Michael Jordan has found a buyer for his Chicago estate after more than 12 years.

The 7-acre compound, custom built for the basketball legend in the ’90s in the area’s Highland Park suburb, first hit the market in 2012 asking $29 million. By 2015, the price on the nine-bedroom home was reduced to $14.855 million—the digits of which add up to 23, Jordan’s jersey number—and it’s remained at that price ever since.

Spanning over 32,000 square feet on Point Lane, the home reflects the larger-than-lifeness of its owner, with 19 bathrooms, five fireplaces, a regulation-sized basketball court, a massive weight room where Jordan used to train, and a built-in aquarium, according to the Wall Street Journal.

The sale was first reported by Crain’s Chicago Business.

Outside the home, there is a tennis court, a putting green and a circular infinity pool with its own island, accessible by a small bridge. There are plenty of circular touches throughout, including a round skylight above a circular eat-in kitchen, an arched wine cellar and a circular sitting room with views directly onto the basketball court.

A large lounge area that was once an indoor pool includes glass sliding walls on either side that can open up completely during Chicago’s milder months.

Other unique features include doors from the original Playboy Mansion, a three-bedroom guesthouse and the number 23 emblazoned on the front gate.

Compass agent Katherine Malkin, who is marketing the property, confirmed the pending sale to The Athletic. Malkin did not respond to a request for comment, and the buyer and price were not immediately available. Jordan could not immediately be reached for comment.

It’s unlikely to exceed the asking price. A year after the home first hit the market in 2012, Jordan decided to sell via auction, but the home failed to even meet the reserve bid of $13 million. Despite the lack of movement, Jordan has not dropped the asking price any further since 2015.

Homes in Highland Park, a wealthy suburb of Chicago can fetch upward of $5 million, but Jordan’s home has been the priciest option on the market for a long time. Fellow Chicago Bulls legend Scottie Pippen sold a nearby home in 2023 after a five-year wait. That home, which Pippen bought for $2.6 million in 2004, sold for $1.7 million two decades later, according to Realtor.com.

It seems that despite the home court advantage, this is one game that Jordan has not been able to win.

For years, global companies showcased their Chinese operations as a source of robust growth. A burgeoning middle class, a stream of people moving to cities, and the creation of new services to cater to them—along with the promise of the further opening of the world’s second-largest economy—drew companies eager to tap into the action.

Then Covid hit, isolating China from much of the world. Chinese leader Xi Jinping tightened control of the economy, and U.S.-China relations hit a nadir. After decades of rapid growth, China’s economy is stuck in a rut, with increasing concerns about what will drive the next phase of its growth.

Though Chinese officials have acknowledged the sputtering economy, they have been reluctant to take more than incremental steps to reverse the trend. Making matters worse, government crackdowns on internet companies and measures to burst the country’s property bubble left households and businesses scarred.

Lowered Expectations

Now, multinational companies are taking a hard look at their Chinese operations and tempering their outlooks. Marriott International narrowed its global revenue per available room growth rate to 3% to 4%, citing continued weakness in China and expectations that demand could weaken further in the third quarter. Paris-based Kering , home to brands Gucci and Saint Laurent, posted a 22% decline in sales in the Asia-Pacific region, excluding Japan, in the first half amid weaker demand in Greater China, which includes Hong Kong and Macau.

Pricing pressure and deflation were common themes in quarterly results. Starbucks , which helped build a coffee culture in China over the past 25 years, described it as one of its most notable international challenges as it posted a 14% decline in sales from that business. As Chinese consumers reconsidered whether to spend money on Starbucks lattes, competitors such as Luckin Coffee increased pressure on the Seattle company. Starbucks executives said in their quarterly earnings call that “unprecedented store expansion” by rivals and a price war hurt profits and caused “significant disruptions” to the operating environment.

Executive anxiety extends beyond consumer companies. Elevator maker Otis Worldwide saw new-equipment orders in China fall by double digits in the second quarter, forcing it to cut its outlook for growth out of Asia. CEO Judy Marks told analysts on a quarterly earnings call that prices in China were down roughly 10% year over year, and she doesn’t see the pricing pressure abating. The company is turning to productivity improvements and cost cutting to blunt the hit.

Add in the uncertainty created by deteriorating U.S.-China relations, and many investors are steering clear. The iShares MSCI China exchange-traded fund has lost half its value since March 2021. Recovery attempts have been short-lived. undefined undefined And now some of those concerns are creeping into the U.S. market. “A decade ago China exposure [for a global company] was a way to add revenue growth to our portfolio,” says Margaret Vitrano, co-manager of large-cap growth strategies at ClearBridge Investments in New York. Today, she notes, “we now want to manage the risk of the China exposure.”

Vitrano expects improvement in 2025, but cautions it will be slow. Uncertainty over who will win the U.S. presidential election and the prospect of higher tariffs pose additional risks for global companies.

Behind the Malaise

For now, China is inching along at roughly 5% economic growth—down from a peak of 14% in 2007 and an average of about 8% in the 10 years before the pandemic. Chinese consumers hit by job losses and continued declines in property values are rethinking spending habits. Businesses worried about policy uncertainty are reluctant to invest and hire.

The trouble goes beyond frugal consumers. Xi is changing the economy’s growth model, relying less on the infrastructure and real estate market that fueled earlier growth. That means investing aggressively in manufacturing and exports as China looks to become more self-reliant and guard against geopolitical tensions.

The shift is hurting western multinationals, with deflationary forces amid burgeoning production capacity. “We have seen the investment community mark down expectations for these companies because they will have to change tack with lower-cost products and services,” says Joseph Quinlan, head of market strategy for the chief investment office at Merrill and Bank of America Private Bank.

Another challenge for multinationals outside of China is stiffened competition as Chinese companies innovate and expand—often with the backing of the government. Local rivals are upping the ante across sectors by building on their knowledge of local consumer preferences and the ability to produce higher-quality products.

Some global multinationals are having a hard time keeping up with homegrown innovation. Auto makers including General Motors have seen sales tumble and struggled to turn profitable as Chinese car shoppers increasingly opt for electric vehicles from BYD or NIO that are similar in price to internal-combustion-engine cars from foreign auto makers.

“China’s electric-vehicle makers have by leaps and bounds surpassed the capabilities of foreign brands who have a tie to the profit pool of internal combustible engines that they don’t want to disrupt,” says Christine Phillpotts, a fund manager for Ariel Investments’ emerging markets strategies.

Chinese companies are often faster than global rivals to market with new products or tweaks. “The cycle can be half of what it is for a global multinational with subsidiaries that need to check with headquarters, do an analysis, and then refresh,” Phillpotts says.

For many companies and investors, next year remains a question mark. Ashland CEO Guillermo Novo said in an August call with analysts that the chemical company was seeing a “big change” in China, with activity slowing and competition on pricing becoming more aggressive. The company, he said, was still trying to grasp the repercussions as it has created uncertainty in its 2025 outlook.

Sticking Around

Few companies are giving up. Executives at big global consumer and retail companies show no signs of reducing investment, with most still describing China as a long-term growth market, says Dana Telsey, CEO of Telsey Advisory Group.

Starbucks executives described the long-term opportunity as “significant,” with higher growth and margin opportunities in the future as China’s population continues to move from rural to suburban areas. But they also noted that their approach is evolving and they are in the early stages of exploring strategic partnerships.

Walmart sold its stake in August in Chinese e-commerce giant JD.com for $3.6 billion after an eight-year noncompete agreement expired. Analysts expect it to pump the money into its own Sam’s Club and Walmart China operation, which have benefited from the trend toward trading down in China.

“The story isn’t over for the global companies,” Phillpotts says. “It just means the effort and investment will be greater to compete.”

Corrections & Amplifications

Joseph Quinlan is head of market strategy for the chief investment office at Merrill and Bank of America Private Bank. An earlier version of this article incorrectly used his old title.

Boeing stock has fallen to its lowest level since 2022 after a downgrade from a Wall Street analyst put a number on one of investors’ worst fears: stock dilution.

Wells Fargo analyst Matthew Akers on Tuesday downgraded Boeing stock to the equivalent of Sell from Hold. His price target was reduced to $119 a share from $185.

That is the lowest target price on Wall Street by almost $70 a share, according to FactSet. At $119 a share, down about 30% from recent levels, Boeing would have a market value of roughly $73 billion, levels not seen since early 2020 during the Covid-19 pandemic.

Boeing stock closed down 7.3% at $161.02, while the S&P 500 and Dow Jones Industrial Average were off 2.1% and 1.5%, respectively. It was the lowest close since Nov. 4, 2022, when it finished at $160.01, according to Dow Jones Market Data.

“We think Boeing had a generational free cash flow opportunity this decade, driven by ramping production on mature aircraft and low investment need,” wrote Akers. “But after extensive delays and added cost, we now see growing production cash flow running into a undefined new aircraft investment cycle, capping free cash flow a few years out.”

At this point in its product cycle, Boeing simply should be generating north of $10 billion in free cash flow a year. However, production and quality problems have pushed output lower and added costs. Wall Street sees Boeing using almost $8 billion in cash to fund operations in 2024.

What is more, Boeing likely will need to design a new single-aisle jet in the coming years to better compete with the Airbus A321 family of aircraft. That will take tens of billions of dollars spread out over several years.

Akers sees $30 billion in equity being raised by 2026 to help cover the cost of new investment. Some of that hefty total will go toward repairing Boeing’s balance sheet. The company ended the second quarter with more than $53 billion in long-term debt, up from less than $11 billion at the end of 2018, before the pandemic and significant problems with Boeing’s 737 MAX jet.

Raising $30 billion of equity at recent prices would require issuing roughly 190 million new shares, increasing the share count by about 31%. All things being equal, a higher share count reduces earnings per share.

“If Boeing were to postpone new plane development for several more years (launch early next decade) and instead just pay down debt, we estimate free cash flow per share could grow to about ~$20 late this decade,” added Akers. That might justify a $150 share price in coming years, but postponing a new plane would mean “ ceding significant narrowbody share” to Airbus.

Narrowbody is industry jargon for single-aisle aircraft such as the 737 MAX or A320.

Raising equity and offering customers a new plane, or not offering a new jet and holding off on raising equity: Boeing doesn’t have easy choices to make in coming years.

Overall, 60% of analysts covering Boeing stock rate shares at Buy, according to FactSet. The average Buy-rating ratio for stocks in the S&P 500 is about 55%. Even though Boeing’s Buy-rating ratio is above average, it has been sliding. Coming into the year, before an emergency- door plug blew out in midair on an Alaska Air flight on Jan. 5, the ratio was north of 75%.

The average analyst price target for Boeing shares is about $214.

There are lots of embarrassing ways to lose money, but it is particularly galling to lose when you correctly identify the theme that will dominate the market and manage to buy into it at a good moment.

Pity the investors in the three artificial-intelligence-themed exchange-traded funds that managed to lose money this year. Every other AI-flavored ETF I can find has trailed both the S&P 500 and MSCI World. That is before the AI theme itself was seriously questioned last week, when investor doubts about the price of leading AI stocks Nvidia and Super Micro Computer became obvious.

The AI fund disaster should be a cautionary tale for buyers of thematic ETFs, which now cover virtually anything you can think of, including Californian carbon permits (down 15% this year), Chinese cloud computing (down 21%) and pet care (up 10%). Put simply: You probably won’t get what you want, you’ll likely buy at the wrong time and it will be hard to hold for the long term.

Ironically enough, Nvidia’s success has made it harder for some of the AI funds to beat the wider market. Part of the point of using a fund is to diversify, so many funds weight their holdings equally or cap the maximum size of any one stock. With Nvidia making up more than 6% of the S&P 500, that led some AI funds to have less exposure to the biggest AI stock than you would get in a broad index fund.

This problem hit the three losers of the year. First Trust’s $457 million AI-and-robotics fund has only 0.8% in Nvidia, a bit over half what it holds in cybersecurity firm BlackBerry .

WisdomTree ’s $213 million AI-and-innovation fund holds the same amount of each stock, giving it only 3% in Nvidia.

BlackRock ’s $610 million iShares Future AI & Tech fund was also equal weighted until three weeks ago, when it altered its purpose from being a robotics-and-AI fund, changed ticker and switched to a market-value-based index that gives it a larger exposure to Nvidia.

The result has been a 20-percentage-point gap between the best and worst AI ETFs this year. There is a more than 60-point gap since the launch of ChatGPT in November 2022 lit a rocket under AI stocks—although the ETFs are at least all up since then.

The market has penalized being equal weighted recently, instead rewarding big holdings in the largest stocks.

Jay Jacobs , U.S. head of thematic and active ETFs at BlackRock, says it is best to be market-value weighted when a theme has winner-takes-all characteristics, which he says generative AI has. When the firm’s AI fund included robotics it was spread across a lot more stocks that didn’t compete with each other, so equal weighted made more sense.

For investors, it isn’t so simple. Global X takes the opposite approach with its two $2 billion-plus AI funds, AIQ and BOTZ. BOTZ only buys stocks that focus on AI and robotics, but takes larger positions. AIQ spreads its bets on AI and tech more widely, and its 3% cap on its biggest holdings each time it rebalances means it has far less in Nvidia than BOTZ, with a cap of 8%. AIQ still managed to beat BOTZ this year, though.

So far, so confusing. The basic lesson: Picking among funds within a theme is hard, and depends on luck as well as close reading of the fund’s documents. A more advanced lesson is that it is hard to pick a theme in the first place, or to stick with it. The three problems:

1. Defining the theme is hard . Nvidia features in the anti-woke YALL ETF, which pitches itself as for “God-fearing, flag-waving conservatives.” The chip maker is also held by vegan, gender-diverse and climate-action ETFs. Its shares are clearly driven by the prospects for AI, but it is still big in computer-game and bitcoin ETFs, where its chips were originally used.

2. Timing the theme is even harder. Get in too early, and there aren’t any companies to buy. Get in when the funds are being launched, and the chances are the theme is already widely known and overpriced, as there are typically large numbers of launches during bubbles and late-stage bull markets.

“They are trendy by design,” says Kenneth Lamont, a senior researcher at Morningstar. “They play to our worst instincts, because we’re narrative-driven creatures.”

A recent example was the race to launch clean-energy and early-stage-tech ETFs during the bubble of late 2020 and early 2021. Performance since then has been miserable as prices corrected, with many of the ETFs halving or worse.

Dire timing is common across themes: According to a paper last year by Prof. Itzhak Ben-David of Ohio State University and three fellow academics, what they call “specialized” ETFs lose 6% a year on average over their first five years due to poor launch timing.

3. Long-term investing is pitched by fund managers as the goal for thematic investing, to hang on until the theme bears fruit. But even investors who really want to commit to a theme for the long run often find it hard, as so many funds are wound up, merged or change strategy when they go out of fashion.

The boom in internet funds of the late 1990s vanished after the dot-com bubble burst, with few surviving to see the internet theme blossom a decade later, while six of the 50 “metaverse” funds launched after Facebook switched to Meta Platforms in 2021 have already shut, according to Lamont.

The oldest thematic fund, the DWS Science and Technology mutual fund, started as the Television Fund in 1948 before adding electronics, and has gone through at least four other names. I only have data back to 1973, but it has lagged far behind the wider market since then, despite golden ages for television, electronics, science and now tech. (Yes, it has a lot of Nvidia.)

So what to do? At a very minimum, don’t buy based on the name of a fund. Look at the holdings, look at the index it follows and how it is structured, and consider whether it does what it says. Then think about just how expensive the idea has already become. Watch for the theme coming into fashion and getting overpriced, as that is a good time to sell (or to launch a fund).

But mostly, look at the fees: They will be many times higher than a broad market index fund, and the dismal history of poor timing suggests that for most people they aren’t worth paying.

Zero-carbon technologies comprised more than 40% of global electricity generation for the first time in 2023, according to a report released Tuesday from BloombergNEF.

Renewable energy sources like wind and solar made up 17% of total electricity generation, and hydroelectric and nuclear power contributed 24%. Fossil fuels including coal and natural gas produced 57% of global electricity last year.

“We’ve consistently seen the penetration of renewables rising every year, and this year we hit quite a few milestones that had felt harder to reach in past years,” said Meredith Annex, head of clean power at BNEF.

One such milestone: Solar and wind represented more than 90% of global energy capacity additions last year, a step up from 2022. Global wind capacity also crossed the one-terawatt threshold. And Brazil, the country with the cleanest power mix of the G-20 economies, hit 88% renewable power generation in 2023.

“It just shows the momentum that the space is having. A lot of that does tie into the investment story, where you’ve got rising—skyrocketing, honestly—investment into solar,” Annex said.

Mainland China accounted for almost a third of total renewable energy output last year. The country recently reached its 2030 target for wind and solar energy six years early, according to a statement from its National Energy Administration, and it has pulled back on permits for new coal-fired power plants. The country’s rapid deployment of renewables has some analysts wondering if it will reach peak fossil fuel consumption this year. Declining emissions in China would signal a turning point because it is the world’s largest polluter, comprising nearly a third of global greenhouse gas emissions, according to the International Energy Agency.

Despite rapid growth in renewables, countries’ current commitments aren’t sufficient to limit global warming to 1.5 degrees Celsius, the goal outlined in the 2015 Paris Agreement, according to the IEA. Advanced economies would need to slash emissions by 80% by 2035 to meet the goal.

At last December’s COP28, a global climate conference hosted by the United Nations, participating countries agreed to triple renewable energy capacity by 2030. BNEF has forecast that achieving this goal would require investments in renewables to increase to 1.6 times 2023 levels from 2024 to 2030.

So far, that increase hasn’t materialised. Global investments in renewables are roughly on par with 2023 levels, at $313 billion in the first half of 2024, according to the new BNEF analysis. “We’re expecting steady growth, but steady growth does not get you to net zero,” Annex said.

The topline numbers obscure bigger changes under the surface. Average spending in the U.S. is up by about 63% compared with levels before the 2022 Inflation Reduction Act, which offers generous subsidies and tax breaks to promote decarbonisation. And while Chinese investment is actually down 4% from the same period in 2023, Annex said the dip is due to cheaper equipment for wind and solar, not a decline in demand.

The second half of this year will be a “defining moment,” for the investment landscape, Annex said. Steady growth “is definitely a positive, and it could be a sign that the industry as a whole is reaching a new kind of status quo, but we need to help expand even faster if we’re going to be in line with net zero.”

Bosses are quietly trying to reset worker pay levels, saying the era of overpaying for talent is over.

Pay for many white-collar recruits shrank last year , and now wages for new hires in construction, manufacturing, food and other blue-collar sectors appear to be ebbing too, according to an analysis of millions of jobs posted on ZipRecruiter.com .

Job seekers report seeing roles that once offered salaries between $175,000 and $200,000 a year ago now being advertised for tens of thousands of dollars less, a change that has had them rethinking their pay expectations. Companies are also moving job openings to lower-cost cities or offering them as lower-paying contractor roles, recruiters and corporate advisers say.

The push to reset employee salaries reflects a power shift in the cooling hiring market. Employers have more choice of who they can hire, and at what pay level, and are questioning whether they really need star hires when a workhorse will do . Even hourly jobs that were until recently the toughest for employers to fill are being advertised at lower pay than a year ago, as are some professional roles, according to business leaders and recruiters. undefined undefined “A lot of companies are thinking they can get away with paying a cheaper salary because they know us job seekers are desperate,” said Eric Joondeph, 31 years old, who has been looking for a senior customer-experience role for nine months. He has lowered his pay expectations by at least $20,000 a year since he started looking.

Among listings for more than 20,000 different job titles on ZipRecruiter.com this year, sectors including retail, agriculture, transportation and warehousing, manufacturing, and food all registered drops in average posted pay. The biggest was retail, where average wages advertised for new hires is down 55.9%; agriculture is down 24.5% and manufacturing, down 17.3%.

Tom Locke, a McDonald’s franchisee who owns 56 restaurants in Ohio, Pennsylvania and West Virginia, starts hourly workers at $13 an hour, but the signing bonuses and other hiring incentives he offered during the pandemic are gone. He said he is constantly asking his managers if they can reduce hourly wages to $12 an hour.

Labor expenses at Locke’s McDonald’s locations now exceed his food costs—something he said hasn’t happened in his 24 years with the company.

“I want everybody to do well in America, but there’s cost pressures,” he said. “It’s just a constant battle.”

‘Geographic arbitrage is real’

Pay resets continue to ripple through the white-collar world too. Joondeph has been looking for a senior role in customer experience since he was laid off from a customer-experience associate role.

“I’ve seen salaries slowly dropping little by little for roles I’ve been targeting,” he said.

Based in Boise, Idaho, Joondeph said he is struck by the number of jobs he has applied for that now advertise salaries not much higher than $60,000. Many used to advertise with a range between $80,000 and $100,000 in the past six to nine months, he added.

In some cases, companies are looking to attract less experienced, but still coachable, people who can be paid less than industry veterans, corporate advisers say.

Brooke Weddle, a senior partner at McKinsey & Co., said one client recently decided to stop recruiting stars, putting in place a “no more unicorns” hiring strategy, in part, to lower costs. (Unicorns are top performers with specialised skills who can command outsize salaries.)

Other businesses are considering moving jobs overseas, said Weddle, a leader in McKinsey’s group that advises on personnel issues. Instead of hiring data analysts in the U.S., for example, companies want to add people in Mexico and cheaper parts of Europe, like Poland, to save on labor costs.

“Geographic arbitrage is real,” she said.

In the U.S., some Fortune 1000 companies are moving enterprise software jobs from expensive cities such as Chicago and San Francisco to places with a lower cost of living, such as Cincinnati and St. Louis, Mo., said Keith Sims, president of Integrity Resource Management, a recruiting firm based in the Indianapolis area.

Sims, who for 25 years has helped companies recruit professionals who work with software systems like SAP and Oracle , said he hasn’t seen bosses so intent on reining in pay since the recession of 2009.

Salaries for tech jobs working with back-office and core operations business software that paid between $110,000 and $130,000 a year ago now go to less experienced hires for $85,000 to $100,000, he said. Some companies are laying off entire service areas, renaming the division and populating it with new hires at much lower compensation levels.

Hiring managers gain leverage

Overall pay for new hires in white-collar sectors increased this year, after falling in 2023, buoyed by gains in certain corners of the professional world, including law, engineering and healthcare, according to Julia Pollak , ZipRecruiter’s chief economist.

Although some tech roles that require artificial intelligence skills still offer hefty pay, many other tech jobs are advertised at lower salaries than two years ago, according to some Silicon Valley recruiters.

“Most people we interview are seeing lower salaries,” said Jill Hernstat, chief executive of Hernstat & Co., a tech recruiting firm based in the San Francisco Bay Area. “Hiring managers know they are more in control now.”

Other white-collar professions with declining new-hire salaries include finance, down 9.2% in the past year, other professional services, down 2.4% and insurance, down 1.6%, according to Gusto, a payroll and benefits software company with more than 300,000 small and midsize businesses as customers.

Pay adjustments are easing some tensions among colleagues who may have resented how much new hires were making, and the fact that tenured employees’ pay hadn’t kept up, said Tom McMullen , a senior client partner at Korn Ferry , a global organizational consulting firm.

“A lot of leaders wanted this market to cool down because they got themselves into some internal equity messes by paying through the nose for all this hot talent,” he said. “What we’re hearing is, ‘Hey, I don’t have to offer the exorbitant in-hire rates that I was offering.’”

Same work, less pay

Kate Ball was at Amazon .com for eight years, some of them as a senior recruiter, before being laid off in 2023. External recruiters have since repeatedly called her about a contract role there as a senior recruiter. Ball said the job is virtually the same as the one she had once held, but for up to 65% less pay.

Some of her former co-workers who were also laid off have taken lower-paid contract positions with Amazon: “I don’t know anyone that came back on the same package,” said Ball, 44, who has started her own HR advisory practice, Sparkle & Sass Consulting.

As Ball has applied for roles elsewhere, she has noticed some openings get reposted with lower pay ranges than were advertised weeks or months before. She applied for one job, as an employee-experience manager, went through two interview rounds, then heard nothing. A few weeks later, she saw the same job re-advertised, this time at roughly a third less than the six-figure salary she’d been quoted by the recruiter.

It is understandable, Ball said, that companies are reining in pay when they have a greater pick of job candidates than they did a couple of years ago. Still, some tactics could create ill will for employers when they have to compete more intensely for talent again.

“People will take a job now because it pays them and they’re scared, but that’s not going to last forever,” she said.

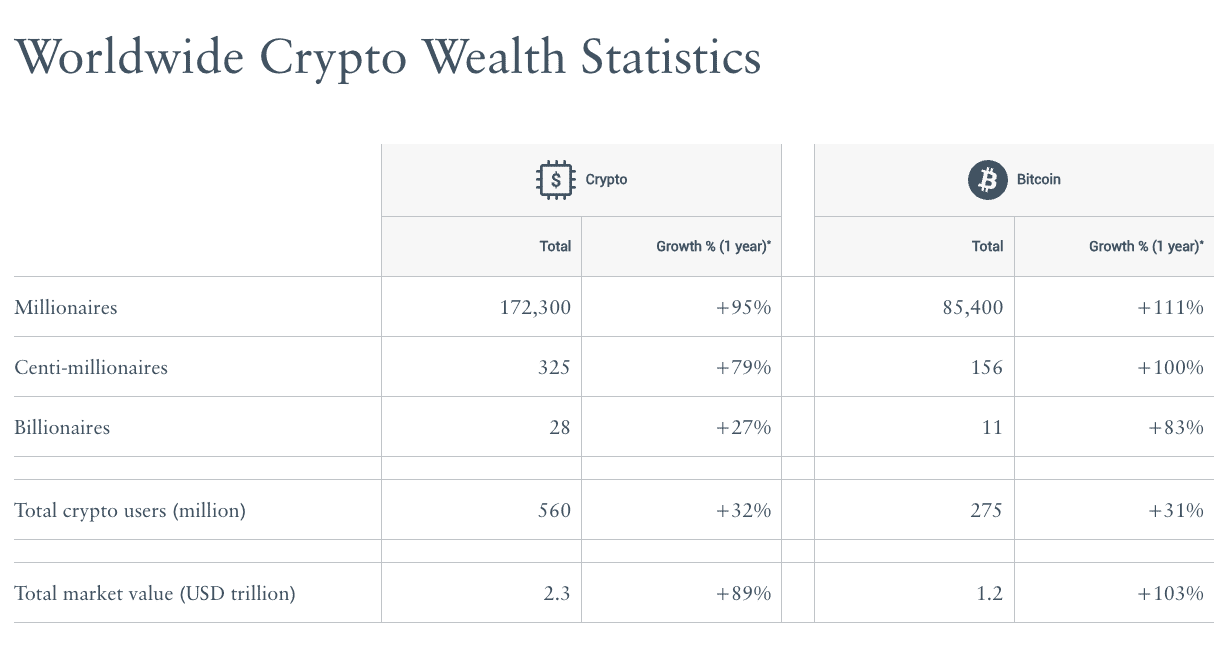

The number of crypto millionaires has doubled in the last year, as key regulatory approvals and a new Bitcoin high led to a rapid increase in crypto adoption and a new “crypto elite,” according to a report by wealth and migration consultancy Henley & Partners.

Crypto adoption increased 31% in the 12 months ending in June, to a total of 560 million users globally, while the total market value of crypto holdings nearly doubled to US$2.3 trillion as of June 30. Bitcoin, which peaked in March at US$73,000, comprised about half of both users and value, with 275 million investors and a US$1.2 trillion total market value, up 103% from the previous year, the report said.

The surge in both price and adoption of cryptocurrencies has minted a new crop of millionaires.

In fact, the number of crypto millionaires just about doubled to 172,300 in the last 12 months, and the number of Bitcoin millionaires more than doubled to 85,400—or roughly half of the overall total.

There are also now 325 crypto centi-millionaires—individuals with crypto holdings of at least US$100 million—up from 181 last year, with Bitcoin investors, once again, comprising about half of the total.

Crypto currencies have also minted 28 billionaires, a list that includes the Winklevoss twins—Brett and Cameron Winklevoss;SecondMarket founder Barry Silbert ; MicroStrategy co-founder Michael Saylor ; and Binance founder Changpeng Zhao , who is currently serving a four-month prison sentence after being found guilty of money laundering by a California court earlier this year, according to MarketWatch.

The increase has largely been driven by regulatory shifts that have allowed for the normalisation of cryptocurrencies, despite the high-profile implosion of key crypto players like FTX and Genesis Global Capital in 2022 and 2023. In particular, the U.S.’s’ approval of spot crypto exchange-traded funds in January (following its approval of crypto futures ETFs) signalled a new era of institutionalisation.

“The long-awaited approval of spot Bitcoin and Ethereum ETFs in the USA unleashed a torrent of institutional capital,” Dominic Volek of Henley & Partners said in the report.

The U.S. ranked fourth in Henley & Partners’ analysis of global crypto hubs, which takes into account regulation, infrastructure adoption, technology prowess, and tax-friendliness, among other factors. Singapore leads the list due to its recent implementation of a regulatory framework for crypto assets, as well as its strength in infrastructure, technology, and economic indicators. Hong Kong, which also approved spot crypto ETFs in January, came second, followed by the United Arab Emirates, which scored highest on tax-friendliness.

Competition between global economic hubs is crucial, because the rise of the crypto elite is driving wealth migration patterns, Henley & Partners said.

“As we move forward, the intersection of cryptocurrency and investment migration will undoubtedly play a major role in shaping the future of global wealth and mobility,” Volek said.

WALK INTO any Kate Spade or Frances Valentine store today, and you’d be forgiven for thinking the retailers are uncomplicatedly preppy—the kind of place where your mother might find an innocuous floral shift or clutch for a luncheon. But Katherine Noel Valentine Brosnahan Spade, the woman who co-founded those brands, was no Lilly Pulitzer during her outsize life, which was cut short by suicide in 2018.

With her partner, Andy Spade, she started Kate Spade with six boxy handbags in 1993. They weren’t married yet; she was the “Kate” and he was the “Spade.” The former fashion editor at Mademoiselle magazine and the brilliant adman made a dashing couple straight out of a Wes Anderson film: she with her chignons, heels and big jewellery, he with his Brooks Brothers—with-a-twist button-downs and jeans. They lived in pre-billionaire Tribeca; they drank martinis; everyone wanted in. Kate and Andy dreamed of a company they hoped would bridge the gap between L.L. Bean and Prada.

“We were just kids,” says Andy today from his new home in the San Francisco Bay Area. “We wanted to control our destiny so we just started a handbag company with no experience whatsoever.”

And boy, did they succeed. The household-name American brand would go on to include stationery, books, clothing, home goods, jewellery, shoes, the men’s line Jack Spade and licensing deals worldwide. Kate Spade’s nylon bags were coming-of-age talismans for girls and women at the turn of the 21st century, spawning oodles of Canal Street knockoffs. When Kate died, Vogue ’s Anna Wintour said, “There was a moment when you couldn’t walk a block in New York without seeing one of her bags, which were just like her; colourful and unpretentious.”

Yet despite the TikTok generation’s thirst for everything Y2K—from Fendi baguette bags to Juicy Couture tracksuits—Kate Spade’s brand heat under current owner Tapestry is lukewarm.

“Gen Zers and TikTok consumers are constantly looking to the ’90s and early aughts for trends,” says Casey Lewis, a consultant who writes “After School,” a youth-culture newsletter. “And so this seems like it would be prime time for a Kate Spade comeback.”

Some interest is bubbling up: Kate Spade recently reissued one small ’90s baguette bag with Urban Outfitters. Last year, it relaunched its original “Sam” bag. And prescient trendsetters are dusting off their vintage Kate Spade pieces. Yet a recent collaboration with Heinz ketchup left some consumers and analysts scratching their heads. Tapestry, which declined to comment, reported a 6% decrease in Kate Spade sales for the nine-month period ending in March 2024 compared with the previous year.

The challenge of evolving Kate’s aesthetic without her began while she was still alive, when the company she co-founded with Andy, Pamela Bell and Elyce Arons was sold to Neiman Marcus Group in 2006. The group, which had already bought 56 percent of the company in 1999, in turn sold it to Liz Claiborne. Coach, which is now Tapestry, acquired the brand in 2017 for $2.4 billion.

NEW YORK 2023: Kate Spade knit green top and cardigan, Kate Spade red long skirt with pink polka dot pattern, Kate Spate green leather bag and green leather mules. (Photo by Jeremy Moeller/Getty Images)

The enigma lies in decoding a fashion icon who was always more complex than polka dots or pink and green. Under Kate and Andy, the brand’s American joie de vivre was tempered with intellectual, offbeat references: architect Buckminster Fuller, Eames furniture, Rei Kawakubo. And along with joy and eclecticism, there was darkness. Her death at age 55 left behind a grieving husband, a 13-year-old daughter, Frances Valentine Beatrix Spade—and a towering style legacy that is often misunderstood.

After a company changes hands multiple times, and its founder dies, can its original vision endure?

“THE INTERPRETATION of [Kate’s] legacy is a little different from how she actually was,” says her co-founder Bell. “Because she was petite and so adorable, everyone associates her with the words cute or happy, and she was much more complicated and sophisticated than that.”

Andy, Kate, Bell and Arons all came from the Midwest. Their partnership coalesced at a summer share house in tony Amagansett, New York. Kate (friends called her Katy) was one of six kids from Kansas City, Missouri; Andy, the brother of comedian David Spade, was born in Birmingham, Michigan, and raised in Arizona. Kate and Andy both went to Arizona State University and met while working at the same Phoenix clothing store. Andy’s car broke down one day, and Kate offered him a ride.

“Katy was more subversive than anyone knew,” says Andy. “They just pigeonholed her as the girl next door. But she was a girl next door and a girl across the street, down the alley and across the hall.”

Kate wore avant-garde Japanese designs from Comme des Garçons and Sacai and hippie slips from Dosa. She loved dining on steaks at Raoul’s and Lucky Strike in SoHo, and hanging out with artists and weirdos. She played Bob Dylan loudly and read books by John Knowles and W. Somerset Maugham. She scoured Indian import stores in the East Village for brightly coloured silk tunics to wear with cigarette pants, pairing them with wild costume jewellery she’d picked up at the wholesalers on Sixth Avenue.

She and Andy also appreciated simplicity. As a design inspiration, the two often cited advice from The Elements of Style, Strunk and White’s manual for writers—“To achieve style, begin by affecting none.”

Kate’s niece Whitney Pozgay, a designer who worked at Kate Spade for years, describes the company culture as freewheeling and fun, with beer carts on Fridays and Phoenix and Björk on the sound system. She says Kate was bubbly and effervescent, coming down to the studio with her little dog Henry to tease, “Working hard or hardly working?”

In the early days, Kate and Andy gave each new employee a copy of Emily Post’s Etiquette. But in 2004, to put her own spin on propriety, Kate published three volumes: Manners, Style and Occasions. The advice offered was more madcap than proper: Admire the polka dots on a Wonder Bread package! Play “Electric Version” by the New Pornographers to start a party! Gift your beloved an Etch A Sketch for your iron wedding anniversary!

Writer Jill Kargman, who was Kate’s intern at Mademoiselle and stayed close with her, says the designer was a master of the written note, pairing formality with casualness and “sparkling chutzpah.” Whether in her correspondence or her style, she says, Kate had “total edge,” musing, “To think outside the box, you have to know what the box is. It’s like she studied the box, but then she flipped it a little bit and gave it a blood transfusion.”

The Spades were funny. When Kate and Andy hosted their first adult dinner party, the invitation went out with a copy of instructions for the Heimlich manoeuvre. While the brand was built on highlighting all the things Kate liked, she told Index magazine in 1998 that her customers were free to say: Who the hell cares what Kate Spade likes? (Andy says that David Spade always considered Kate to be funnier than all his comedian friends, including the late Chris Farley.)

Even the company’s signature—a small, humble black clothing label in the place of a logo—came from a place of irreverence: Kate thought the bag needed a little something, so right before the launch she put the inside label on the outside. For its first order, Barneys New York requested that the label be put back inside. But, Bell says, “Of course, after they became popular, they wanted them on the outside.”

As the brand took off, so did the couple’s social life. Although Andy, more than Kate, became a collector of bohemian downtown characters, she was always game. Gabi Asfour, co-founder of the artistic collective As Four, who once worked for the couple as a clothing designer, remembers staying up late drinking with the Spades at the Hôtel de Crillon during a trip to Paris. “What I loved is the clash of the roughness of downtown mixing with the cleanness of uptown,” he says.

That creative clash came through in the brand’s advertising, as masterminded by Andy alongside Julia Leach, now chief creative officer at Athleta. Andy commissioned filmmakers like Mike Mills and the Safdie brothers to direct shorts for the brand. The print ads, such as those photographed by artists Larry Sultan and Tim Walker, rarely did the basic job of displaying the handbags. The goal was something else entirely: to evoke feelings.

One campaign, shot by art-world chronicler Jessica Craig-Martin, was produced as an actual party at The Explorers Club in Manhattan, with Kate and Andy hosting. “The party was very real, totally madcap, and had been set up to elegantly fall apart in just the photogenic way I desired,” remembers Craig-Martin.

Another, by artist Tierney Gearon, depicted a day in the life of an elegant New England family: loading up the car, playing hide-and-seek, getting ready in the bathroom. Gearon says that although the pictures depicted a “perfect family,” she now finds them a little eerie.

Some collaborators have suggested that with these ads Andy was chasing a vision of perfection that is hard to achieve in real life. Today he says, “It definitely reflected how we felt as people.”

“It wasn’t trying to paint the picture-perfect version of white picket fences,” says Leach, who wrote scripts for these ads. She and Andy were thinking about John Updike’s and John Cheever’s stories about the beautiful flaws of American life.

KATE AND ANDY’S lightning in a bottle was all about giving glamour an off-kilter spin. Yes, an ad showing a kid seated on a toilet was weird, but it was playful—and just pretty enough. As Craig-Martin says, “The brilliance lay in the understanding of how the esoteric or sophisticated could be used to appeal to the mass market.”

Striking that balance without Kate and Andy’s input is tricky, and gets harder as the years go by.

“They get the ingredients, but not the recipe,” says Pozgay when discussing how her aunt’s style legacy is often interpreted. Yes, she loved pink, but it had to be the right pink, and perhaps shot through with a dark poppy-red stripe.

After selling the brand in 2006, Kate and Andy Spade agreed to stay on for six months to help with the transition. In the intervening years, the company has grown incrementally but lost some of its cultural cachet. This year, the Federal Trade Commission sued to block Tapestry’s $8.5 billion acquisition of Capri Holdings, which owns Michael Kors and Versace. In the meantime, Tapestry must prove its mettle with the heritage brands it already owns.

As for Frances Valentine, where Kate was working alongside her old friend and Kate Spade co-founder Arons when she died, the brand is owned by Andy, Arons and other investors, including venture-capital fund Sweater. The company reports 200 percent growth in its wholesale business from 2023 to 2024, and will launch at Dillard’s this fall. A recent visit to its small, quiet Sag Harbor, New York, store (one of nine) revealed preppy, retro classics like beaded sandals and beachy caftans. Arons is working on a forthcoming book about her friendship with Kate.

In the weeks following Kate’s death, sales surged at both Kate Spade and Frances Valentine. When a fashion designer or an artist dies, scarcity fuels demand—Alexander McQueen’s suicide in 2010 inspired a similar frenzy. It’s what happens after that bump that determines a brand’s longevity.

“How do you do justice to the spirit of the thing, but bring it to more people?” asks the chief creative officer of luxury resale retailer TheRealReal, Kristen Naiman, who worked at Kate Spade from 2014 to 2023. “That’s the name of the game when you scale something as special as what Kate and Andy made.”

While they were running the company, Andy would quote advertising executive Jay Chiat, who asked: How big can we get before we get bad? Today, he is at peace with how they handled the sale, which he equates with getting your teen child into college and then backing off.

“There are roots in that brand—Kate Spade—that are about values and people, and that’s what I wanted to do,” Andy says. “Build roots for the brand to exist forever. And I never looked back.”

During Kate and Andy’s time at Kate Spade, the company didn’t resort to one of the fashion industry’s lesser publicized strategies for growth: making products specifically targeted for outlet stores. Today, there is an extensive outlet network, including a newly launched dedicated e-commerce site. Kate Spade pajamas produced under a license were recently sold at Costco for less than $20.

“I think they have a lot of potential,” says Casey Lewis, the youth-culture consultant. “I would be shocked if they did not successfully make a comeback in the coming years, because the brand isn’t so watered down or so irrelevant that no one knows it at this point. They can just reclaim the cool.”

HANDBAGS ASIDE, Kate’s legacy also includes opening up conversations about mental health in fashion, a notoriously punishing industry.

When she died, the Kate Spade New York Foundation contributed $1 million immediately to mental-health and suicide prevention causes. “We really have the authentic responsibility to talk about it and to try to amplify it,” says Liz Fraser, Kate Spade’s current CEO. The company says it is now one of the world’s largest corporate donors to women’s mental-health initiatives.

During Kate’s time, such things weren’t spoken of. While the designer’s friends and family maintain that she was for the most part a genuinely happy, ebullient woman who loved her life and her family, everyone has their private struggles, and she was no different.

“Everyone’s like, ‘Well, what happened?’ ” says Bell. “I don’t think any one thing happened.”

Andy and Kate Spade were separated at the time of her death, but they were still very much a family unit with their daughter, known as Bea. “We loved each other very much and simply needed a break,” he said at the time.

Bell, who is a co-founder with Kenneth Cole of the Mental Health Coalition, says that she and Kate had a euphemism for therapists: “the contractor”—as in, someone who can fix you. “I regret that, because I think that we could have just said therapist…. I think we should have talked about it more openly,” she says.

The co-founder talks about how rough menopause can be on women and says that she’s been recommending Miranda July’s novel All Fours, which deals with that very topic, to everyone she knows: “I read it and I was like, I wish I knew this then.”

Kargman remembers thinking that Kate’s drinking had gone from celebratory to solitary in the last years of her life. She says, “I think I was already looking at it through the prism of slight worry, but never in a million years did I think she would take her life, not in a million years.” In a statement at the time of her death Andy said Kate was on medication for depression and anxiety but that there were no substance-abuse issues.

When a person becomes a brand, even when they are beloved, boundaries blur. Kate talked about adding “Frances Valentine” to her many names in 2016 to differentiate herself from the namesake brand she sold. But in a panel talk with Andy the following year, she seemed unsure about it. “I get confused,” she said. She ended up adding just “Valentine.”

One day, while shopping with Bea at a Kate Spade store after she had left the company, she was tickled when a sales associate asked if she was on the mailing list. She would have never cried, “I am Kate Spade.” When she appeared on her brother-in-law David’s sitcom Just Shoot Me in 2002, her only request was that her part become smaller.

While some might see a contradiction between a brand built on colour and optimism and the spectre of mental-health issues, Naiman thinks that makes the message behind Kate’s legacy all the more potent. She says, “I think that the deepest truth is that there’s something so powerful and incredible about saying that this person who made this incredibly joyous brand struggles.”

Today, Andy runs his Partners & Spade creative agency in California, and is still a partner in Frances Valentine as well as his pajama company, Sleepy Jones. He’s working on a sculpture show about Kate called Uncommon Flowers. He is, as ever, brimming with ideas, and very much still processing the death of the person he calls “the most beautiful woman I’ve ever seen.”

He chose the Bay Area, for one, to be off the grid: “It was purposeful to be disconnected, because my daughter and I didn’t want to be around the mayhem.”

In the early Kate Spade days, Andy would use the word mercury to describe a certain undefinable je ne sais quoi, a taste, a feeling. Recalling an old thermometer, he notes how you can’t put your finger on the quicksilver—it jumps at the merest touch. “I always thought we were mercury,” he says. “Just when they think they know who we are, it changes.”

Or as Kate herself put it, in 1998: “I mean, shit, we’re just doing what we like.”

An auction of clothing, props, and decor from the hit sitcom “Friends,” will be held next month to celebrate the 30th anniversary of the show’s premiere.

The sale, which will be held by Julien’s Auctions live in Los Angeles on Sept. 23 and online, will offer 110 lots of original props, studio-made reproductions and costumes worn by stars Jennifer Aniston, David Schwimmer, Matt LeBlanc, Courtney Cox, Lisa Kudrow, and the late Matthew Perry.

Leading the auction is a studio-made reproduction of the couch from Central Perk, the coffee shop that serves as a main hangout spot in the show. The orange upholstered sofa has a price estimate between US$2,000 andUS$3,000.

The studio-made reproduction of the couch from Central Perk has an estimate of between US$2000 and US$3000.

Other auction highlights include one wardrobe item from each member of the main cast, which includes Rachel Green’s grey sweater from season 7’s “The One With the Truth About London”; a blue long-sleeved shirt worn by Ross Geller in season 9’s “The One with the Boob Job”; and a teal, cashmere polo-style sweater worn by Chandler Bing in season 7’s “The One with the Holiday Armadillo.”

Rachel Green’s grey sweater from season 7

Also up for sale are Joey Tribbiani’s brown, striped short-sleeved button-down shirt from season 10’s “The One After Joey and Rachel Kiss”; Monica Geller’s brown and tan knit top from season 9’s “The One with the Mugging”; and a blue denim coat with faux fur on the cuffs and neck and embroidered Japanese flowers worn by Phoebe Buffay in season 7’s “The One With Joey’s Award.”

Each wardrobe piece worn by the main cast has a price estimate between US$1,000 andUS$1,500.

Costumes worn by notable guest stars will also be up for sale, including a polo shirt worn by Paul Rudd, a fur-trimmed jacket worn by Christina Applegate—who plays Rachel’s sister Amy—and a bright-pink dress and coat worn by Winona Ryder. Each of these items is estimated to sell between US$600 andUS$800.

Some original props included in the auction are five “Monica’s Catering” business cards (estimate: US$100-US$200 each) and a blue metal bike used by Ross’ son Ben—played by Cole Sprouse—in the season 7 episode “The One With All the Candy” (estimate: US$500-US$700).

“Monica’s Catering” business cards (estimate: US$100-US$200 each)

“Friends” first aired on Sept. 22, 1994, and ran for 10 seasons, concluding with a 2004 series finale, which is the fifth-most-watched series finale of all time and the most-watched television episode of the 2000s.

Wildfires in California have grown more frequent and more catastrophic in recent years, and that’s beginning to reflect in home values, according to a report by the San Francisco Fed released Monday.

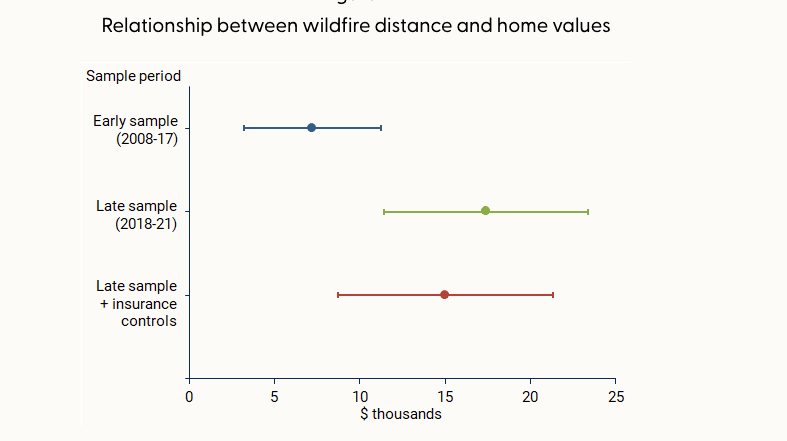

The effect on home values has grown over time, and does not appear to be offset by access to insurance. However, “being farther from past fires is associated with a boost in home value of about 2% for homes of average value,” the report said.

In the decade between 2010 and 2020, wildfires lashed 715,000 acres per year on average in California, 81% more than the 1990s. At the same time, the fires destroyed more than 10 times as many structures, with over 4,000 per year damaged by fire in the 2010s, compared with 355 in the 1990s, according to data from the United States Department of Agriculture cited by the report.

That was due in part to a number of particularly large and destructive fires in 2017 and 2018, such as the Camp and Tubbs fires, as well the number of homes built in areas vulnerable to wildfires, per the USDA account.

The Camp fire in 2018 was the most damaging in California by a wide margin, destroying over 18,000 structures, though it wasn’t even in the top 20 of the state’s largest fires by acreage. The Mendocino Complex fire earlier that same year was the largest ever at the time, in terms of area, but has since been eclipsed by even larger fires in 2020 and 2021.

As the threat of wildfires becomes more prevalent, the downward effect on home values has increased. The study compared how wildfires impacted home values before and after 2017, and found that in the latter period studied—from 2018 and 2021—homes farther from a recent wildfire earned a premium of roughly $15,000 to $20,000 over similar homes, about $10,000 more than prior to 2017.

The effect was especially pronounced in the mountainous areas around Los Angeles and the Sierra Nevada mountains, since they were closer to where wildfires burned, per the report.

The study also checked whether insurance was enough to offset the hit to values, but found its effect negligible. That was true for both public and private insurance options, even though private options provide broader coverage than the state’s FAIR Plan, which acts as an insurer of last resort and provides coverage for the structure only, not its contents or other types of damages covered by typical homeowners insurance.

“While having insurance can help mitigate some of the costs associated with fire episodes, our results suggest that insurance does little to improve the adverse effects on property values,” the report said.

While wildfires affect homes across the spectrum of values, many luxury homes in California tend to be located in areas particularly vulnerable to the threat of fire.

“From my experience, the high-end homes tend to be up in the hills,” said Ari Weintrub, a real estate agent with Sotheby’s in Los Angeles. “It’s up and removed from down below.”

That puts them in exposed, vegetated areas where brush or forest fires are a hazard, he said.

While the effect of wildfire risk on home values is minimal for now, it could grow over time, the report warns. “This pattern may become stronger in years to come if residential construction continues to expand into areas with higher fire risk and if trends in wildfire severity continue.”