Are Low Interest Rates A Risk to the Property Market and Economy?

As MSQ Capital’s Managing Director Paul Miron sees things, we’re pawns to a rather significant economic experiment.

By

Paul Miron

Fri, Apr 9, 2021 11:17am 4 min

4 min

OPINION

It is to the astonishment of most economists, politicians and property experts that we are experiencing an extraordinary V shape recovery.

This week’s fundamental economic good news is that the unemployment rate has fallen to 5.8%, smashing expectations. The property market seems to be booming, job adverts are increasing and consumers are now freely going back to pre-Covid-19 spending levels. Millennials are once again ordering smashed avocados whilst leisurely completing their online home loan applications in order to begin the hunt for their first property purchase. That debut purchase, mind you, is now mostly sponsored by the government’s extraordinarily generous schemes, such as ‘home builder’ ($2billion worth) and other various grants (providing up to $50,000 per person).

This is a far cry from expectations a year ago, when Prime Minister Scott Morrison sternly prepared Australians for a 6-month hibernation, followed by a high unemployment rate and a long and hard economic recovery.

Despite current positive economic euphoria, there are some very respected and seasoned investors, politicians and economists who are extremely worried — of the view that the economic recovery, both locally and internationally, is founded on fragile thin ice.

There is a high risk that both our local economy and international economies may generate inflation past the prescribed target of the 2%-3% tolerance of central bankers around the world. This would place the RBA Governor, Philip Lowe, under significant pressure to increase interest rates, despite his assertions that rates will stay put for at least 3 years.

Lowe’s motivations would be to avoid the undesirable economic and social impacts of hyperinflation, akin to past historical experiences that lead to the Great Depression of the ‘30s, the late ’70s oil crisis and the ’80s, where many people can remember living through official interests of 18.5%.

During the past few weeks we’ve seen a number of global central bankers — notably as those from Russia, Brazil and Turkey, among others — increase their official interest rates as their economies simply do not have the financial capacity to continue printing money as freely as our economy.

Increase in interest rates would put downward pressure on asset classes such as property and shares, whilst undermining consumer confidence — resulting in lower spending and impeding a full economic recovery.

The current unemployment trend would very quickly change from positive to negative. The most alarming comment is that both monetary and fiscal policies have pretty much been exhausted during the pandemic. Worse still, if the Government was unable to support the market, it could lead to a market collapse like the crashes of 1987 and 2004 and the various property market corrections we have experienced in the past.

The rationale for such divergence of economic opinion is fundamentally based on the fact that we’re living through an economic experiment. The combination of monetary and fiscal policy employed by the Government and RBA has never before been tested — think zero interest rates, Quantitative Easing, Job Keeper, Job Seeker and mortgage payments deferrals to name but a few.

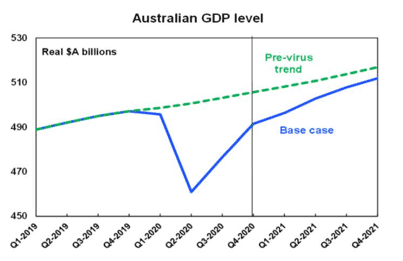

Another way to appreciate this is via the below graph prepared by AMP. It demonstrates the hypothetical green line if Covid-19 had not happened. The blue line depicts actual GDP figures.

Despite Australia’s GDP being in excess of 3% for the past two quarters (for the first time ever), we remain 2.4% below than what we would have been if Covid-19 never arrived. Our unemployment was mid 4% pre-Covid, with wage growth peaking at a mere 1.4%p.a., whereas today unemployment sits 5.8%.

It is the RBA’s fundamental economic assumption that in order for inflation to shoot past 3% maximum traditional target, interest rates must be kept low and we require the unemployment rate to fall to 3%. This is because in the current economic situation, wage inflation is the key element to push overall inflation. According to many economists, it could take years for unemployment to reach a rate below 4% and which therefore supports the RBA’s expectation.

The estimated financial cost to future tax payers to ensure we have this V shape recovery is estimated to be circa $350b, roughly 17% of our GDP. This is 5 times larger than any stimulus that was provided during the GFC.

And so, despite the surging asset values, it is unlikely for the economy to suddenly overshoot the green line while a number of industries, such as tourism and international students, remain subdued (and let’s not forget those industries being targeted in our ongoing trade war).

The true economic recovery picture will be seen in the next two quarters of GDP figures, where either the fear of inflation will abate or crystallise into reality.

Paul Miron has more than 20 years experience in banking and commercial finance. After rising to senior positions for various Big Four banks, he started his own financial services business in 2004.

msqcapital.com