Beyond the Central Region: Best Places For Expats to Live in Singapore

By Justin Huang

Fri, Oct 21, 2022 2:39pm 4 min

4 min

4 min

4 min

4 min

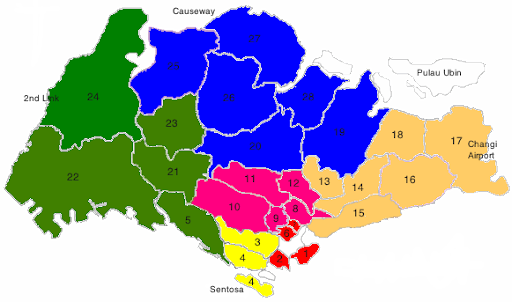

Welcome to Singapore. Known for its political stability, multicultural and multiethnic demographic, Singapore grew from a tiny fishing town into a bustling financial hub that is a magnet for talents regional and international. A growing pool of expatriates flocking into the lion city only means one thing: real estate is heating up and getting more competitive. For those that have just recently received job offers to Singapore, fret not. Here’s a rundown of the best areas for expats to reside in Singapore.

Kanebridge spoke with a rising real estate agent in Singapore, Denyse Chong for her insights on these trends in Singapore.

Not only are the properties in these areas near to the Central Business District (Raffles Place, City Hall etc), it also boasts Singapore’s famous Orchard Road Shopping Belt! Cafes, restaurants, eateries, and groceries are easily accessible when you need them, and work is only a short 20-minute commute away! Within District 9, River Valley would be my personal favourite. The Riverfront Lifestyle promises a very chill, relaxing environment that you’ll be excited to come home to after a day of work.

Expats with children will most likely bookmark this district as this is the place you’d want to be when considering education options for your adolescents. It is surrounded by elite junior institutions such as Anglo Chinese School, Raffles Girls, Nanyang Primary, to name a few. It is also home to the Singapore Botanical Gardens where you can bond with your family over picnics. It is slightly farther out than Orchard, but even then, reaching the CBD will take you no longer than 30-mins.

Tiong Bahru is known for its “quaint little vibes” with walk-up apartments, shophouses and local coffee shops. You’re also inbetween either CBD, or the Telok Blangah offices. For some weekend fun, you can easily pop by Sentosa’s beach clubs for drinks.

Depending on where and which part of those areas, it can be pretty fast-paced, especially during rush hours. More so for the dwellings along the Orchard stretch. Foot and vehicular traffic can get quite heavy at the end of the day.

Rivey Valley is a nice quiet neighbourhood. You would meet fellow expats at the cafés in the area having brunch on weekends after walking their dogs, or fellow neighbours going for a run or cycle along the Singapore River.

Queenstown and Tiong Bahru presents more of a local vibe with more public housing located in the area, compared to D09 and D10. If you’re looking to immerse yourself into local culture, this area can be very interesting too!

Depending on your budget. If it’s within your financial means, purchasing a BUC (building under construction) property/brand-new property directly from the developer will be better as there are lower risks incurred from progressive payment. You are also at lower risks amidst a hike in interest rates as your loan would be disbursed progressively and not in entirety. Alternatively, you can also consider projects that have just obtained completion, so the wait is less, and you can move in immediately.

If you’re in need of larger living spaces, I would recommend going for slightly older developments (10 years of age and above) as you would get more liveable space for the same amount of beds and bath layout. However, this is location subjective. Finding an older development may also command a higher premium than a developer’s new release due to prevailing PSF prices.

If you’re here for a short but good time, renting would be a better way as you get to explore a variety of properties during your stay here.

Barriers of entry for purchasing a property include the upfront cash on hand required amounting to 25% of property price, as well as the additional buyer stamp duties foreigners would be required to pay, above the property price, at 30%, payable in cash. This represents a huge quantum.

It should be pre-requisited on what your goals are. If you’re purchasing and intending to pass the property down to your children, I would say freehold. But if you’re intending to invest, leasehold is equally competitive. The returns on investment may even stand to be better than a freehold property too.

While I believe it used to be popular to stay within the city due to close proximities to the office, nowadays, staying within the city fringe is getting increasingly popular as well. Furthermore, City Fringe property prices are much lower than that within the Core Central Region (CCR). Our Public Transportation is reliable and cost-efficient. This allows for more expats to rent at city fringe places for bigger spaces at the same budget. (An equivalent 2-bedroom rental in the city would translate to renting a 3-bedroom in the city fringe). It is a consideration for Expats to want to “detach” from work by returning to their home slightly further away from the hustle and bustle of the city.

You may wish to contact Denyse for further assistance if you’re looking to relocate to Singapore for work.

Denyse Chong

(65) 97116664

R063810F

The Australian leather house has opened an immersive four-day pop-up in Manhattan, unveiling its Bloom Collection and redefining what a product launch can look like.

Following the successful launch of its Palais Collection, MAISON de SABRÉ has unveiled a new modular handbag system offering more than 720 styling combinations.

The imposing stone structures, with towers, turrets and a hot tub room, lord over the landscape near the mountain resort town of Sandpoint.

2 min

Idaho is not a place that’s often associated with Medieval castles, but a pair have just hit the market for $6.25 million.

The imposing stone structures have towers, turrets, ramparts, arrow-slit windows and even a drawbridge, and might just be the most authentic-looking castles this side of the Atlantic.

“Who expects to see a castle like this in Idaho?” said listing agent Brenda Burk of Coldwell Banker Schneidmiller Realty, who brought the property to the market last week. They are, she said, “extremely unusual.”

Schweitzer Castle and Château de Melusine, as they’re known, stand within Schweitzer Mountain Resort in the Selkirk Mountains and overlook the nearby mountain resort town of Sandpoint. They take in panoramic views of Lake Pend Oreille, Idaho’s largest lake.

The pair of ski-in/ski-out homes each have three bedrooms, two bathrooms and three stories, Burk explained. They are “so authentic,” she said. “Every single stone was handlaid.”

Schweitzer Castle, she said, wasn’t built for “functionality,” but has been modernized and adapted and now has everything a 21st-century residence requires, along with a dungeon, which for some buyers may also be a requisite.

The chateau, meanwhile, has a hot tub room with mountain views, as well as a garage.

The property is being sold furnished, and will come complete with the hand-carved statues, armor, mounted swords, stained-glass windows and a host of antiques dating to the 15th and 16th centuries.

The owner, an antique collector who couldn’t be reached for comment, “is always looking for that hidden jewel and he found that here,” Burk said.

The next custodian is likely to stem from a varied pool of buyers, Burk said, that would include “the trophy-home buyer, someone who can say ‘I own a castle.’”

The property could also appeal to someone looking for a vacation home, or a multi-generational estate, and beyond that “there’s the dreamers,” she said. “We definitely try to market to people who like Medieval history or maybe do Renaissance fairs.”

The seller “really wants it to go to someone with the same passion.”