A Mid-Century Modern home in Carmel, California, hit the market on Friday for just the third time in 70 years with a listing price of $4.25 million.

Located in the community of Carmel Highlands, the house is just steps from the coastline and comes with private beach access, according to the listing with Tim Allen of Coldwell Banker Realty in Northern California. Allen was not immediately available for comment.

The property last changed hands in 2010 when Hollywood screenwriter Richard Outten bought it for $990,000, public records show. Outten penned the screenplays for the 1992 movie “Pet Sematary Two” and the 1987 film “Lionheart,” and created the story for the 2012 “Journey to the Center of the Earth” sequel, “Journey 2: The Mysterious Island.” He was not immediately available for comment.

Built in 1953, the home’s mid-century charm has been preserved over the years while still being updated for modern living. Interior details include wood paneling, exposed-brick walls and beamed ceilings.

The single-level house has 1,785 square feet, which includes three bedrooms and two full bathrooms. Though not directly on the water, large windows flanking the adobe-brick, wood-burning fireplace look out at the ocean.

Sliding glass doors create a seamless flow between indoor and outdoor living. Outside, there’s a large patio surrounded by lush landscaping, and there are also meandering paths through sustainable succulent gardens, according to the listing.

In addition to its close proximity to the beach, the home is a 10-minute walk from downtown Carmel-by-the-Sea.

As of July, the median list price in Carmel is $3.1 million, up 8% from last year, even as active listings have increased 50% year over year, according to data from Realtor.com.

Christie’s is selling a painting from Claude Monet’s earliest Nymphéas series at the first evening auction taking place in its new Hong Kong headquarters this fall.

Nymphéas (Water Lilies), painted circa 1897-99, is among seven works by the French impressionist that were his first forays into exploring variations in light, colour, and reflections in the water lily pond at his home in Giverny, France.

The work, which Christie’s said is being offered from an anonymous private collection after remaining with the Monet family for years, is expected to sell for between US$25 million and US$35 million.

Christie’s Cristian Albu, head of 20th/21st-century art for Asia Pacific, called the painting “a true singular treasure.” It’s about 2 feet, 4 inches by 3 feet, 3 inches in size.

Monet created more than 250 paintings of waterlilies in his lifetime, several of which have sold for record sums at auction. Last November, Le bassin aux nympheas , 1917-19, sold for US$74 million, with fees, at Christie’s in New York. (Estimated auction prices don’t include fees).

The highest price for a Nymphéas was set during Christie’s sale of the Peggy and David Rockefeller Collection , fetching nearly US$85 million, with fees.

What’s notable about the work Christie’s is selling in Asia is that it’s among Monet’s first to focus on waterlilies, and that it introduces what the auction house said is “one of the most important and radical aspects of his Nymphéas —the elimination of a horizon line.” As with many of these works, the viewer looks directly at the pond’s centre, “removing all other peripheral details to focus entirely on the constantly shifting relationships between water, atmosphere, and light that transformed the pond’s surface with each passing moment.”

Other examples from Monet’s first water lilies series can be found in the Musée Marmottan Monet in Paris, the Los Angeles County Museum of Art, the Kagoshima City Museum of Art in Kagoshima, Japan, and the Galleria Nazionale d’Arte Moderna in Rome.

The Hong Kong sale, which will take place on Sept. 26, will be Christie’s first at its new Asia-Pacific headquarters in the Henderson, a newly built 39-floor skyscraper by Zaha Hadid Architects with a curved glass facade.

If the Federal Reserve cuts interest rates in the coming weeks, a friendlier borrowing environment could make all the difference for some mothballed renewable-energy projects.

The returns generated by such projects once they are up and running are often predictable and modest, but because they require a large upfront expenditure, frequently funded in part by debt, they are sensitive to interest-rate fluctuations.

With recent economic data suggesting the Fed has plenty of room to cut, some investors say now is the time to get moving on renewable plans.

Thomas Byrne, chief executive at solar investor CleanCapital, said a drop in interest rates would affect a “not inconsequential amount” of solar developments under consideration. “We have had projects on hold that simply don’t make economic sense for us anymore because the borrowing cost was too high. So those projects will immediately unlock,” he said.

Byrne estimates some of these projects could begin construction by the end of the year and start generating energy next summer.

Solar and wind energy in particular stand to gain from lower borrowing costs, said Srinivasan Santhakumar, principal research analyst with the research firm Wood Mackenzie. “Higher interest rates have disproportionately affected the economics of wind and solar projects,” he said.

An interest-rate increase of 2 percentage points could result in a 20% jump in the cost of producing energy for utility-scale solar power over the life cycle of a project, according to a Wood Mackenzie analysis released in April. In comparison, the same increase might boost the cost of producing energy from gas by 10% to 12%.

Some developers may wait to see a steeper drop before making moves. “It’s definitely a phenomenon, particularly for the more sophisticated, more longer-standing developers who’ve had a history of surfing the ups and downs of the interest-rate spectrum and are also aware of the consequences for their own balance sheet of a long-term interest rate rise,” said Katherine Mogg, managing director at the New York Green Bank, a state-sponsored investment fund that focuses on filling gaps in energy transition financing. Mogg said she expects to see a modest uptick in requests for proposals in the coming months.

The Federal Reserve has signalled a rate cut at its next meeting in September, and most futures investors expect a quarter-percentage-point reduction, according to CME FedWatch. More than three quarters of investors expect the Fed to lower its benchmark rate, now in a range between 5.25% and 5.5%, by at least a full percentage point by year-end.

While a cut in interest rates is a positive for renewables financing, a durable boost for green projects may require a Goldilocks economic scenario in which a cut to borrowing costs don’t coincide with rising fears of a global recession, which could in turn drive investors away from the U.S., said Ron Erlichman, partner at the law firm Linklaters.

“There are a lot of different factors, like the old cliché of ‘headwinds,’ that affect transactions,” he said, adding that large-scale projects such as offshore wind, hydrogen and carbon capture frequently rely on foreign investment.

Fears of unchecked inflation and rampant increases in the cost of materials have cooled down somewhat in the past year, he said, but the looming U.S. election brings a fresh element of uncertainty . While many see a low probability of a full rollback of the Inflation Reduction Act, the legislation that provides game-changing tax breaks for renewables, an executive branch hostile to green energy could slow project permitting or otherwise “nibble at the fringes” of the landmark legislation, as Byrne put it.

“Having done this awhile and seen the cycles in the market, I still remain incredibly optimistic about renewables and energy transition in the United States,” Erlichman said.

In many ways, Alexandra Cruse is living the American retirement dream.

Cruse moved to Palm Beach Gardens, Fla., a year and a half ago to escape the cold winters in Massachusetts. She describes her financial situation as “perfectly comfortable” after a career in banking. She keeps active with yoga, volunteering at a local hospice, piano lessons, art classes and a bicycling group.

One thing she’s not interested in: saying “I do.” Cruse lost her husband of nearly four decades, Stephen, in 2015. And while she’s open to meeting a new partner, she has no desire to remarry.

“What would be the point?” said Cruse, 68. “Just the commingling funds is just too complicated.” Besides, “over 65, you’re not going to have any children.”

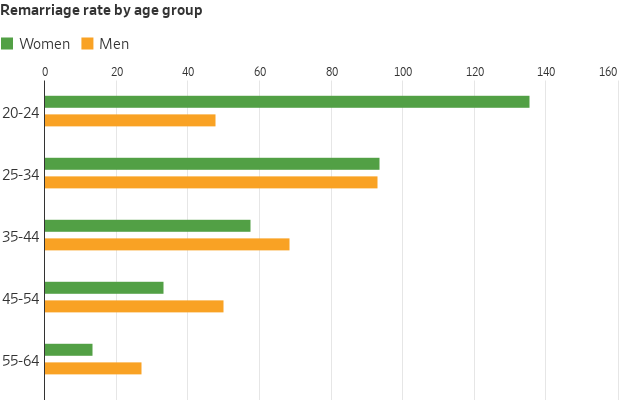

Plenty of American women are finding that they don’t need a husband to enjoy their golden years. Both men and women in their mid-60s or older are more likely to be divorced or never married than at any time in the past three decades. But the women are much less likely than their male counterparts to get remarried.

Part of the reason is that women have a smaller pool to choose from. They on average live about five years longer than men, according to the federal Centers for Disease Control and Prevention.

About 53% of U.S. women 65 and older are divorced, widowed or never married, compared with 30% of men, according to an analysis of Census Bureau data by Bowling Green State University’s National Center for Family & Marriage Research.

But there are other considerations, too. Women are more likely to maintain stronger social ties with family and friends, which means they have more support after a divorce or the death of a spouse. And for both men and women, American society has become more accepting of couples living together outside of marriage.

Susan Brown, a sociology professor at Bowling Green and one of the authors of the Census analysis, said that many older women “don’t want to be a ‘nurse or a purse.’ ” That means, Brown said, that they “don’t want to provide care and they don’t want to jeopardise their own financial stability.”

That’s the case for Christy Sahler, who has been divorced for almost three decades. She has no plans to remarry, as she wants to ensure her assets pass only to her daughter.

“It’s a bit lonely having dinner on my own,” said Sahler, who is 61 and lives in Tucson, Ariz. “But I recognise that if I had a partner I’d be going home to make dinner for that person.” Being single also frees her up to do other things in the evenings, like yoga and pottery.

After a divorce or bereavement, younger women are more likely than men to find a new partner. That trend shifts after age 35. By age 55 to 64, men are twice as likely to remarry, and more than three times as likely when they are age 65 and older.

The last time Pew Research Center polled divorced or widowed Americans about their intentions to remarry , in 2014, 54% of women said they didn’t want to get married again. Only 30% of men gave the same answer.

Research shows that marriage tends to be good for a person’s finances. Married people have a higher median net worth and are more likely to be homeowners than their unmarried peers, thanks in part to their ability to split costs, pool assets and get certain tax breaks.

Divorce is financially detrimental at any age, but particularly punishing later in life when people have less time to catch up financially. Women who divorce at age 50 or older experience a 45% decline in their standard of living, while men see their standard of living drop by just 21%, according to a 2021 study in the Journals of Gerontology. That can make women especially hesitant about entering another marriage: They worry about having to go through the same thing again.

Remarriage can also create thorny disputes around issues like inheritance and power of attorney, especially when both partners bring children into the relationship. Widows and divorcées who remarry may lose eligibility to their former spouse’s Social Security benefits.

Norma Israel’s first marriage ended in divorce when she was in her 30s, and she lost her second husband to cancer in her 50s.

She wasn’t looking for another relationship when, a year later, a co-worker invited her to a concert. She and Larry Chase have now been together for a decade and live together in North Beach, Md. They share a love for music and travel, but they don’t share bank accounts. And Israel has no plans to put a ring on it.

“It’s hard for me to have three strikes,” said Israel, 63.

Chase said he would get remarried if it were important to Israel, but he’s equally happy not to.

“Society seems pretty OK with it nowadays,” said Chase, 78, who was previously married and has a son.

“We’re in love,” he added. “It’s a pretty nice life.”

Na’ama Shenhav, who teaches public policy at the University of California, Berkeley, found that when women’s wages increase relative to men’s, so does the share of women who choose not to marry. The share of divorced women also rises when women’s wages increase.

Rosemary Hopcroft, a sociology professor emerita at the University of North Carolina at Charlotte, found that higher-income men are more likely to get married and remarried than men who make less money. For women, the effect is the opposite, at least for remarriage: Higher-income women are less likely to get remarried than other women.

“As women get older, the group of men they find attractive gets smaller and smaller; whereas for men, as they get older and more financially stable, the group of women they find attractive gets larger and larger,” said Hopcroft.

What’s more, longer lifespans mean people are looking at their golden years with a different time horizon. By the end of this year, the youngest of the baby boomer generation—around 70 million strong, or one in five Americans— will all turn 60 . According to the Social Security Administration, a 60-year-old man today can expect to live for nearly 24 more years, while a 60-year-old woman can expect to live for nearly 27 more years.

“For a lot of people that means thinking, ‘Am I going to stay in a potentially unsatisfying relationship for the rest of my life if the rest of my life is decades instead of years?’ ” said Jeffrey Stokes, associate professor at the Gerontology Institute at the University of Massachusetts Boston.

Today, overall divorce rates are falling. But the share of adults ages 65 and up who were divorced in 2022 was nearly triple the 1990 level, according to the Bowling Green analysis .

Lyn Silarski divorced in her early 50s after 16 years of marriage. A period of financial hardship followed, as she had to restart her career and deal with legal costs. She had to dip into her retirement savings and sell her house during a three-year spell of unemployment.

Today, Silarski is working as a graphic designer and living in a rented house in Manchester, N.H., enjoying the fact that she’s no longer responsible for the upkeep of the outdoors of the property. In her free time, she works out and goes hiking.

“I often say I wish I had a man to run around with, somebody who was a friend who wanted to do things, because I do have the girlfriends but they’re married and they’re busy,” said Silarski, 69.

Silarski, who has two sons and one grandchild, tried online dating, but found men her own age wanted to date younger women. Older men interested in a relationship with her were looking for someone to take care of them, she said.

“Perhaps someone might come along who would be an incredible fit,” Silarski said, “but I see that as kind of in the realm of miracles, really.”

Corrections & Amplifications undefined Research by Rosemary Hopcroft, a sociology professor emerita at the University of North Carolina at Charlotte, found that higher-income women are less likely to get remarried than other women. An earlier version of this article incorrectly implied the research also found they are less likely to get married. (Corrected on Aug. 24)

An opportunity could be on the horizon for those who deferred a home purchase in some of the luxury real estate markets that boomed during the pandemic as demand falls.

Among them, the Miami and Naples areas of Florida; urban Honolulu; and Santa Fe, New Mexico, could be among the best luxury markets in the U.S. for buyers this fall, according to data Realtor.com provided to Mansion Global. The data was staked on a combination of falling luxury median price points, which indicate markets that are softening and where buyers could potentially score a deal; a shift in median days on market; and page views, with fewer views indicating less demand.

“We see that these higher-priced markets are seeing falling demand,” said Hannah Jones, senior economic research analyst at Realtor.com . “And so for buyers who do have access to the capital that they could purchase in one of these markets, they may find more flexibility than in some of the markets that are lower priced and are still seeing a ton of competition.”

Read on for where the opportunity lies and advice in those markets from real estate agents on the ground.

Miami, Fort Lauderdale and Pompano Beach, Florida

Buyers who couldn’t get enough of the sandy shores of this trio of South Florida cities during the pandemic have largely backed off, making it the No. 1 destination for luxury buyers this fall.

The luxury median listing price in Miami, Fort Lauderdale and Pompano Beach was down 22% to $2.5 million in the second quarter. Between June 2023 and June 2024, the median days on market for luxury listings rose five days and in the same time page views of luxury properties on Realtor.com fell a whopping 44%.

Mick Duchon, a Miami-based agent with Corcoran, said that some sellers who were stuck in the high-price mindset of 2021 and part of 2022 are starting to come around, meaning there are still properties out there with a listing price ripe for an adjustment. He said it’s an opportunity for people who have been waiting on the sidelines.

Case in point, Duchon was working with a buyer on a penthouse apartment in the South of Fifth neighbourhood in the summer of 2022, when the market had just started to adjust from its pandemic highs. After approaching the seller with a deal and agreeing on it, the buyer decided to wait. undefined undefined “Two years later, we transacted at 15% below that initial contract price,” on the same penthouse with the same buyer and seller, he said.

He added, “If buyers are basing their offers on what has transacted recently, then they should be able to achieve a solid deal.”

The peak Covid rush to Honolulu has abated somewhat. Pixabay

Honolulu

Realtor.com found that the median luxury listing price in Honolulu fell nearly 10% to $2.34 million in the second quarter. In June, the median days on market for luxury listings fell 11 days compared to a year ago, while in the same time frame, luxury page views fell 31%, indicating less interest, making Honolulu the No. 2 market for buyers this fall.

Noel Shaw, an agent with Hawai’i Life Real Estate Brokers Forbes Global Properties, said the peak Covid rush to Honolulu has abated somewhat, but other buyers who decided to change their lifestyle and move there as part of their 10-year plan are still trickling in. It’s keeping competition up for those mid-tier luxury listings and makes it imperative to work with an agent who knows the city like the back of their hand. (Shaw grew up in Honolulu, and said the quality of real estate varies block by block.)

“This is an island, the city’s very limited so we still have a limited supply,” she said. “So while there are going to be some great deals within the city, it’s not going to be as easy or obvious as other cities.” undefined undefined The listings luxury buyers should keep an eye out for are the top-tier properties of Japanese sellers, she said. Honolulu is a prestigious second-home market for Asians, Shaw said, but the weakness of the yen right now means that some Japanese owners may choose to sell and convert their funds back to yen. Those prized properties, which are rare in Honolulu because of the constraints on inventory, are the extra sweet spot for luxury buyers looking for top-of-the-line properties these days, she said.

Naples-Marco Island, Florida

The market frenzy has quelled in this Gulf Shore slice of Florida, with the luxury median listing price down 18% to $4 million in the second quarter. The median days on market over the year ending June is the same as the year prior, at 85, but page views on luxury properties are down over 11% in the same time period, bringing the Naples-Marco Island metro into the No. 3 spot. undefined undefined “We’re over the Covid mania, where people came and purchased properties at any price,” said Celine Wells, an agent with Douglas Elliman. “What we’re seeing now is less volume of sales, but very strong sales.”

For potential buyers, “patience is a virtue,” said Chris Wells, Celine’s business partner and husband. Chris added it’s important to have knowledge of the market so you can act quickly when a particularly interesting property comes to market. Most transactions happen in cash, with mortgages brought into the picture post-closing, he said.

He added, “A nice deposit, a quick closing, a cash deal, a short due-diligence period—these are things that help a buyer get the property they desire.”

Mick Duchon, a Miami-based agent with Corcoran, said that some sellers who were stuck in the high-price mindset of 2021. Pixabay

Santa Fe, New Mexico The Sunbelt and Mountain West experienced huge demand in recent years, and the small in-between market of Santa Fe was not immune to that.

Unlike the other cities on this list, demand is still up there, with luxury page views surging nearly 7% and luxury median days on market falling 33 days, to 86, between June 2023 and June 2024. Prices, however, are trending down, with the luxury median listing price having fallen nearly 14% to $2.98 million from April to June. All together, it makes Santa Fe the fourth-best market for luxury buyers this fall. undefined undefined “People are still wanting to come here. Santa Fe is still very, very desirable,” said Ricky Allen of Sotheby’s International Realty – Santa Fe Brokerage. “They’re coming for the size of the city, the climate, the culture, the lifestyle. … I think it’s a good time to be a buyer.” undefined undefined Allen suggested that buyers see as many properties as possible that check most of their boxes. “You never know what those properties are going to end up selling at,” he added.

(Mansion Global is owned by Dow Jones. Both Dow Jones and Realtor.com are owned by News Corp.)

This article was originally published on Mansion Global.

Until a few years ago, Chinese factories supplied the world with Sharpie retractable pens and Oster blenders.

No more.

Consumer giant Newell Brands now makes those products, and more, at its own plants in the U.S. and Mexico. Many of its other products are made in factories in Vietnam, Indonesia and Thailand.

Chris Peterson , Newell’s chief executive, said the company’s shift reduces its dependence on China at a time when both the Democratic and Republican parties “are getting more protectionist in terms of trade policy.”

Tariffs are becoming an entrenched tool tying together geopolitics and trade , and they are playing a bigger role in long-term manufacturing and sourcing decisions. Nowhere are they hitting harder than in China, where importers and exporters are navigating an increasingly complicated regime of levies on goods ranging from semiconductors to mattresses.

“Tariffs have always existed and they’ve always been regarded as a cost of doing business,” said Simon Geale, executive vice president of procurement at supply-chain consulting firm Proxima. “But they’ve been getting much more teeth in the last five or six years.”

The new era of tariffs kicked off under the Trump administration with duties on imports from a swath of countries and a focus on Chinese products ranging from truck chassis to consumer goods.

The Biden administration kept most of the tariffs in place, and then added further duties on Chinese steel, semiconductors and electric vehicles, citing national security concerns and an industrial policy aimed at reviving American manufacturing .

The two candidates in this year’s presidential election look set to continue the trend, as trade, manufacturing and the tools to tie them together take a prominent role in the campaign.

Former president Donald Trump , the Republican nominee, has said he would roll out new tariffs with a potential 10% across-the-board duty on imported goods and a 60% tariff on goods from China.

Vice President Kamala Harris , the Democratic nominee, so far hasn’t indicated a desire to deviate much from President Biden’s trade policies.

Before becoming vice president, Harris diverged from Biden on Trump’s revised North American Free Trade Agreement, known as the United States-Mexico-Canada-Agreement. As a senator, Harris joined some Democratic lawmakers, saying it didn’t do enough to address climate change, suggesting Harris may have more of a focus on social justice issues when considering trade pacts.

Harris has been in lockstep with the president in the Biden administration.

At an electronics factory in Wisconsin last summer, Harris said she and Biden want to bring manufacturing jobs back to America. At a campaign event in North Carolina on July 18, she said Trump’s proposed universal 10% tariff “would increase the cost of everyday expenses for families.” She didn’t criticise current tariffs on Chinese goods .

Both Trump and Harris opposed the Trans-Pacific Partnership, the expansive multination trade deal that was designed to expand alternatives to trading with China. Trump withdrew the U.S. from the agreement immediately on taking office in 2017.

The trade policies pose a conundrum for companies. Do they continue sourcing from China and risk the potential impact of escalating tariffs? Or do they look outside China, where costs are higher, but duties and other geopolitical risks are lower?

Trump’s threat of universal tariffs has even spooked supporters. Tesla Chief Executive Elon Musk , who has endorsed Trump, said he would delay a decision on a new plant in Mexico until after the election because “it doesn’t make sense” if Trump wins and puts “heavy tariffs” on vehicles produced there.

Shifting supply chains to other countries is complex. Companies must find new suppliers of raw materials and finished goods. Suppliers and sub-suppliers must be vetted to make sure they don’t violate increasingly stringent U.S. rules on issues such as forced labor.

Anne van de Heetkamp , a vice president of product management at supply chain and logistics technology company Descartes , said when trade tensions started ratcheting up five years ago companies weren’t in a hurry to shift supply chains. Now that the duties appear more permanent, Descartes’s customers are mapping out new global supply networks.

Surging exports out of Southeast Asia, India and Mexico suggest Newell isn’t alone in its desire to reduce reliance on China. The shifts are fuelling new logistics investments in factories, warehousing and transportation operations around the world.

DHL Express U.S., a parcel unit of German logistics giant Deutsche Post , added a new direct flight between Vietnam and the U.S. in 2022 to cater to rising exports that used to reach the U.S. via Hong Kong. CEO Greg Hewitt said the unit is also looking at expanding its networks along the U.S. -Mexico border to serve surging demand there.

Hewitt cautioned that China remains the world’s top supplier of manufactured goods and will likely hold that position because of its streamlined supply chains and low costs for raw materials and labour.

Retail industry trade groups and some executives warn some items can’t be produced anywhere else in the world and that escalating tariffs will simply raise consumer prices and fuel inflation. Analysts at Goldman Sachs estimate that every percentage point increase in the overall U.S. tariff rate would increase core consumer prices by just over 0.1%.

“The problem is the best place to make shoes is China,” said Ronnie Robinson, chief supply chain officer at Designer Brands , parent company of footwear retailer DSW.

Robinson said for every dollar the government adds in tariffs, consumers pay an extra $2 to $4 at the checkout. “The reality is that you and I are paying for the tariffs as part of the ticket price when you go into the store and buy,” he said.

Robinson said Designer Brands sources about 70% of its footwear from China, down from 90% several years ago. He said the company aims to reduce its reliance further to about 50%, but China will remain the company’s largest single source of shoes.

Peterson said just 15% of Newell’s goods rely on products made in China today, down from more than 30% several years ago. He expects that by the end of next year the share will fall below 10%.

He said that when the company is searching for new Chinese suppliers one of its first questions is whether they have capacity or plan to add capacity outside the country.

“If a supplier doesn’t have manufacturing capability outside of China, we will not select them as a vendor for us,” he said.

Classic car enthusiast Rudi Klein was, by all accounts, a unique character.

The German émigré lived in Los Angeles, where he opened a junkyard called Porche Foreign Auto Dismantling (with the automaker’s name misspelled to avoid litigation). Klein, who passed away in 2001, took in only high-end foreign cars, mostly Mercedes and Porsche, but also BMWs and every brand of supercar, including many very rare examples. The junkyard’s trophies included famous Grand Prix driver Rudolf Caracciola’s 1935 Mercedes 500 K Special Coupe, a rare 1955 Mercedes-Benz 300 SL “Gullwing” (one of 29 with alloy bodywork), and many more.

Stacked-up Porsches are still in place for the auction. Robin Adams/RM Sotheby’s

Most, but certainly not all, of the cars that Klein bought were crashed, burned, or otherwise derelict. A German crew managed to get into Klein’s closely guarded sanctuary, subsequently producing the unauthorised 2017 photo book Junkyard . Many other people were turned away from the gates, and Klein charged such high prices for salvaged parts that purchases were fraught. The doors remained closed after Klein’s sons, Ben and Jason, took over. But now, everything is coming into the light as RM Sotheby’s prepares to auction cars from the Klein collection on Oct. 26 in its current South Los Angeles location, including those two notable Mercedes-Benzes.

Andrew Olson, car specialist at RM Sotheby’s, said Klein’s premises have “an interesting and special atmosphere—if we moved the cars, some of that would be lost. There’s still a rack of Porsche 356s. We took them out to photograph them, but then they went back to where they were.” In Monterey last year, the auction house staged a horde of storm-damaged Ferraris as if they were still in a collapsing warehouse. Klein’s yard provides natural staging.

There’s a total of 180 cars in the sale, Olson says. Most of what was in the yard will be sold, minus some extensively burned cars and those with a current value that would not justify restoration.

The 500 K Mercedes coupe has bodywork by Sindelfingen. It is a one-of-one vehicle, still wearing its original body. The car was restored and caused a stir at the famed Pebble Beach car show in 1966 and then again in 1978. But it was parked under Klein’s ownership in 1980, fortunately under cover. “The condition is surprisingly good,” Olson says. “It’s very solid and should be a straightforward restoration.”

A roomful of Porsche 356s at Rudi Klein’s yard. Robin Adams/RM Sotheby’s

The alloy-bodied 1955 Mercedes 300 SL was the only one delivered in black, and had once been owned by Ferrari importer Luigi Chinetti. The auction house describes it as “a unique example of the most sought-after of all 300 SLs, virtually unseen for decades.” Complementing it is a 1957 300 SL Roadster that was painted Fire Engine Red from the factory, with a cream interior, and coveted Rudge wheels.

Rudolf Caracciola’s 1935 Mercedes 500 K Special Coupe is in “surprisingly good” condition. Kegun Morkin/RM Sotheby’s photo

The 1967 Iso Grifo A3/L Spider is a prototype built by the Italian coachmaker Bertone, and is the only factory-built Grifo convertible. Klein acquired the car, with Chevrolet V8 power, reportedly from auto enthusiast and Hollywood producer Greg Garrison. According to Junkyard : “It was one of Rudi Klein’s all-time favourites, and he hoped one day to rebuild it and take part in a classic-car rally in Bavaria.”

When planning a trip, or seeking a venue for a special celebration, prospective travellers often look at social-media photos of people enjoying possible destinations.

Such selfies can actually make the destinations seem less appealing, according to a recently published study . More specifically, if consumers are considering a place for a self-defining experience such as a wedding, proposal or special vacation, they won’t like it if they see other people pictured there.

The reason, researchers say, is that when a human is featured in a website picture or social-media post of a destination, it can give the viewer a sense that the person pictured has or is signalling ownership of the place.

“We want to stand out by being a little different,” says Zoe Y. Lu , an assistant professor of marketing at Tulane University and the lead author of the paper. “If my cousin saw a picture of my husband proposing to me at a particular national park, for example, my cousin would worry that choosing that same spot to propose to his loved one would be perceived as him being a boring person, lacking a sense of self.”

The ‘experience venues’

Across six studies, Lu and two colleagues looked at when and why human presence in online photos lowers viewers’ preference for what she calls “experience venues”—that is, destinations that serve not only as physical spaces but as symbolic arenas that provide a way for people to define themselves.

In one experiment, Lu and her team asked 416 online participants to look at images of two hiking trails, labeled A and B, and to imagine they were picking one for their New Year’s Day hike. Participants liked trail A better than trail B when no person was shown. If there was a hiker present in the photo of trail A but not trail B, viewers preferred trail A significantly less than when no human was shown. “Our theory is that the hiker in the image offers kind of a territorial signal,” says Lu. “It says to our self-identity, ‘Someone else has been here, don’t try their hike, try a hike that seems like nobody has done.’ ”

In another experiment, participants were asked to imagine the photos they were being shown were of two potential wedding locations for themselves. Fifty-three percent of participants chose location A if neither picture included another couple tying the knot. But if another couple was shown in a photo of location A, and not in location B, only 27% of the participants chose location A.

By contrast, in another experiment, participants were told to imagine they were planning a wedding for someone else. As planners, they didn’t mind whether or not a couple was shown in the photo. “Wedding planners aren’t seeking self-identity the way their clients are,” Lu says.

Online-marketing lesson

Lu says that her research may have some implications for online marketers. “They might encourage previous customers not to post selfies of special experiences if they want new customers to try those experiences at the same location, which seems counterintuitive, I know,” she says.

Hotels and destinations, too, might reconsider including images of clearly visible guests and visitors in their marketing materials. And social-media influencers might want to skip the selfie in paid posts for destinations, so as not to seem territorial. One exception, Lu notes, is when the person in the photo has an identity that is distinct from that of the viewer, such as the owner of the venue, “but you might want to acknowledge that the person shown is the owner,” she says.

The oldest members of Gen X are turning 60 next year. Many can’t afford to stop working any time soon.

Born between 1965 and 1980, Gen Xers launched their careers at the start of a massive shift in how Americans work. Companies moved from pensions that promise steady income after years of service, to plans such as 401(k)s that place employees’ retirement destiny in their own hands.

Some Gen Xers were hit hard in their prime working years during the 2008 financial crisis. Others are still paying off student debt. Their children are increasingly living at home well into adulthood, while their own aging parents often require care. Few believe they can rely on Social Security to make ends meet later in life.

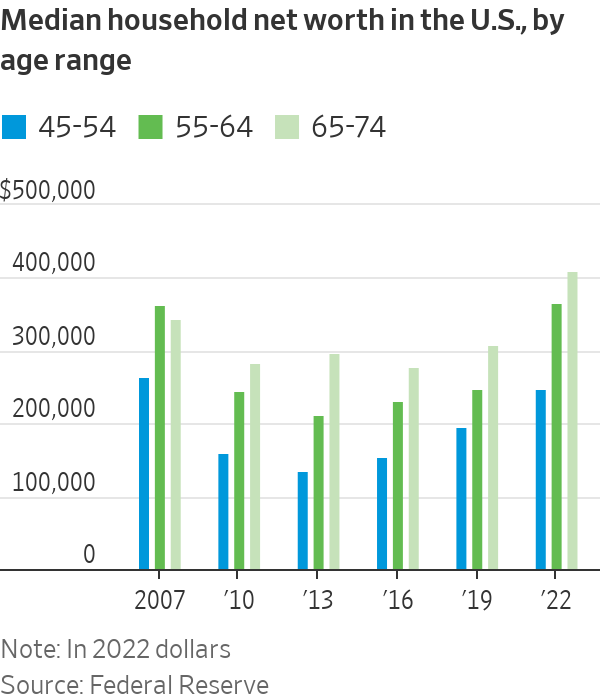

By some measures, Gen Xers are worse off financially than their baby boomer predecessors. The median household net worth of Gen Xers between 45 and 54 years old was about $250,000 in 2022, about 7% lower than that of baby boomers at the same age in 2007, according to inflation-adjusted Federal Reserve data. That was the only age group that experienced a drop in median wealth over the 15-year period.

David Bryan, 55, earns about $35,000 a year as a school-bus driver and lives on Tybee Island, Ga. He doesn’t own property and has about $100,000 in retirement savings from his previous jobs as a railroad conductor and a researcher at a college foundation.

It’s a different life than that of his parents, who worked for decades for the sheriff’s department and the post office and received steady pension checks when they retired.

“As long as my body will let me, it’s better I keep working,” said Bryan.

“As long as my body will let me, it’s better I keep working,” said David Bryan.

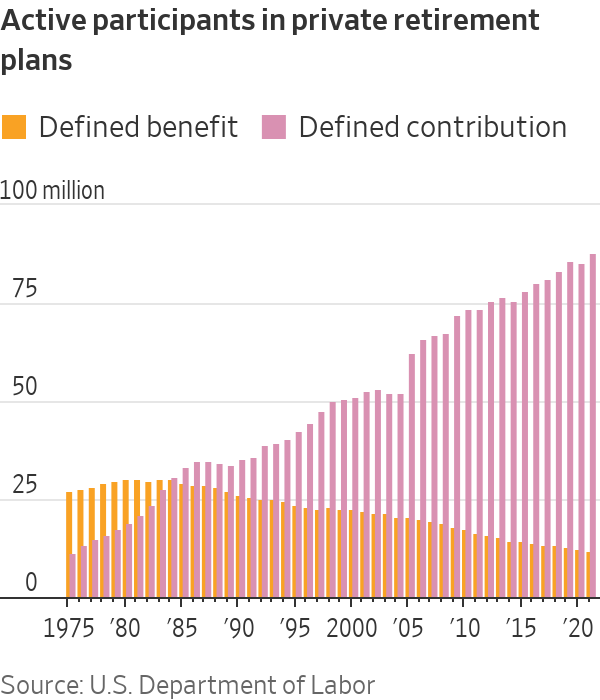

The roughly 65 million Americans in Gen X are sometimes referred to as the “forgotten generation,” sandwiched between the larger and louder baby boomer and millennial generations. They are also called the “latchkey generation,” often coming home from school as children to an empty house. Goldman Sachs Asset Management in a recent report called Gen X the “‘401(k) experiment’ generation.”

For decades, employers often supported loyal workers in old age through traditional pensions with set payouts for life. The advent of the 401(k) system pushed the responsibility on to the individual—and Gen X was caught squarely in the transition.

“Gen X is the first generation where they were mostly expected to figure out their retirement on their own,” said Jeremy Horpedahl , an economics professor at the University of Central Arkansas and director of the Arkansas Center for Research in Economics.

The early champions of the 401(k) never thought that it would become the dominant way most Americans save for retirement. It is named for a line in the tax code changed in 1978 that gave executives a tax-free way to defer compensation from bonuses or stock options. Human-resources executives and economists jumped on the 401(k) as a way to encourage saving for rank-and-file employees.

By the mid-1980s, the number of active participants in defined-contribution retirement plans—such as 401(k)s—overtook those in defined-benefit plans—such as traditional pension plans—in the private sector. Now, private pensions are rare.

When Gen Xers entered the workforce, the 401(k) was a new concept. Features such as automatically enrolling employees in a workplace plan and automatically increasing contributions every year didn’t become commonplace until later.

Other common private retirement savings tools were also introduced in the last half-century. The individual retirement account—a tax-deferred investment vehicle—was authorised in 1974, while the Roth IRA—funded with posttax money, but tax-free when withdrawn—was established in 1997.

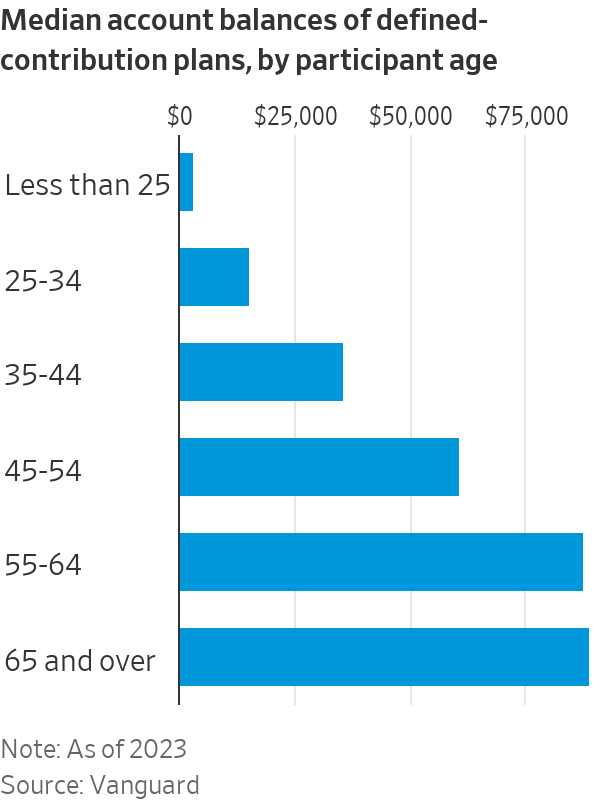

Gen Xers between 45 and 54 years old had a median account balance of roughly $60,000 in defined-contribution retirement plans at Vanguard Group in 2023, according to the firm. For most Americans, that is well below the target some financial experts recommend of having roughly six times one’s salary saved for retirement by age 50.

John Kotrides, a 54-year-old living near Charlotte, N.C., had contributed to 401(k)s ever since he started his career in banking about three decades ago. But whenever he moved to a different employer, he usually cashed out his 401(k) because there was a more urgent expense, such as a home repair or moving costs.

Keeping the money invested in the stock market didn’t seem worth it after witnessing crashes like the bursting of the dot-com bubble. Retirement seemed far away.

“You no longer have a generation of people whose employer took you from your first job into your retirement,” he said. “When we were offered 401(k)s, I don’t think that was a great deal.”

Kotrides says he doesn’t have much in retirement assets, besides the home he owns, where he lives with his wife and two daughters, who are 12 and 20 years old. After quitting his job as a mortgage lender during the pandemic, he now works as a bartender part-time and earns most of his money making social-media content, mostly nostalgic videos about the 1970s through 1990s. He likes having more time to spend with his family.

“This is basically my retirement plan,” he said. “I truly assume that I’ll continue to work to provide for my family as long as I need to.”

Even those who have benefited from the 401(k) system say it hasn’t been easy.

Scott Zibel, a 56-year-old in Leominster, Mass., started putting money in a 401(k) when he began working at a grocery store at 15. His father encouraged him to contribute. The account grew as he continued working at the store through college and became a manager. In his early 30s, he became an English teacher and expects to receive a pension after retiring.

When the stock market crashed in 2020 at the onset of the Covid pandemic, he and his wife pulled the money in his wife’s 401(k) out of the market and into a money-market fund. Now they have reinvested the money, but put a greater portion of it into bonds than before.

“I’m grateful for the 401(k), but there’s no guarantees as well,” he said, estimating his household retirement savings at a little over $1 million.

Zibel feels prepared for retirement but says he has to live frugally to save. He has driven the same car for 12 years and has avoided pricey expenses such as new carpeting for his 30-year-old home.

“My wife and I have done so much planning for the future with our money, it’s made living in the now difficult,” he said.

For some Gen Xers, the 2008 financial crisis was a hit that took years to recover from.

Around 2007, Darling “Diva” Moore was at the peak of her career as a managing partner at a title company in West Palm Beach, Fla. Then the housing market collapsed and her company went under. She couldn’t make rent on her apartment and had to crash with her significant other at the time, sometimes turning to sleeping on the beach or in the car.

“The Great Recession changed everything for us,” said Moore, who is 57. “After that, I don’t know how many Gen Xers trusted that system.”

Darling “Diva” Moore was at the peak of her career when the housing market collapsed.

After settling in Denver, more than two years went by before she landed a new job. She went back to school, getting an online bachelor’s degree in business management and master’s degree in human relations and organisation development. Now she is self-employed as a career counsellor.

As she is approaching her 60s, Moore is trying to locate money she contributed to various 401(k)s from jobs earlier in her career. Whenever she switched jobs, she didn’t rollover her balance to an IRA or new 401(k), so those accounts are scattered across plan providers. “In the ‘90s, they didn’t make it easy to find out where that money is,” she said.

She is also contending with student debt from a for-profit associates-degree program she completed in her 20s that has swelled to nearly $90,000 from around $27,000 due to interest.

More than a quarter of U.S. households led by Gen Xers between the ages of 45 and 54 had education loans in 2022, compared with about 15% of baby boomers at the same age in 2007, according to Fed data.

Soaring tuition costs, sky-high rents and other inflationary pressures for Gen Z are also Gen X’s problem. Many Gen Xers have forked over tens of thousands of dollars for their children to attend college. Young people are also increasingly living with parents, or relying on them for financial support, well into adulthood .

Pamela Likos’s 21-year-old son lives at home with her in the suburbs of Madison, Wis., while another son and daughter are at college.

“My kids are still definitely not grown and flown,” Likos said.

Some Gen Xers are simultaneously caring for aging parents, who are living longer than previous generations.

Likos isn’t in that situation yet, but her stepmother, who has Alzheimer’s, and her father are in their 80s.

“I need my parents to hang on healthwise for another five to 10 years because we are not ready to help financially, really,” she said.

Likos, who is 54, was the first person in her family to go to college, but didn’t work for about two decades after she got married and became a stay-at-home mom. When she got divorced about seven years ago, she found herself with no savings of her own and no resume to apply for jobs. She got a license to work as an esthetician for a few years and now is remarried. From her divorce, Likos received about half of her ex-husband’s 401(k), which comprises most of her plan for retirement.

The youngest members of Gen X are in their mid-40s, offering more time to boost savings ahead of retirement. Tyler Bond, the research director at the National Institute on Retirement Security, wonders if there will be diverging retirement experiences between the older and younger ends of the cohort.

“The older Gen Xers simply may not have time,” he said.

Avery Nesbitt, a 44-year-old operations manager in the Atlanta area, isn’t waiting for retirement to go on nice vacations or buy a new car because he wants to enjoy them now—and he doesn’t expect to be able to save up a cushy nest egg for later in life. If the Covid pandemic taught him anything, it was that anything can happen.

He and his wife have contributed modestly to employer-sponsored retirement accounts but didn’t feel like they could afford to save more. They own a home, where they live with their two children. That makes up the bulk of their wealth. He said he has put more money into life-insurance policies than in retirement accounts.

“I fully expect to work until I die,” Nesbitt said. “It is what it is.”

SYDNEY—Australia’s unemployment rate rose in July to its highest level since late 2021 even as employment jumped by much more than expected over the month, with a record number of people participating in the labor market.

The unemployment rate rose to 4.2% in July from 4.1% in June, the Australian Bureau of Statistics said Thursday.

The economy created a further 58,200 jobs over the month, with full-time employment rising by 60,500, the ABS said. The employment creation was about three times that expected by economists.

The apparent mismatch in the data is explained by a rise in the labour market participation rate to a record high 67.1% in July from 66.9% in June.

Overall, the data suggests the job market remains tight, which will feed the Reserve Bank of Australia’s fears about the availability of labor, wage pressures and sticky core inflation over the coming quarters.

RBA Gov. Michele Bullock ruled out an interest-rate cut over the next six months citing concerns that inflation remains stubbornly high, while firms are reporting the job market is still tight.

The employment-to-population ratio rose by 0.1 percentage point to 64.3%, indicating employment growth was faster than population growth, the ABS said.

“Although the unemployment rate increased by 0.1 percentage point in each of the past two months, the record high participation rate and near record high employment-to-population ratio show that there continues to be a high number of people in jobs, and looking for and finding jobs,” the ABS said in a statement.

The number of people unemployed increased to 637,000 in July, the highest it has been since November 2021, but it remains around 70,000 below its pre-pandemic level, ABS added.

Seasonally adjusted monthly hours worked rose by 0.4%, in line with the 0.4% increase in employment, the ABS said.