How to Make Sense of New York’s Confusing Luxury Home Market

From where the big deals are happening to new condo inventory, here’s everything you need to know about what’s happening at the high end

By KATHERINE CLARKE

Thu, Mar 21, 2024 9:17am 9min

Buyers and sellers are having a hard time deciphering the New York City luxury real-estate market. Credit: Matteo Colombo/Getty Images

On Central Park South, retired entrepreneur Ron Pobuda has relisted his two-bedroom apartment for $8.95 million, a dramatic 40% reduction from its first asking price in Sept. 2020. Twenty blocks north, on the Upper East Side, real-estate agent James Morgan found a buyer for an $18 million penthouse before he could even get the property listed online.

In the wake of the Covid pandemic and interest-rate hikes—and amid an AI-driven stock market climb—buyers and sellers are having a hard time deciphering the New York City luxury real-estate market.

Ask a broker in Miami and they’ll say New York is dead. Ask a residential tower developer in New York, they’ll say that is nonsense. Ask a local real-estate agent, and he’ll say the market has rarely felt so hit-or-miss.

“It’s a mixed bag. Some things sell in two days. Other things sit there for two years,” said Leonard Steinberg, a luxury real-estate agent with Compass .

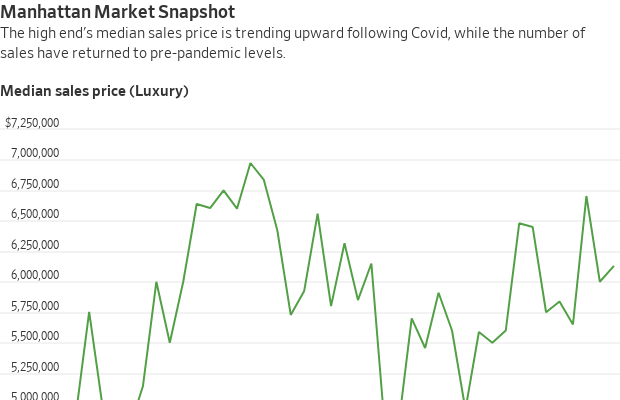

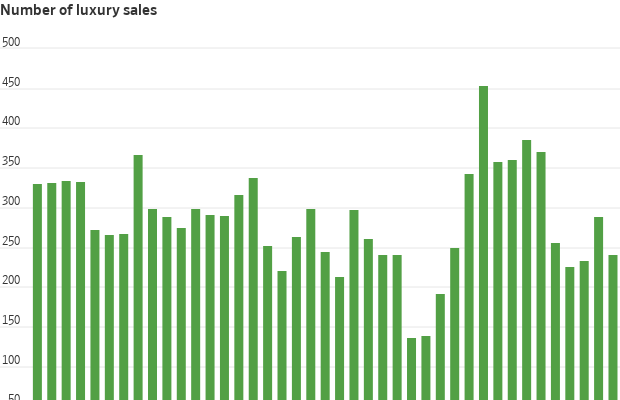

The Manhattan numbers point to a post-Covid luxury market that likely bottomed out in 2023, said appraiser Jonathan Miller . A report he prepared for brokerage Douglas Elliman shows that, in the fourth quarter of 2023, sales of luxury Manhattan homes (defined by the report as the top 10% of all sales ) were down by 5.9% compared with the same period a year prior.

It seems to be improving. So far in 2024, luxury contract activity has ticked up incrementally, according to local agents, who cite a decrease in inventory and a rising stock market. Liquidity pace, a measure of the rolling previous 30 days of signed-contract volume, was up by 9% so far in 2024 through Feb. 26 for apartments priced at $5 million and up, compared with the same period last year, according to real-estate data firm UrbanDigs.

“It looks like 2024 will be better, but it won’t be a boom,” Miller said.

Thanks to higher interest rates, all-cash deals are dominating the market, with roughly 68% of all Manhattan transactions unfinanced in the fourth quarter, according to Miller. That is up from the usual average of around 50%, Miller said.

Here’s a closer look at New York’s contrary, confusing high-end property market.

Where the sales are

The sale of a roughly 12,000-square-foot Greenwich Village mansion owned by Dexter Goei , the former chief executive of telecommunications company Altice USA , set a new price record for Downtown Manhattan. (NYC brokers define Downtown as south of 34th Street. It is more commonly defined as south of 14th Street.) It traded off market for $72.5 million in January. The price was more than double the $30.9 million that Goei paid for it in 2016, records show.

A West Village townhouse recently set a Downtown record when it sold for $72.5 million. PHOTO: MARCY AYRES/THE WALL STREET JOURNAL

The deal added to a string of major Downtown transactions that propped up the Manhattan market in 2023. In July, a penthouse at 150 Charles Street, a successful West Village condominium project, sold for $52 million . The seller was a company tied to former Credit Suisse executive Robert Shafir . In June, a Soho penthouse tied to Stefan Kaluzny, managing director of the private-equity firm Sycamore Partners, sold for $50 million , one of the largest deals ever recorded in Soho.

Clayton Orrigo, who worked on the $72.5 million Greenwich Village deal, said his team at Compass has closed or signed contracts on more than $500 million in real estate since the beginning of the year, with about 80% located south of 30th Street, and he expects the Goei property to be the first of a handful of major house sales in the neighbourhood. Other major Downtown properties that have been shopped for sale at similarly ambitious price points in recent years include financier Steve Cohen’s fortresslike, single-family mansion on Perry Street, which is said to have asked around $150 million in off-market conversations.

“I do believe that it’s a pioneer,” Orrigo said of the $72.5 million deal, declining to confirm the identity of his clients. “I don’t think it’s the last and I don’t think it will be the most expensive.”

Orrigo attributed the rise of Downtown prices to a lack of available inventory. Sought-after Downtown neighbourhoods like Greenwich Village, the West Village and Tribeca don’t see the same levels of new development as other Manhattan neighbourhoods, thanks in large part to height restrictions tied to their designations as historic districts. He said many of his moneyed clients who visit the city eventually look to buy pieds-a-terre in the area because they are unsatisfied with the hotel offerings. Airbnb listings in New York City have also all but disappeared as the city cracks down on short-term rentals .

In addition to the city’s stepped-up enforcement of short-term rental rules, many condo and co-op boards don’t allow owners to rent their properties at all, even if the rental wouldn’t be subject to the city’s short-term rental regulations. “When they realise how hard it is, they end up buying,” Orrigo said.

Orrigo said the buyer pool is made up of tech titans and “the nepo community,” meaning the children of wealthy individuals. “We’re seeing a tremendous amount of inherited wealth,” he said.

Luxury agent Sarah Williams of Societe Real Estate said she recently had a client sign a $41,000 a month, long-term rental deal when they couldn’t find a home that met their criteria in the West Village or Tribeca.

“There’s this widespread misunderstanding about New York, that it’s struggling,” she said. “New York is so sought after, it’s just that people cannot get what they want.”

One of the most successful new condos of 2023 was also located Downtown at 450 Washington Street. A rental-to-condo conversion by the Related Companies, it posted roughly $240 million in sales across 85 transactions in 2023, the developer said. Units were priced between $1 million to $15 million for studio to four-bedroom homes. Bruce A. Beal Jr., Related’s president, said the project had the “right pricing” and that buyers, the majority of whom were local, “understood the product.”

Where it’s still tough to sell

While Downtown is thriving, Midtown has been hobbled by excess inventory, remote work and a decline in foreign buyers, who have historically gravitated toward Midtown apartments, agents said.

When Pobuda, the entrepreneur with the Central Park South apartment, listed his longtime unit, a sprawling two-bedroom with a large terrace overlooking the park, in late 2020, he first asked $15 million. While ambitious, the price reflected the property’s trophy views and location, next door to 220 Central Park South , the most expensive building in the city. He got no offers.

“It was really obvious very quickly that nothing was going to happen, so I said, ‘Let’s just pull it off the market.’ ” Pobuda said.

The new asking price is a reflection of how the market has moved in response to interest rates and is strategically pegged just under $10 million to put it in a different bracket for New York’s mansion tax, said Peter McLean of the Corcoran Group, who is listing Pobuda’s unit. “We’re throwing as many incentives to the buyers as possible,” McLean said. (The tax, paid by the buyer, starts at 1% beginning with properties of $1 million or more and gradually increases to a maximum of 3.9% for properties purchased for $25 million or more.)

Pobuda’s story is typical of Midtown sellers, many of whom have had to slash prices on luxury properties to make a deal. Compass agent James Morgan said he recently lost a listing for a three-bedroom apartment at Museum Tower on West 53rd Street after the seller refused to consider reducing the $4.25 million price. Meanwhile, his high-end listings on the more inventory-constrained Upper East Side, such as the $18 million sale of a penthouse at 135 East 79th Street, are moving quickly.

“We’re still dealing with the Covid effect in Midtown,” he said. “People are working from home and they want to be in areas that are considered more neighbourhoody.”

Midtown also has the largest concentration of high-end, unsold new development units in Manhattan. Much of the unsold inventory is on the Billionaires’ Row strip south of Central Park. It sits in buildings such as Extell Development’s Central Park Tower, the 1,550-foot-tall glassy behemoth at 217 West 57th Street, which launched sales in 2018 and has roughly 77 unsold units priced at $5 million and up as of late February, according to real-estate data and analytics company MarketProof. While 53w53, the Jean Nouvel-designed tower next to the Museum of Modern Art, which has struggled to find buyers since launching in 2015, has about 65 units remaining priced at $5 million and up as of late February, as per MarketProof.

Units at both towers are routinely selling for significant discounts. A roughly 3,700-square-foot two-bedroom unit at 53w53 recently sold for $7.85 million, 32% less than its original $11.5 million asking price in 2016, records show.

Sales hobbled by rules

While the condo and townhouse markets are generally showing signs of life, agents say the city’s co-op market remains muted. Many of them blame antiquated co-op board rules that restrict a resident’s ability to sublet their units or renovate them. Some posh buildings insist on approving contractors, for instance, or fine residents if their renovations take too long, said luxury agent Donna Olshan.

Anne Hendricks Bass in 2010 PHOTO: MIMI RITZEN CRAWFORD FOR THE WALL STREET JOURNAL

The subletting rules seem particularly egregious post-Covid, said Williams, the luxury agent, since many high-net-worth individuals moved to Florida and want more flexibility to use their units as pieds-a-terre.

“They want to live in Miami, they want to live in London. They don’t want to be tied down,” she said.

Some of the city’s priciest co-ops have seen their prices reduced in recent months. A Manhattan apartment long owned by the late pharmaceutical executive Martin Howard Solomon is now asking $45 million, down from the original $55 million when it listed in 2022. The longtime Fifth Avenue home of the late oil heiress and philanthropist Anne Hendricks Bass also got a $10 million price chop to $60 million in November. Both remain on the market as of March 18.

“Even the best of these addresses are going for ridiculously low prices,” Olshan said “It’s amazing that the shareholders don’t file activist lawsuits to try to motivate their boards to change.”

A new development drought

For the past few years, the Manhattan market has suffered from a serious oversupply problem, appraiser Miller said. For now, overall inventory remains high outside of a few select neighbourhoods, but that likely won’t last. That is because filings for new luxury condos have plummeted.

Plans approved by the New York Attorney General’s office for units priced $5 million and up peaked in the mid-2010s and have dropped since 2020, according to MarketProof. In 2015, offering plans were approved for 952 units at that price point. In contrast, there were just 57 approved in 2023.

“In the years since Covid, so many things stood in the way of new inventory,” said Kael Goodman, co-founder of MarketProof. “There was supply chain, Covid shutdowns, a perception of oversupply and a high cost of capital. There was also an attention shift from New York to Miami.”

As of the close of February in Manhattan, there were close to 1,400 developer-owned units for sale at prices over $5 million, with an average asking price per square foot of $3,820, according to analytics firm MarketProof.

Outside of Midtown, neighbourhoods with significant new development inventory at that price range include West Chelsea, Lincoln Square and the Financial District. Again, that is thanks to a handful of mega projects, including Chelsea’s One High Line and Macklowe Properties’ One Wall Street.

After a slow start marred by controversy, One High Line was among the top-selling buildings of 2023. It posted 35 closings with an average price per square foot of around $3,000, according to a spokeswoman for the developer. That brought the total number of sales to around 80, she said. Formerly known as the XI, the 235-unit condo project first launched sales in 2018, but the original developer, HFZ Capital Group, faced financial distress and the project stalled. Witkoff and Access Industries took over the project in 2022 and rebranded it.

Meanwhile, industry sources say sales have been slow at One Wall Street, the former headquarters of the Irving Trust Company bank. Sales launched at the 566-unit building in September 2021 and there were still 467 units remaining as of late February, according to MarketProof. A spokeswoman for the project didn’t respond to a request for comment.

Gary Barnett of Extell Development, the firm behind Central Park Tower, said that while “inventory is gradually getting eaten up” across the city, his company is now being “very careful to pick the right projects.”

“You don’t want to be in a situation where your cost basis is so high that you have to make $6,000 or $7,000 a foot to make money,” he said.

While he has plenty of inventory remaining on Billionaires’ Row, another of the company’s projects, 50 West 66th Street, a roughly 125-unit project off Central Park on the Upper West Side, is close to 50% sold without having even formally launched sales, he said.

Barnett pointed to the project as evidence that “if you have the right product in the right location, you can still get very real and serious prices.”

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Related Stories

Property

Idaho’s Most Unusual Listing: A Pair of Medieval Castles Complete With a Dungeon and Drawbridge

By Liz Lucking 13/07/2026

Property

Moving Back Home Used to Be a Sign of Failure. Now It Shows Financial Savvy.

By REBECCA PICCIOTTO & NICHOLAS G. MILLER 06/07/2026

Property

Alfred Hitchcock’s Vandamm House Never Existed, Until They Built Their Own

The imposing stone structures, with towers, turrets and a hot tub room, lord over the landscape near the mountain resort town of Sandpoint.

By Liz Lucking

Mon, Jul 13, 2026 2min

Idaho is not a place that’s often associated with Medieval castles, but a pair have just hit the market for $6.25 million.

The imposing stone structures have towers, turrets, ramparts, arrow-slit windows and even a drawbridge, and might just be the most authentic-looking castles this side of the Atlantic.

“Who expects to see a castle like this in Idaho?” said listing agent Brenda Burk of Coldwell Banker Schneidmiller Realty, who brought the property to the market last week. They are, she said, “extremely unusual.”

Schweitzer Castle and Château de Melusine, as they’re known, stand within Schweitzer Mountain Resort in the Selkirk Mountains and overlook the nearby mountain resort town of Sandpoint. They take in panoramic views of Lake Pend Oreille, Idaho’s largest lake.

The pair of ski-in/ski-out homes each have three bedrooms, two bathrooms and three stories, Burk explained. They are “so authentic,” she said. “Every single stone was handlaid.”

Schweitzer Castle, she said, wasn’t built for “functionality,” but has been modernized and adapted and now has everything a 21st-century residence requires, along with a dungeon, which for some buyers may also be a requisite.

The chateau, meanwhile, has a hot tub room with mountain views, as well as a garage.

The property is being sold furnished, and will come complete with the hand-carved statues, armor, mounted swords, stained-glass windows and a host of antiques dating to the 15th and 16th centuries.

The owner, an antique collector who couldn’t be reached for comment, “is always looking for that hidden jewel and he found that here,” Burk said.

The next custodian is likely to stem from a varied pool of buyers, Burk said, that would include “the trophy-home buyer, someone who can say ‘I own a castle.’”

The property could also appeal to someone looking for a vacation home, or a multi-generational estate, and beyond that “there’s the dreamers,” she said. “We definitely try to market to people who like Medieval history or maybe do Renaissance fairs.”

The seller “really wants it to go to someone with the same passion.”

9 min

9 min

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.