HONG KONG’S PROPERTY MARKET IS A MESS—AND THE FED IS PARTLY TO BLAME

U.S. rate increases have tamed inflation at home but caused pain elsewhere

By ELAINE YU

Tue, Aug 8, 2023 10:23am 4 min

4 min

4 min

U.S. rate increases have tamed inflation at home but caused pain elsewhere

4 min

Hong Kong’s notoriously expensive property market is often seen as a barometer of the city’s economy. It isn’t looking good.

Home prices are down. Office vacancy rates have hit a record high. Commercial real-estate investment has plummeted. The shares of some big developers in the city are trading at a 30-year low to their net asset value, a measure of financial health, according to research by analysts at JPMorgan.

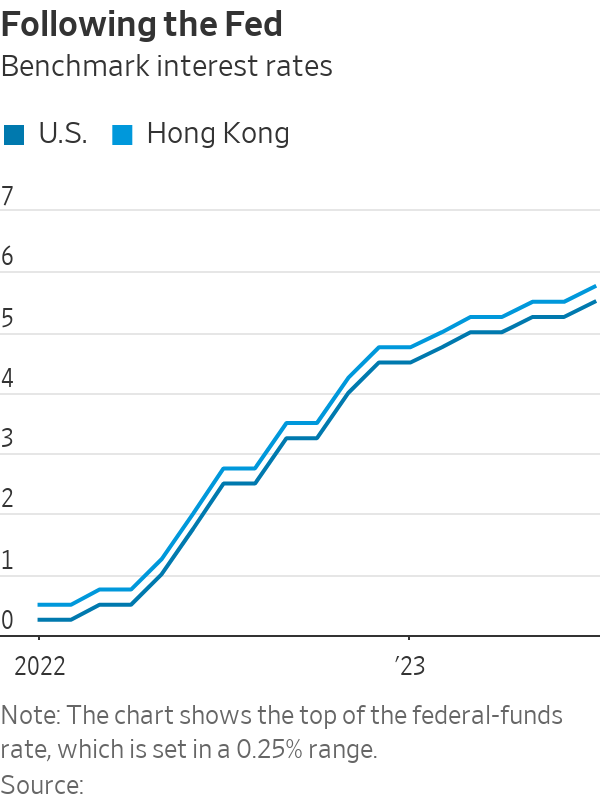

A key reason is high interest rates, which have increased the burden on mortgage-paying home buyers, said Cathie Chung, senior director of research at Jones Lang LaSalle, a real-estate services company. The Hong Kong dollar’s peg to the U.S. dollar forces monetary authorities in the city to track U.S. interest-rate decisions, limiting their ability to stimulate the property sector and the wider economy.

The Federal Reserve has embarked on a historic cycle of interest-rate rises since last March, raising the benchmark federal-funds rate from around zero to 5.25% to 5.50%. The Hong Kong Monetary Authority, the city’s de facto central bank, has followed these hikes, increasing its base rate to 5.75% from 0.75% over the same period.

The full impact of higher interest rates in the city still hasn’t been felt, said Asif Ghafoor, chief executive of online real-estate marketplace Spacious. Asking prices of residential properties listed on the platform have fallen 5% since the start of the year. Sales prices tend to follow suit, and are likely to fall 5% to 10% in the next six months, he said.

To prop up the market, the HKMA relaxed mortgage rules in early July for the first time since 2009, allowing home buyers to pay less upfront and borrow more for some properties if they plan to live in them. But those working in the sector think the pain is far from over.

“We expect that the recovery will be slow and long,” said Chung at Jones Lang LaSalle.

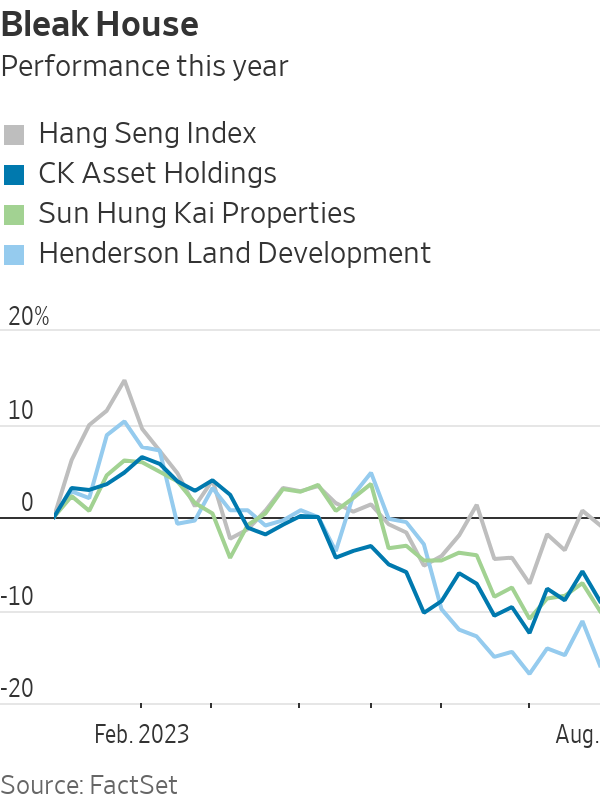

The slump in the property market has hurt the share prices of developers, a major source of wealth for some of the city’s richest families. CK Asset Holdings, Henderson Land Development, Sun Hung Kai Properties and New World Development—all still partly owned by the families of the founders—are performing much worse than the wider stock market this year. New World and Henderson Land have lost more than 15% this year, according to FactSet data.

Hong Kong is one of the world’s leading financial centres and is seen by many foreign businesses as a gateway to mainland China. It is now being hit by a slowdown in investment-banking activity—with several large banks cutting staff this year—and the shaky recovery of China’s economy, which has undermined confidence among businesses and potential home buyers in Hong Kong.

The overall vacancy rate for offices reached a record high of 15.7% in the first half of this year, compared with an average of under 5% in 2018, according to figures by CBRE. In the central business district, there was almost eight times as much empty office space as in 2018, when the area had a vacancy rate of just 1.3%.

The equivalent of $603 million was invested in commercial real estate between April and June, according to CBRE data, just a third of the first-quarter tally and the lowest quarterly figure since the end of 2008, when the global financial crisis caused a huge drop in confidence.

Hong Kong’s border with mainland China was reopened earlier this year, but companies from the mainland haven’t grabbed office space in the numbers many had hoped, said Ada Fung, head of office services at CBRE Hong Kong. Flexible working arrangements and geopolitical tensions that have made many companies pause expansion plans are also crimping demand, she said.

The drop in demand is being exacerbated by a supply glut. Developers bought land and started constructing a number of new buildings before 2019, when widespread protests rocked the city and only ended with the passing of a strict national-security law. Demand for commercial property after that was soon undermined by the spread of Covid-19.

This shift in supply and demand is finally giving potential renters the upper hand, said Fung. “It could be a healthy reset,” she said.

There are some reasons for optimism. Retail businesses have increased their demand for commercial property after the reopening of the border with China, which has brought in tourists looking to spend on luxury goods. There is also hope that a recent rise in residential rents could help home prices.

After an exodus of professionals and other residents in recent years, people have started to move to the city, including foreign students and those coming to Hong Kong through government talent schemes designed to reverse a brain drain. That is helping rents pick up after hitting a bottom in the first quarter, and could lead to more demand for properties as investments, said Cusson Leung, head of property research in Hong Kong at JPMorgan.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

The imposing stone structures, with towers, turrets and a hot tub room, lord over the landscape near the mountain resort town of Sandpoint.

2 min

Idaho is not a place that’s often associated with Medieval castles, but a pair have just hit the market for $6.25 million.

The imposing stone structures have towers, turrets, ramparts, arrow-slit windows and even a drawbridge, and might just be the most authentic-looking castles this side of the Atlantic.

“Who expects to see a castle like this in Idaho?” said listing agent Brenda Burk of Coldwell Banker Schneidmiller Realty, who brought the property to the market last week. They are, she said, “extremely unusual.”

Schweitzer Castle and Château de Melusine, as they’re known, stand within Schweitzer Mountain Resort in the Selkirk Mountains and overlook the nearby mountain resort town of Sandpoint. They take in panoramic views of Lake Pend Oreille, Idaho’s largest lake.

The pair of ski-in/ski-out homes each have three bedrooms, two bathrooms and three stories, Burk explained. They are “so authentic,” she said. “Every single stone was handlaid.”

Schweitzer Castle, she said, wasn’t built for “functionality,” but has been modernized and adapted and now has everything a 21st-century residence requires, along with a dungeon, which for some buyers may also be a requisite.

The chateau, meanwhile, has a hot tub room with mountain views, as well as a garage.

The property is being sold furnished, and will come complete with the hand-carved statues, armor, mounted swords, stained-glass windows and a host of antiques dating to the 15th and 16th centuries.

The owner, an antique collector who couldn’t be reached for comment, “is always looking for that hidden jewel and he found that here,” Burk said.

The next custodian is likely to stem from a varied pool of buyers, Burk said, that would include “the trophy-home buyer, someone who can say ‘I own a castle.’”

The property could also appeal to someone looking for a vacation home, or a multi-generational estate, and beyond that “there’s the dreamers,” she said. “We definitely try to market to people who like Medieval history or maybe do Renaissance fairs.”

The seller “really wants it to go to someone with the same passion.”