

Overseas, the Stoxx Europe 600 closed almost 5% below where it was a week ago, whereas the Swiss franc, a common haven asset, is up roughly 4%. The most eye-popping moves happened in Asia, though, where the Nikkei 225 plunged 12.4% Monday in the worst trading session since Oct. 20, 1987—the day that followed Wall Street’s infamous Black Monday.

Yet it is precisely the breakneck speed with which Japanese equities tumbled that should give most investors a reason to remain calm.

As a guideline, sudden market selloffs are less dangerous than those that unfold progressively over time. This is because investors who rationally price in bad economic data often do so slowly, as it trickles in. Flash crashes, conversely, are often a sign that some tidbit of bad news made speculative bets go awry, triggering a cascade of trades, many of them automated.

Japan is particularly prone to such reversals because interest rates there are so low that many investors use them to fund higher-yielding investments in other currencies. Whenever markets get jittery, these “carry trades” tend to unravel, pushing up the yen and hitting Japanese stocks, many of which are diversified exporters that do better when global growth accelerates. Amplifying this tendency, Japanese stocks had this year become extremely popular among global investors.

The timing of the rout also points a finger at the Bank of Japan , which last week decided to tighten monetary policy for the first time in 17 years with the explicit goal of boosting the yen. Investors who rushed to cover their bets then triggered the reversal of stretched trades elsewhere, including in the U.S.

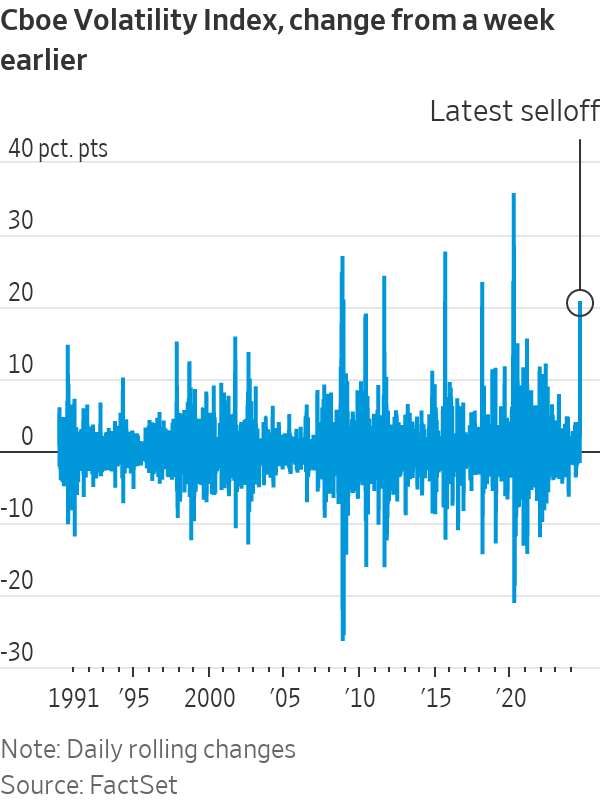

One of the most striking features of the S&P 500 for most of this year has been its extremely low volatility. Until July, the Cboe Volatility Index, or VIX, was at 2019 levels, and kept sliding lower even as investors made big changes to their monetary-policy forecasts.

While the VIX is often dubbed Wall Street’s “fear gauge,” the options contracts it is based on often themselves influence volatility. Whenever investors make bets against market swings, as they have recently in the U.S. by buying lots of structured products , the banks that sell those options are forced to take the other side. These hedges then suppress volatility in the stock market.

The flip side is that whenever a panic breaks through this feedback loop, volatility skyrockets. As the stock market opened Monday, the VIX hovered above 50, making it the highest weekly jump since the onset of the pandemic, though it later fell below 40.

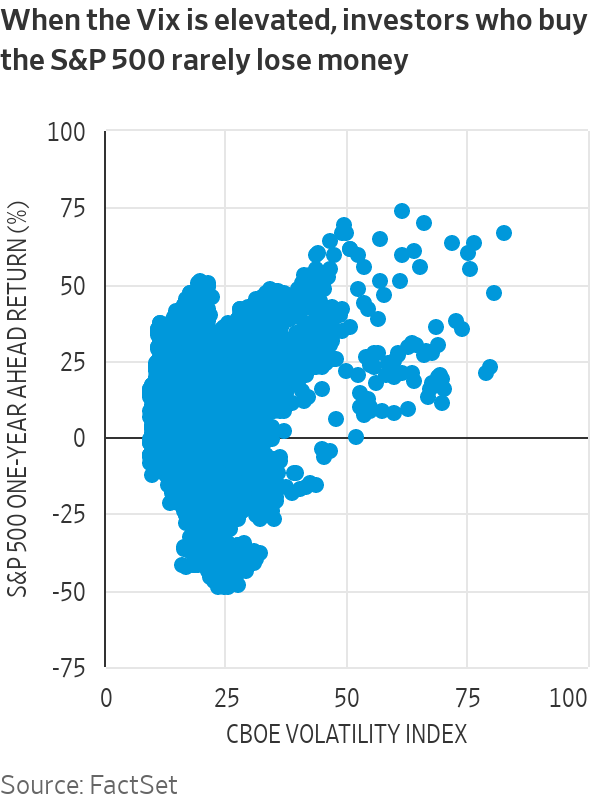

This suggests the selloff is disproportionate, especially looking at the historical record: 87% of the time, investors who bought the S&P 500 on days when the VIX closed at 30 or higher ended up making money a year later.

The second-quarter reporting season has brought mostly good news, with 78% of the S&P 500 firms that have reported so far beating analysts’ earnings estimates—compared with a 74% 10-year average. Both AI-related companies and the rest are reporting net income above what was forecast a month ago. Overall, the U.S. economy still looks robust: The unemployment rate has gone up because the labor force has expanded.

Also, looking at S&P 500 returns since 1994 shows that selling based on the previous day’s falls is a bad strategy. Electing to move into cash after large monthly declines fared better, but still less well than sitting tight.

This isn’t to say that concerns about an economic slowdown or high tech valuations aren’t warranted. Investors have reasons to diversify away from the AI trend or swap more cyclically exposed stocks for more “defensive” names. Indeed, selling out of stocks after particularly exuberant days and months has historically tended to be a winning move. But hindsight is a terrible guide to investing your savings.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.