If You’re Buying a Home Near a Nightmare Neighbour, You Might Want to Think Again

Three real-estate professionals dish on dealing with confrontational people living next door to a listing

By ROBYN A. FRIEDMAN

Thu, Mar 14, 2024 11:29am 3min

DAVE URBAN

Q: Have you ever had to deal with a nightmare neighbour while showing a home?

Arthur Greenstein, broker associate, Douglas Elliman Real Estate, Dallas

In April 2022, I showed a four-bedroom duplex unit in University Park, near Dallas, to one of my clients. From the second we arrived, I knew there was going to be a serious problem because the next-door neighbour, who lived in the other half of the Midcentury Modern house, was nosy and angry. She would barge into the unit each time I was there with my buyer, trying to find out who her neighbour would be, and she would stand outside the duplex yelling at us about how we parked our cars. She was retired and had a lot of time on her hands, and she acted like she was the mayor of the block. It was difficult because I didn’t want to be confrontational with anyone when showing a house, and she was being intrusive. After she did this a few times, I tried to convince my client not to buy the property because I’ve seen in other situations what an unpleasant neighbor can do to the value and enjoyment of a property. But he purchased it anyway because that area had limited inventory and great schools. After the closing, the problems continued. The neighbour shut off my client’s water and electricity and put a lock on the water meter. He had to call the police to get the utilities turned back on. Over the past year, things have not calmed down. My client is involved in a lawsuit now with the next-door neighbour and the previous owner for not disclosing the adverse condition of having a nightmare neighbour living next-door.

ILLUSTRATION: DAVE URBAN

Tom Stuart, associate broker, The Corcoran Group, Brooklyn, N.Y.

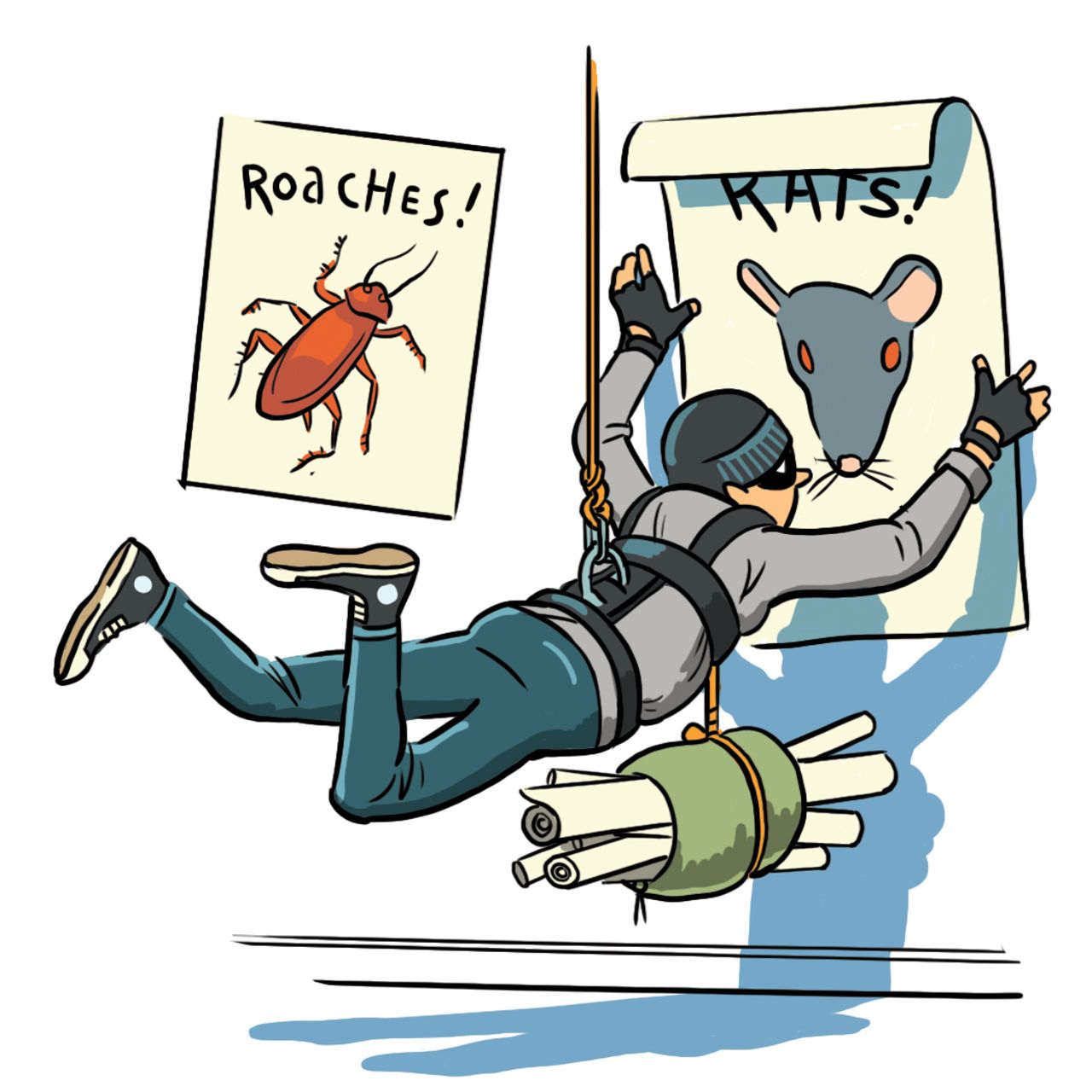

In June 2020, I listed a two-bedroom co-op in Brooklyn. This was during Covid, and the neighbour next door was very angry that buyers were coming in and out of the building. At the very first open house, when I was buzzing individual buyers into the building one by one, a buyer informed me that there was a note taped to the door of the apartment. When I went to look, I found a piece of notebook paper taped to the door that said in scrawled handwriting: “Don’t buy this! Rats and Bugs!” I had no idea how many people saw it. The neighbour also called building management and my manager to complain, but everything was being done properly. He started posting signs on the walls of the hallway that said things like “You are being watched!” and “Area under surveillance.” More than once, I caught him with his door cracked open, peeking through, which spooked potential buyers. My sellers were perplexed, but didn’t want to confront him. I was eventually able to sell the apartment, but he didn’t do himself any favours since his efforts certainly meant it took longer to sell the property and, ultimately, more people came through than might have without his interference.

Melvin A. Vieira, Jr., real-estate agent, Re/Max Destiny, Boston

In October 2019, I sold a two-bedroom, Cape Cod-style home in the Hyde Park neighbourhood of Boston. I was representing the seller. Every time I would go over to the house, the seller would yell, “Melvin, close the door, close the door!” I didn’t know what he was talking about, but then he would shout, “It’s too late. She’s there!” And then, his next-door neighbour would appear, a middle-aged woman who was nice, but quirky. She would just walk into the house and start talking about everything going on with the house and the neighbourhood. My client said she was just making it up. It got to the point where I had to sneak into the house. It became a game, almost like an episode of “Mission Impossible.” I would pull up, check for her car, and if I saw it, I would park my car down the block and then walk to the house and go in a side door just to avoid having her see me and come over to interrupt a showing. My client told me she was doing that because she didn’t want him to move. He had lived there since 1996, and she didn’t like change, so she was trying to kill the deal. My strategy was to become friendly with her and have conversations with her away from the house. If I knew someone was going to show the house, I would stop her outside her house and talk to her to distract her. The market was strong, and the house sold within a few days of being listed, so she didn’t slow anything down. And, ironically, she and the new owners get along now.

—Edited from interviews by Robyn A. Friedman

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide. LEARN MORE

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

Related Stories

Property

Idaho’s Most Unusual Listing: A Pair of Medieval Castles Complete With a Dungeon and Drawbridge

By Liz Lucking 13/07/2026

Property

Moving Back Home Used to Be a Sign of Failure. Now It Shows Financial Savvy.

By REBECCA PICCIOTTO & NICHOLAS G. MILLER 06/07/2026

Property

Alfred Hitchcock’s Vandamm House Never Existed, Until They Built Their Own

The imposing stone structures, with towers, turrets and a hot tub room, lord over the landscape near the mountain resort town of Sandpoint.

By Liz Lucking

Mon, Jul 13, 2026 2min

Idaho is not a place that’s often associated with Medieval castles, but a pair have just hit the market for $6.25 million.

The imposing stone structures have towers, turrets, ramparts, arrow-slit windows and even a drawbridge, and might just be the most authentic-looking castles this side of the Atlantic.

“Who expects to see a castle like this in Idaho?” said listing agent Brenda Burk of Coldwell Banker Schneidmiller Realty, who brought the property to the market last week. They are, she said, “extremely unusual.”

Schweitzer Castle and Château de Melusine, as they’re known, stand within Schweitzer Mountain Resort in the Selkirk Mountains and overlook the nearby mountain resort town of Sandpoint. They take in panoramic views of Lake Pend Oreille, Idaho’s largest lake.

The pair of ski-in/ski-out homes each have three bedrooms, two bathrooms and three stories, Burk explained. They are “so authentic,” she said. “Every single stone was handlaid.”

Schweitzer Castle, she said, wasn’t built for “functionality,” but has been modernized and adapted and now has everything a 21st-century residence requires, along with a dungeon, which for some buyers may also be a requisite.

The chateau, meanwhile, has a hot tub room with mountain views, as well as a garage.

The property is being sold furnished, and will come complete with the hand-carved statues, armor, mounted swords, stained-glass windows and a host of antiques dating to the 15th and 16th centuries.

The owner, an antique collector who couldn’t be reached for comment, “is always looking for that hidden jewel and he found that here,” Burk said.

The next custodian is likely to stem from a varied pool of buyers, Burk said, that would include “the trophy-home buyer, someone who can say ‘I own a castle.’”

The property could also appeal to someone looking for a vacation home, or a multi-generational estate, and beyond that “there’s the dreamers,” she said. “We definitely try to market to people who like Medieval history or maybe do Renaissance fairs.”

The seller “really wants it to go to someone with the same passion.”

3 min

3 min

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.

Copyright 2020, Dow Jones & Company, Inc. All Rights Reserved Worldwide.