China’s real-estate bust left behind tens of millions of empty housing units. Now that historic glut of unoccupied property is colliding with China’s shrinking population , leaving cities stuck with homes they might never be able to fill.

The country could have as many as 90 million empty housing units, according to a tally of economists’ estimates. Assuming three people per household, that’s enough for the entire population of Brazil.

Filling those homes would be hard enough even if China’s population were growing, but it’s not. Because of the country’s one-child policy , it is expected to fall by 204 million people over the next 30 years.

“Fundamentally, there are not enough people to fill the homes,” said Tianlei Huang, a research fellow at the Peterson Institute for International Economics.

Some unused real estate will be bought up and lived in, especially if more government support—which economists have been calling for —convinces Chinese buyers that values will rise again. Big cities like Beijing, Shanghai and Shenzhen will almost certainly absorb their excess housing, given their dynamic economies and migrant inflows, which have helped keep their populations growing.

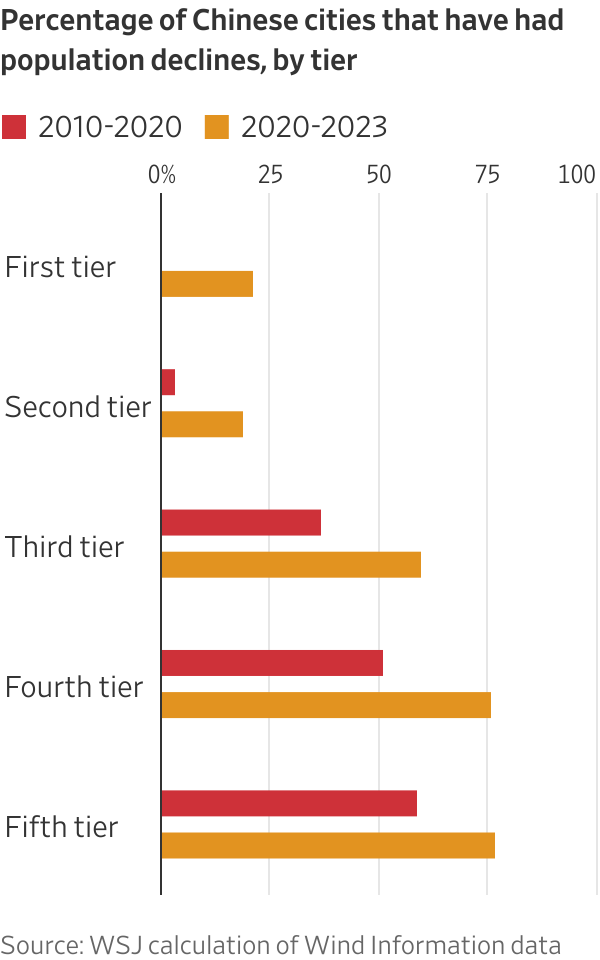

The problem is much harder to solve in smaller cities, which often have weaker economic prospects and declining populations. In China, researchers informally group cities into tiers, and many of the nearly 340 cities classified as third-, fourth- and fifth-tier—with populations from few hundred thousand to several million people—are struggling economically.

Young residents are leaving. At least 60% of China’s third-, fourth- and fifth-tier cities saw their populations shrink from 2020 to 2023, according to Wall Street Journal calculations based on official data.

Those cities have more than 60% of China’s housing inventory, according to Harvard economics professor Kenneth Rogoff . Many encouraged developers to build more—even when their populations were falling—because land sales and construction boosted economic growth and fattened local governments’ wallets.

Figuring out what to do with unneeded property is becoming more urgent as China’s economy languishes . In May, Beijing unveiled a rescue package in which the central bank would provide up to $42 billion in low-interest loans for Chinese banks to lend to state-owned firms, which would then buy empty properties and turn them into affordable housing.

By the end of June, banks had only used 4% of that quota. Economists say that even with cheap loans, it doesn’t make sense to convert empty properties, because the rents would be too low for firms to earn a profit.

Beijing recently ramped up measures to support the ailing economy and the property market, including cutting interest rates, lowering down payments for second homes and allowing home buyers to refinance their mortgages . However, economists said that more is needed to pull China’s economy out of the rut.

China’s Ministry of Housing and Urban-Rural Development and the State Council Information Office didn’t respond to questions.

Robin Xing , chief China economist at Morgan Stanley, said China’s government should introduce a more comprehensive bailout that involves buying up excess inventory in China’s 30 to 50 largest cities and turning it into public housing , without worrying about profit. Estimated cost: $420 billion.

That wouldn’t include empty homes in third-, fourth- and fifth-tier Chinese cities. Putting more money into those units, many economists say, wouldn’t make sense because there aren’t enough people to live in them anyway.

Many will become long-term burdens to cities and investors who get saddled with assets they can’t sell and which have lost their value, yet still must be maintained. Some will just wither away, economists say.

Cheap as cabbage

An abandoned development called State Guest Mansions, on the edge of Shenyang, a city in northeastern China, gives an idea of what that could look like. Construction stopped years ago, with more than 100 half-built villas in the style of grand European homes.

During a recent visit, goats roamed the complex. Grandeur Place, the building that used to house the sales showroom, looked like a post-apocalyptic opera house , with a dilapidated chandelier hanging from the ceiling. It remains unclear what will be done with the complex, whose developer has defaulted on its debt.

Shenyang at least has a growing population. In Hegang, a frigid city near China’s border with Russia, the population has declined to 940,000 from 1.09 million in 2010.

A few years ago, when Hegang’s market was hot, property enthusiasts posted online messages touting homes they said were as cheap as cabbage.

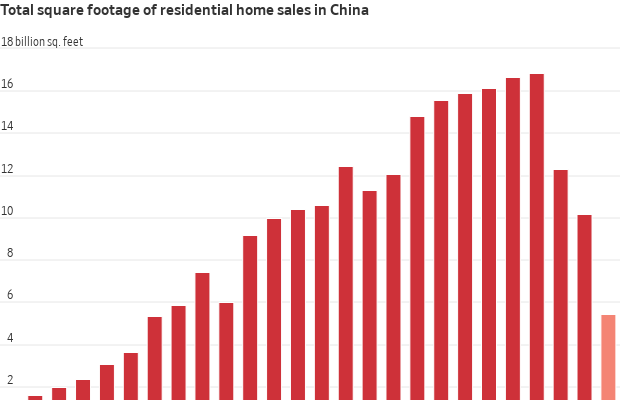

Prices now are even lower, according to an online property broker, and sales have stalled. Hegang’s inventory of unsold homes more than doubled from 2019 to 2022. Assuming a typical home size of around 1,200 square feet—the average in China in its 2020 census—only 534 residential homes in Hegang sold in 2022, according to official data on total square feet for residential real estate sold.

A 650-square-feet apartment in the city centre was recently listed for just under $9,300.

Zhou Yongzhi, a part-time stock trader who grew up there, said most high-rise apartment buildings in the city centre are dark at night. “Hegang is my hometown, and I want to see it flourish. But I don’t see much hope for it in the next 10 to 20 years,” he said.

Hegang’s government didn’t respond to requests for comment.

Rogoff, the Harvard professor, said he believes there will be some cities in China in which a quarter of the housing is empty.

In such places, “it is very hard to maintain law and order, even probably in China,” he said. “I think it’s going to be a big social and governance problem in the future.”

Complex issue

China’s property glut developed over a years long construction boom that ended in 2021, when Beijing, worried about a bubble, tightened credit for builders. It quickly became clear that developers had overbuilt .

It’s hard to determine exactly how big the problem is. China doesn’t provide an official count of empty units, so economists must devise estimates using vacancy rates, building permits and other data sources. They estimate the number is in the tens of millions—including several kinds of empty properties, each with its own challenges.

Of the up to 90 million units that are unoccupied, as many as 31 million were fully or partially built but never sold. Such properties could be bulldozed, but many are tied up in litigation related to developers’ bankruptcies. In many cases, cities and developers hope to finish them.

Another 50 to 60 million units were bought but remain empty. Many Chinese, lacking other good ways to invest their money, poured excess cash into speculative properties—often in smaller cities, where prices were cheaper—without any intention of living in them.

Approximately 74% of Chinese households in first- and second-tier cities owned more than one home across China, while nearly 20% owned three homes or more, according to a recent survey by Citi Research.

These homes are potentially more difficult to deal with because their owners still hope for appreciation. Many are in partially occupied buildings that can’t be torn down.

An additional 20 million units were sold but were left largely unbuilt by developers due to cash-flow problems and poor market conditions. The owners still want them, but developers don’t have money to finish them.

Venice on the Sea

Many builders set their sights on smaller cities when times were good. Bigger cities were getting expensive, and investors seemed willing to buy anywhere so long as prices kept climbing.

Smaller cities embraced the activity. Many issued robust population-growth forecasts, despite evidence China’s population was peaking, because it helped them secure more resources from provincial governments and justify more building projects.

In Qidong, where the Yangtze River empties into the East China Sea, local officials struggled for years to lure major investments such as factories. Selling land to developers helped them meet growth targets. Qidong’s land sales revenue more than doubled from $932 million in 2017 to $2 billion in 2021, according to data compiled by Shanghai-based Wind Information.

Developers, in turn, marketed Qidong as an ideal bedroom community for Shanghai, a two-hour drive away.

The city’s population peaked at 1.1 million in 2020 and has declined for three consecutive years. The number of local jobs has been declining since 2007.

One of the new projects, Venice on the Sea, has 40,000 units, an artificial beach and a five-star resort. Residents can enjoy faux Venetian canals and pathways dotted with Greek and Roman statues.

Xiang Dayu, a property agent there, remembers feverish demand during peak years. Some buyers openly discussed buying apartments for mistresses. Others were willing to pay without inspecting homes in person.

But most people—many from Shanghai—bought homes as investments and left them empty, Xiang says. Now, most units sit unoccupied much of the year, with occupancy rising to only around 60% during peak summer months.

Many owners are trying to sell, with dozens of units listed on auction websites or marketed on Douyin, China’s version of TikTok. In one video recently posted to Douyin, a landlord showed a property agent around a 1,030-square-foot unit, which the owner said he bought in 2016 for around $101,000 after a beach trip to Qidong with friends.

“I thought the unit had a nice view, so I bought it there and then. I never lived here, not even once, and bought it completely for investment purposes,” he said in the video. He is now trying to sell the place for around $63,100.

Venice on the Sea was built by now-bankrupt China Evergrande Group. To the north sits another massive, largely empty residential complex built by defaulted developer Country Garden . To its south is an unfinished compound developed by China Sunac Group , which also defaulted. To its west: acres of farmland.

Local government officials didn’t respond for comment.

Ghost cities

In other countries that have had overbuilt property markets, it has sometimes taken years for excess supply to be absorbed—if ever.

In Japan, a 1990s real-estate bust and a shrinking, ageing population left millions of empty homes. Tearing them down proved hard due to legal hurdles, such as when the owner can’t be located. The number of empty units grew to 9 million last year from 8.5 million in 2018, with houses littering Japan’s landscape.

In China, many owners of empty properties are likely to keep maintaining their units, since management fees in China are low and property taxes are only levied in special cases. Tough personal-bankruptcy rules in China make it hard to walk away from properties, and many want to hang on to them for a possible market rebound.

Still, some economists fear a negative spiral in which declining home prices spur more owners to try to unload empty units, depressing values for everyone.

Prices for new and existing homes in major Chinese cities fell 5.7% and 8.6% in August from a year earlier, respectively, according to National Bureau of Statistics data.

Property prices in most cities have returned to 2017 and 2018 levels, said Yi Wang, head of China real-estate research at Goldman Sachs. If prices drop to 2015 levels, many more owners might choose to sell unoccupied properties. That’s because 2015 was the beginning of the last boom, and owners who bought early won’t want to see their units’ values fall below what they paid, Wang said.

That might be inevitable, though, given China’s falling population.

“I don’t think the housing oversupply problem has a solution, really,” said Huang, of the Peterson Institute. “Fundamentally, it’s the problem of declining demographics. Ghost cities will remain ghostly.”