Things I miss about my local gas station:

…

That’s it. That’s the list. OK, fine, I did enjoy the communal squeegees.

This week marks six months since the grand opening of my home electric-vehicle charging station. Congrats to the whole team! (Me and my electrician.) Located between my garage door and recycling bin, it’s hard to beat for the convenience. And also the price.

If you’ve followed my ad-EV-ntures, you’re aware of my feelings about the hell that is public EV charging , at least before Tesla started sharing its Superchargers with its rivals. Truth is, I rarely go to those public spots. The vast majority of EV owners—83%—regularly charge at home, according to data-analytics company J.D. Power.

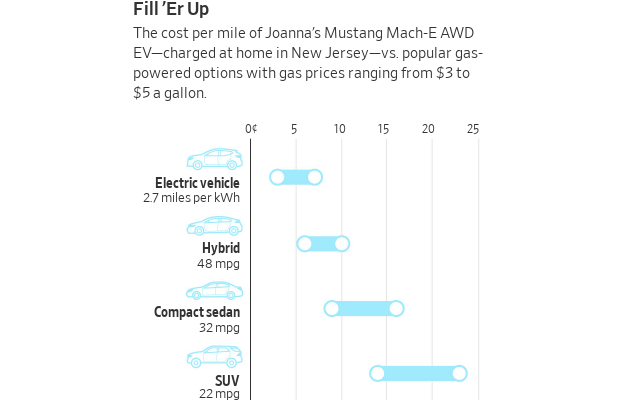

I already discovered many EV virtues , but I didn’t quite grasp the cost savings until I tallied up half a year of home-charging data. In that time, I spent roughly $125 on electricity to drive just under 2,500 miles. In my old car, that would have cost me more than twice as much—assuming gas held steady at around $3.25 a gallon . And I was charging through the winter, when electricity doesn’t stretch as far in an EV.

Rebates and programs from my state and utility company sweeten the deal. So I will be able to take advantage of discounted electricity, and offset the cost of my charger. The same may be available to you.

But first, there are technical things to figure out. A 240-volt plug? Kilowatt-hours? Peak and off-peak charging? While other people are in their garages founding world-altering tech companies or hit rock bands, I’m in there finding answers to your home-charging questions.

How to get set up

Sure, you can plug your car into a regular 120-volt wall outlet. (Some cars come with a cable.) And sure, you can also simultaneously watch all of Netflix while it charges. It would take more than two days to fill my Ford Mustang Mach-E’s 290-mile battery via standard plug, known as Level 1 charging.

That’s why you want Level 2, which can charge you up overnight. It requires two components:

• A 240-volt electric outlet. Good news: You might already have one of these higher-powered outlets in your house. Some laundry dryers and other appliances require them. Bad news: It might not be in your garage—assuming you even have a garage. I realise not everybody does.

Since my suburban New Jersey home has an attached garage, the install process wasn’t horrible—or at least that’s what my electrician said. He ran a wire from the breaker panel in the basement to the garage and installed a new box with a NEMA 14-50 outlet. People with older homes or detached garages might face trickier wiring issues—more of a “Finding NEMA” adventure. (I apologise to everyone for that joke.)

My installation cost about $1,000 but the pricing can vary widely.

• A smart charger. Choosing a wall charger for your car is not like choosing one for your phone. These mini computers help you control when to start and stop charging, calculate pricing and more.

“This is not something where you just go to Amazon and sort for lowest to highest price,” said Tom Moloughney, the biggest EV-charging nerd I know. On his website and “State of Charge” YouTube channel , Moloughney has reviewed over 100 home chargers. In addition to technical measurements, he does things like freezing the cords, to see if they can withstand wintry conditions.

“Imagine you are fighting with this frozen garden hose every time you want to charge,” he said.

One of his top picks, the ChargePoint Home Flex , was the same one my dad had bought. So I shelled out about $550 for it.

Just remember, if you want to make use of a charger’s advanced features—remote controls, charging updates, etc.—you’ll also need strong Wi-Fi in your garage.

How to save money

I hear all you money-minded WSJ readers: That’s at least $1,600 after getting the car. How the heck is this saving money? I assumed I’d recoup the charging-equipment investment over time, but then I found ways to get cash back even sooner.

My utility provider, PSE&G, says it will cover up to $1,500 on eligible home-charger installation costs . I just need to submit some paperwork for the rebate. In addition, New Jersey offers a $250 rebate on eligible charger purchases. (Phew! My ChargePoint is on the list.) If all is approved, I’d get back around $1,250. Fingers crossed!

I didn’t know about these programs until I started reporting on this. Nearly half of home-charging EV owners say they, too, are unaware of the programs offered by their electric utility, according to a 2024 study released by J.D. Power . So yes, it’s good to check with your provider. Kelley Blue Book also offers a handy state-by-state breakdown.

How to charge

Now I just plug in, right? Kinda. Even if you have a Level 2 charger, factors affect how many hours a fill-up will take, from the amperage in the wall to the current charge of your battery. Take Lionel Richie’s advice and plan on charging all night long .

It can also save you money to charge during off-peak hours.

Electricity costs are measured in kilowatt-hours. On my basic residential plan, PSE&G charges 18 cents per kWh—just 2 cents above the 2023 national average . My Mustang Mach-E’s 290-mile extended-range battery holds 91 kilowatt-hours.

Translation: A “full tank” costs $16. For most gas-powered cars, that wouldn’t cover half a tank.

And If I’m approved for PSE&G’s residential smart-charging plan, my off-peak charging (10 p.m. to 6 a.m. and weekends) will be discounted by up to 10.5 cents/kWh that I’ll get as a credit the following month. I can set specific charging times in the ChargePoint app.

Electricity prices fluctuate state to state but every expert I spoke to said no matter where in the country you live, home charging should cost less than half what gas would for the same mileage. (See chart above for a cost comparison of electric versus gas.) And as I’ve previously explained , fast charging at public stations will cost much more.

One big question: Am I actually doing anything for the environment if I’m just taxing the grid? Eventually, I’d like to offset the grid dependence—and cost—by powering my fancy little station with solar panels. Then, I’ll just be missing the squeegee.

4 min

4 min

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.