In a transaction that further cements NBA Hall of Famer Michael Jordan’s standing atop the world of sports memorabilia, Sotheby’s New York sold six Air Jordan sneakers earlier Friday for the whopping total of US$8 million.

Dubbed the Dynasty Collection, the set of six shoes were sold to an anonymous buyer who was in the room during the bidding, according to the auction house. Sotheby’s had publicised the sale with a far-reaching tour, displaying the sneakers around the world while estimating that the set would sell for between US$7 million and US$10 million.

“To have something from one of Jordan’s championship clinching games is a goal for every collector of sports artifacts. To have something from all six is unheard of,” says Brahm Wachter, Sotheby’s head of modern collectables. “We are thrilled with the result which is a testament to the greatest to ever play the game.”

The Dynasty Collection earned headlining status for the second edition of Sotheby’s “The One,” a cross-category sale that features an eclectic range of notable objects representing human achievement and excellence.

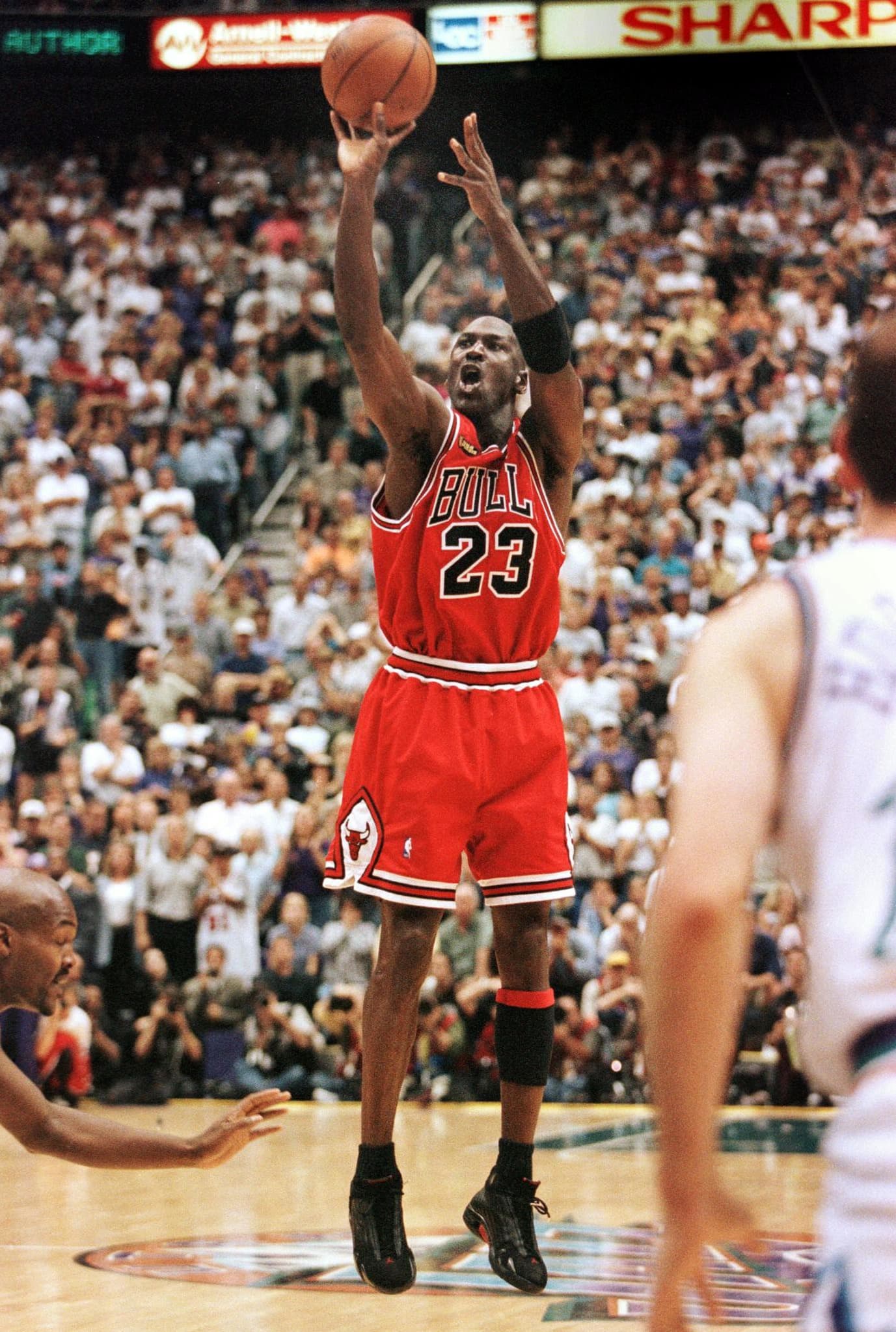

Michael Jordan of the Chicago Bulls shoots the winning jump shot with 5.2 seconds left during game six of the NBA Finals against the Utah Jazz in Salt Lake City in June, 1998. The Bulls won 87-86 for their sixth NBA championship. AFP via Getty Images

As the hammer fell, the final price tag set a new global benchmark for game-worn sneakers while becoming the second-highest price achieved for any Jordan memorabilia, just behind Jordan’s 1998 NBA Finals Game 1 jersey from the famed “Last Dance” season, which achieved US$10.1 million at Sotheby’s in September 2022 and still holds the world record for any game-worn sports memorabilia.

The auctioneer also holds the record for any pair of sneakers, with Jordan’s 1998 NBA Finals Game 2 Air Jordan 13s having earned $2.2 million in April 2023.

Jordan, who turns 61 on Feb. 17, famously handed off one of his size-13 and 13.5 shoes—an Air Jordan VI (1991), Air Jordan VII (1992), Air Jordan VIII (1993), Air Jordan XI (1996), Air Jordan XII (1997), and Air Jordan XIV (1998)—after each championship-deciding victory to Bulls PR exec Tim Hallam.

The sneakers were later obtained from Hallam by a private American collector, who ultimately enlisted Sotheby’s for the sale. Initially announced nearly a year ago, the collection has captured the attention of sports fans and hobbyists alike.

“Today’s record-breaking price is a testament to the GOAT. The Dynasty Collection undeniably ranks among the most significant compilations of sports memorabilia in history,” Wachter said in a statement announcing the result.

“Serving as both a reminder of Michael Jordan’s lasting impact on the world and a tangible expression of his recognised legendary status, its significance is further validated by this monumental result.

One other piece of Jordan memorabilia was included in the auction: the signed official scorekeeper’s sheet from the highest-scoring game of his career—a 69-point effort against the Cleveland Cavaliers on March 28, 1990. It sold for US$50,800.

Board members at Elon Musk’s electric-car maker, Tesla, were facing a dilemma.

One longtime director, the venture capitalist Steve Jurvetson, had left his firm after an internal investigation found he had slept with multiple women in the tech industry and used illegal drugs.

Some of the details had been splashed across the press in 2017, and Tesla directors informally discussed how they should handle it, according to people familiar with the situation. Some urged him to resign.

Luckily, Jurvetson, even though the company designated him an independent director, had a good friend with whom he had deep financial ties and also attended parties with, using ecstasy and LSD: Musk.

Musk pushed directors in private conversations to allow Jurvetson to take an unusual leave of absence from the board of the public company, and then step down on his own accord in 2020, the people said. Jurvetson remains a director at Musk’s privately held rocket company, SpaceX.

“The answer was do nothing and see what happens,” said another former independent Tesla director and good friend of Musk’s, Antonio Gracias, in a 2021 court deposition, when asked how the board handled the Jurvetson situation. Gracias and his venture-capital firm held investments recently valued at about $1.5 billion in Musk companies.

Multiple other directors of Musk companies have deep personal and financial ties to the billionaire entrepreneur, and have profited enormously from the relationship. The connections are an extreme blurring of friendship and fortune and raise questions among some shareholders about the independence of the board members charged with overseeing the chief executive. Such conflicts could run afoul of the loose rules governing what qualifies as independence at publicly traded companies.

On Tuesday, a Delaware judge struck down Musk’s multibillion-dollar pay package at Tesla, saying board members who signed off on it in 2018 were beholden to Musk.

Several current or former directors at Tesla and SpaceX attend parties with him, go on exotic vacations and hang out at Burning Man, the Nevada arts and music festival.

Musk and these directors, including venture capitalists Gracias and Ira Ehrenpreis, tech mogul Larry Ellison, former media executive James Murdoch, as well as Musk’s brother, Kimbal Musk, have invested tens of millions of dollars in each other’s companies—Ellison held billions of dollars in Tesla shares with about a 1.5% holding in 2022. Some also received career support and help from Elon Musk.

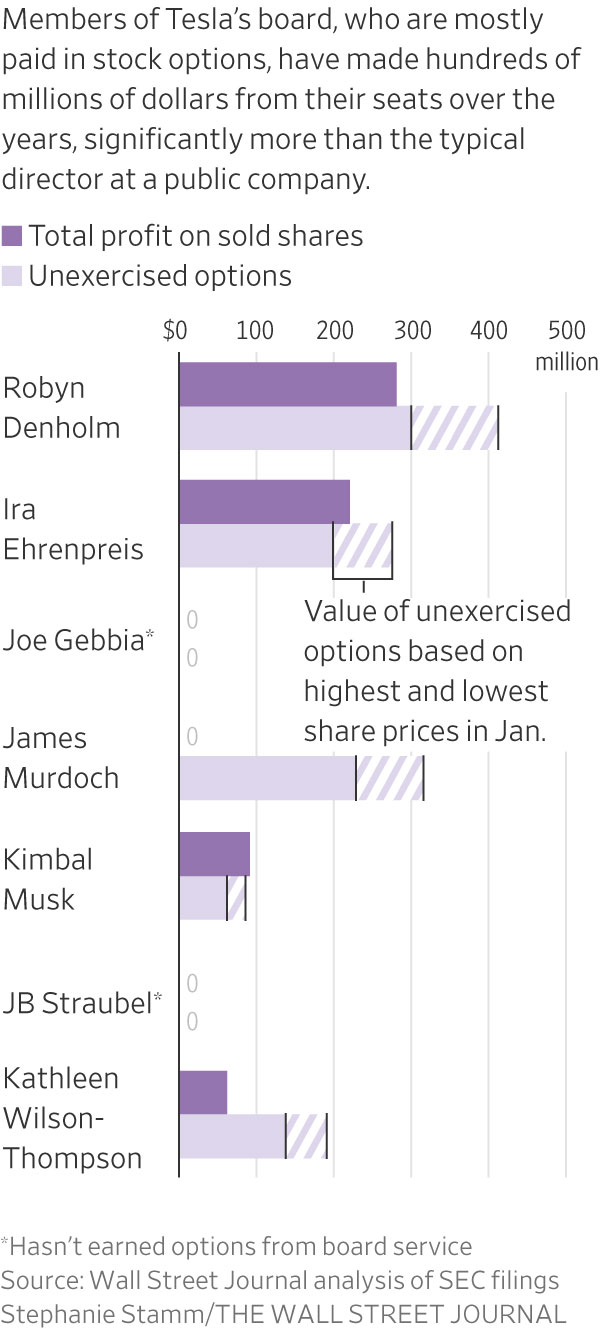

Most members of Tesla’s current eight-person board have amassed shares worth hundreds of millions of dollars from their seats over the years, significantly more than what board members at other companies make for their service.

Tesla pays its directors mostly in stock options, and the current board, not including Musk himself, collectively has made more than $650 million selling shares from those options. They hold additional options valued at nearly $1 billion. Some directors agreed to return a portion of that compensation to Tesla to resolve a shareholder lawsuit about their compensation while denying any wrongdoing. A judge has yet to approve the settlement.

Some current and former Tesla and SpaceX directors have knowledge of Musk’s illegal drug use but haven’t taken public action, according to people who have witnessed the drug use or were briefed on it.

The Wall Street Journal reported in January that Musk has used drugs including cocaine, ecstasy, LSD and magic mushrooms, and that leaders at Tesla and SpaceX were concerned about it, particularly his recreational use of ketamine, for which Musk has said he has a prescription. The illegal drugs violate strict anti drug policies at Musk’s companies and could put SpaceX’s federal contracts and Musk’s security clearance at risk.

At the upscale Austin Proper Hotel, Musk has attended social gatherings in recent years with Tesla board member Joe Gebbia, the Airbnb co-founder and a friend of his, where Musk took ketamine recreationally through a nasal spray bottle multiple times, according to people familiar with the drug use and the parties.

Other directors, Gracias, Jurvetson and Kimbal Musk, have consumed drugs with him, according to people who have witnessed the drug use and others with knowledge of it.

Musk and some people close to him, including Kimbal Musk, attend parties at Hotel El Ganzo, a boutique hotel in San José del Cabo, Mexico, known for its art and music scene as well as drug-fuelled events, according to people familiar with the parties.

The volume of drug use by Musk and with board members has become concerning, some of these people said.

In the culture Musk has created around him, some friends, including directors, feel there is an expectation to consume drugs with him because they think refraining could upset the billionaire, who has made them a lot of money, some of the people said. More so, they don’t want to risk losing the social capital that comes from being close to Musk, which for some feels akin to having proximity to a king.

Musk and his lawyer, Alex Spiro, didn’t respond to requests for comment.

In response to the Journal article in January about Musk’s illegal drug use, Spiro said Musk is “regularly and randomly drug tested at SpaceX and has never failed a test.”

After that article, Musk tweeted that in three years of undergoing random drug testing after a pot-smoking incident in 2018, “Not even trace quantities were found of any drugs or alcohol. @WSJ is not fit to line a parrot cage for bird [poop emoji].” He later tweeted: “If drugs actually helped improve my net productivity over time, I would definitely take them!”

Tesla’s general counsel and a SpaceX spokesman didn’t respond to requests for comment.

Ellison offer

Some board members worry about the negative effects of Musk’s behaviour on the six companies he oversees and the roughly $800 billion in assets held by investors, according to people close to Musk.

Despite the concerns, the Tesla board hasn’t investigated his drug use or recorded their worries into official board minutes, which could become public.

Around the winter of 2022, Musk’s good friend and former Tesla board member, Ellison, urged him to come to his Hawaiian island to relax from work and dry out from the drugs, according to people familiar with the offer.

The outreach came as friends and others close to Musk worried that his drug use was getting worse, and some asked him to go to rehab, some of the people said.

Around the same time as the Ellison offer, Musk attended a party in the Hollywood Hills where he consumed a liquid form of ecstasy from a water bottle, according to a person who was there. Musk’s security guards asked people to leave the floor of the house for privacy before Musk took the drug.

Across Silicon Valley, executives sometimes invest in each others’ companies and ventures, and might have one or two personal friendships on a company board, especially before it goes public.

Musk, because of the extent of his personal and professional board ties and the enormous amount of money involved, is the most prominent example of a chief executive who is intertwined with directors. The Journal traced connections by reviewing hundreds of pages of court documents and depositions, Securities and Exchange Commission filings and other public records.

The amount Tesla pays its directors is far more than the average compensation for boards at most U.S. companies. The average total compensation for board members in the largest 200 U.S. companies was $329,351 in 2023, according to a new report from the National Association of Corporate Directors and compensation consultant Pearl Meyer. By comparison, current Alphabet board members hold stock valued at about $8 million, and received an average annual compensation for board service of about $475,000 since 2015.

Beyond board pay, some Tesla and SpaceX directors have tens of millions of dollars in additional investments in Musk’s companies, including his brain implant startup, Neuralink, and his tunnelling venture, The Boring Co.

Musk, in turn, invests in some directors’ companies. Board members also have invested in Kimbal Musk’s Kitchen Restaurant Group and in SolarCity, a company run by Musk’s cousins that was acquired by Tesla.

Governance experts, such as longtime board members and advisers to boards, say the personal and financial ties could muddy directors’ views, and that it is highly unusual at U.S. public companies.

According to the rules of Nasdaq, where Tesla trades, an independent director can’t be an employee, a family member or someone whose relationship “would interfere with the exercise of independent judgment.” Nasdaq requires a majority independent board.

While rules governing independent directors across the country are murky, financial entanglement is one area where courts have sometimes found public companies at fault for claiming directors’ independence while they hold investments tied to one another.

Amalgamated Bank, which managed around $180 million of investments in Tesla as of September, signed a shareholder letter last year asking Tesla board members to step up their “meagre oversight” of Musk.

The investors expressed concern that the close ties between Musk and several Tesla directors make the board ill-equipped to act in the best interest of shareholders.

CEO with leeway

Some directors view Musk as a once-in-a-generation genius, with a brilliant mind and unusual methods. In depositions and courtroom testimony, directors have said they think Musk’s leadership is crucial to both Tesla and SpaceX, and believe in his long-held mission to colonise Mars. He is seen as the soul of his companies and intertwined with their success. Tesla’s stock is up more than 300% in the past four years, but has dropped about 25% since the beginning of January.

When striking down Musk’s pay package on Tuesday, the Delaware Court of Chancery judge called the process for approving it “deeply flawed” and cited Musk’s “extensive ties” to some of the directors who negotiated it. A Tesla shareholder had sued, alleging Musk played too big a role in deciding his own pay.

Musk “enjoyed thick ties with the directors tasked with negotiating on behalf of Tesla, and dominated the process that led to board approval of his compensation plan,” wrote Chancellor Kathaleen McCormick in the opinion. She described board Chair Robyn Denholm’s approach to her oversight obligations as “lackadaisical.”

Tesla board members can appeal the decision to the Delaware Supreme Court. After the ruling, Musk posted on X saying, “Never incorporate your company in the state of Delaware” and said Tesla would hold a shareholder vote about incorporating in Texas.

Board members had signed off on the pay deal in 2018, with Tesla valuing it at a maximum of $55.8 billion. It was the biggest pay package ever to the chief executive of a U.S. public company, according to governance-data firm Equilar.

While negotiating the pay package, Musk emailed the company’s top lawyer explaining how he would use the additional compensation. “The added comp is just so that I can put as much as possible towards minimising existential risk by putting the money towards Mars,” Musk wrote. Ehrenpreis, a yearslong friend, was head of the board’s compensation committee.

Company directors frequently allowed Musk an unusual amount of leeway on issues big and small.

After he bought Twitter in 2022, for example, Musk tapped Tesla employees to review the social-media platform’s engineering talent. Also around that time, SpaceX signed off on an unusual $1 billion loan to its chief executive, the Journal has reported.

A 2018 settlement with the SEC, following Musk’s tweet about plans to take Tesla private, required Tesla to establish more controls and form a new committee of independent board members to oversee Musk’s communications. But according to court documents, Denholm said Musk “does self-regulate” compliance, and some directors said they don’t review his tweets.

Tesla disclosed in 2022 that it had received a subpoena from the SEC seeking information about how the company was complying with the settlement.

Musk’s freewheeling commentary on Twitter, now X, and in interviews has injected volatility into Tesla’s share price and affected his other companies. In 2020, Tesla’s stock closed down more than 7% for the day after Musk tweeted, “Tesla stock price is too high imo.” Last year, major companies stopped advertising on X after he described an antisemitic post on X as “the actual truth.”

Investors have for decades pressed for independent directors, especially at public companies, because it allows them to push back against management and closely monitor what is happening inside the business.

The sweeping set of rules known as Sarbanes-Oxley in 2002 mandated that public companies have independent directors, including on the audit committee. The rules came after the collapse of energy trading giant Enron, which later was found to have hidden its financials amid improper board oversight.

Stock exchanges generally spell out how they define independence on boards and other expectations. At private companies, there are no requirements for the number of independent directors, or what constitutes one. At Nasdaq, if a company doesn’t comply with its majority independent board rule, it gives the company one year or until its next shareholder meeting to make a change; if not, it may be delisted.

Questions about a public director’s independence have gone to the courts, with judges sometimes finding problems with deep financial ties.

The Delaware Supreme Court in 2016 ruled that the majority of video game developer Zynga’s board weren’t independent. Among the reasons was that a venture-capital firm two directors worked for had invested in a startup the CEO’s wife co-founded and that another director and her husband co-owned a private plane with the CEO.

Following the court’s decision, Zynga expanded its board and formed a special litigation committee to investigate insider trading allegations. Zynga settled the suit in 2019 for $11 million.

“To me, it’s really: Are you capable of making a disinterested, objective decision uninfluenced by the relationship?” said Lawrence Hamermesh, former director of the Widener Institute of Delaware Corporate and Business Law, who has also served as senior special counsel in the SEC’s corporate finance division.

Surrounded by friends

When Tesla was looking to replace a departing director, it turned to a familiar face in JB Straubel. The board believed the company’s former chief technology officer, whom Tesla considers a co-founder, was someone Musk would listen to, could fill Ellison’s shoes and had technical expertise, according to people with knowledge of the board’s thinking.

Last year, ahead of a vote to approve Straubel, some shareholders pushed back over his close ties to the company, saying if he were added to the board then at least five of the eight members would lack independence. Straubel was elected anyway. A Nasdaq spokesman said it doesn’t comment on specific companies and referred a Journal question on how Straubel can be classified as an independent director to Tesla.

Musk has long surrounded himself with close friends as he built his business empire. He has turned to them for advice on new business ventures and on daily operational help.

In addition to Musk on the Tesla board, his brother, Kimbal Musk, is a member. He previously served on the SpaceX board and has counseled Musk on numerous ventures, including whether to start OpenAI and Neuralink. He and Musk are also close personally, often attending the same events and parties.

Ehrenpreis, who chairs two of four committees on the Tesla board, is designated independent by the company and has been close to Musk for years.

The venture capitalist held the right to buy the first Tesla Model 3—which some covet for bragging rights. Around Musk’s 46th birthday in 2017, he gave it to Musk, tweeting, “Much love and respect for everything you do.”

Ehrenpreis has personally or through his venture-capital firm, DBL Partners, invested in many of Musk’s ventures, totalling about $70 million.

On the Tesla board, he has made more than $220 million on stock sales earned through board service and has additional options worth more than $200 million at recent prices.

James Murdoch, former chief executive of 21st Century Fox, also is classified independent by Tesla. His friendship with Musk dates back to around 2006, and he has vacationed with Musk and their families, including on trips to Israel and Mexico.

In court testimony in 2022, Musk said he didn’t know Murdoch well, though Murdoch in an earlier deposition affirmed his friendship with Musk.

Murdoch, who is the younger son of Rupert Murdoch, chairman emeritus of News Corp, which owns The Wall Street Journal, has said in court testimony he considers himself independent and has described a director as “having an ability to exercise independence of thought in governance and oversight as a member of a public company.”

Murdoch poured $20 million into SpaceX, and a company controlled by him invested about $50 million in the space company, court records show.

Denholm, who is designated independent, is based in Australia and doesn’t socialise with Musk. She has said in court testimony she doesn’t have personal investments in Musk’s other companies.

Her decade-long position on the Tesla board has been lucrative, earning her more than $625 million in the company’s equity. Denholm has exercised about half her options, profiting more than $280 million from the sales.

Denholm runs Tesla board meetings as informal, family-style occasions. Directors sometimes ask softball questions of Musk, such as future Tesla product colours, according to people familiar with the board.

Musk, meanwhile, would sometimes arrive two hours late, or hours early, and then blame his staff for not getting him there at the appropriate time, according to one of the people.

Musk said he handpicked Denholm, who replaced him as board chair in 2018 under an agreement with the SEC, according to an interview on “60 Minutes” that year.

The idea Denholm would watch over him was “not realistic” given his status as the company’s largest shareholder, he said in the interview, adding: “I can just call for a shareholder vote and get anything done that I want.” Musk later tweeted that the show had edited the interview in a misleading way. A “60 Minutes” spokeswoman said the show stands by its reporting.

Gebbia, the Airbnb co-founder and friend of Musk’s, joined the Tesla board in 2022, lives in Texas and is designated an independent director.

Former Walgreens Boots Alliance executive Kathleen Wilson-Thompson, who joined the board in 2018, is designated independent and doesn’t have public ties to Musk.

Deal with ex-girlfriend

Three current and former Tesla and SpaceX board members have been among Musk’s closest personal and financial partners.

Ellison, the co-founder and current chief technology officer of Oracle, was designated independent during his board tenure at Tesla between 2018 and 2022. He has said “I’m very close friends” with Musk and has hosted him multiple times at his Hawaiian island, Lanai.

When Musk revealed his plans to buy Twitter, Ellison committed $1 billion in 2022, while still on the Tesla board, to help fund it, surpassing the investments of many of the venture-capital firms involved in the deal.

Gracias, whom Tesla classified as the company’s lead independent director from 2010 until 2019, has been close friends with Musk for more than two decades. Musk turned to Gracias for support after his baby son died in the early 2000s, according to a 2021 court deposition.

He is also one of the friends who attends private parties around the world and sometimes consumes illegal drugs with Musk.

In court testimony in 2022, he called Musk “extraordinary,” “an amazing engineer” and “a product genius.”

Former Tesla and current SpaceX board member Steve Jurvetson, shown in 2016, is among the directors who have used drugs with Musk, according to people who have witnessed it and others with knowledge of it. PHOTO: NIKKI RITCHER FOR THE WALL STREET JOURNAL

For his work on the Tesla board, he has made more than $100 million by selling shares he earned.

When Musk needed cash, Gracias lent him $1 million, Gracias said in a court deposition, though it is unclear when he gave the money or what it was for. Musk has also personally invested about $10 million in Gracias’s Valor Equity Partners.

When asked in a court deposition whether his close friendship and business relationships with Musk affected his ability to act as an independent director at Tesla, particularly related to Musk’s 2018 pay package, Gracias said it didn’t. “Otherwise, I wouldn’t have done it,” he said.

Gracias stepped down from the Tesla board after more than a decade in 2021 in response to the pressure to improve its corporate governance. He remains a SpaceX director.

Jurvetson is one of Musk’s closest friends, and the two have mixed friendship and business for years. Jurveston was an early investor in SpaceX, and the two have used LSD and ecstasy together.

Jurvetson, who is an amateur rocket enthusiast, often hosts Elon and Kimbal Musk for parties at his house at Half Moon Bay, a small beachside city south of San Francisco.

One episode, soon after the 2017 scandal that led to Musk and Jurvetson working to keep his Tesla board seat, shows the extreme intertwining of personal and business relationships around Musk.

Tesla’s general counsel at the time, Todd Maron—who had been a divorce lawyer for Musk—helped negotiate an understanding with one of Jurvetson’s ex-girlfriends, Keri Kukral, according to emails between the company and Kukral reviewed by the Journal.

As part of the 2018 arrangement, Kukral was given permission by Maron to review and approve public messaging, such as press releases, related to Jurvetson and his Tesla board seat, the emails show. After Maron left Tesla, his successor general counsel, Jonathan Chang, continued to communicate with her, the emails show.

In return, Kukral wrote a professional recommendation of Jurvetson to Tesla as he campaigned to keep his board seat.

It is highly unusual for a company’s general counsel to get involved in such personal matters of board members, or to give an outside person the power to review company messaging, corporate governance experts said.

Musk also tried to persuade board members to let Jurvetson vote while he was on a leave of absence, people familiar with the conversations said. Kimbal Musk, Murdoch and Denholm pushed back, the people said.

Jurvetson made more than $9 million selling Tesla shares received as a director before leaving the board in 2020, according to the documents reviewed by the Journal.

At least two former board members have bristled at the company’s lack of corporate governance and deference to Musk.

Former Tesla board member Linda Johnson Rice wasn’t close with Musk or other directors outside of work, although she sometimes saw fellow director Gracias at work events in Chicago, where they are both based.

She didn’t stand for re-election to the board in 2019 after serving less than two years over frustration with Musk’s volatile behaviour, including his drug use, the Journal reported. She informally asked whether the board should investigate and was brushed off.

“She served her term and that was it,” Musk tweeted about Rice, following the Journal’s January article about his drug use. “No negativity at all with Linda!”

Similarly, Hiromichi Mizuno, a former chief investment officer of Japan’s Government Pension Investment Fund, left the Tesla board in 2023 after three years in part because of the lack of ability he felt he had to work on improving the company’s governance-related practices. At issue was the board’s deference to Musk, who had different priorities for Tesla, according to people familiar with the board.

Mizuno found the board to operate more like a family company with fiefdoms, rather than a public company with stringent rules and regulations, even if it did usually perform well. He has made a practice of avoiding close relationships with others in the workplace to remain objective. While Mizuno was sometimes invited for a drink with Musk, he never attended his private parties or events, according to the people.

Musk has been recently pushing for even greater control over Tesla. He currently owns around 13% of the company.

In mid-January, before the Delaware court ruling on his pay package, he wrote in a post on X that he was uncomfortable transforming the electric vehicle giant into a leader in artificial intelligence and robotics without voting control over roughly 25% of the company.

“Unless that is the case, I would prefer to build products outside of Tesla,” Musk wrote.

The tweet was effectively an ultimatum for Tesla board members to revisit his compensation. The board so far hasn’t acted.

—Berber Jin, Lisa Schwartz and Jim Oberman contributed to this article.

A few years ago, Indonesia set out to turn its treasure trove of nickel into an electric-car manufacturing boom.

It imposed a sweeping ban on the export of raw nickel. That meant that companies wanting to tap the world’s largest source of the mineral—used in the most powerful type of EV batteries—would have to build smelters in Indonesia. Officials bet that factories to make EV batteries and entire electric cars would also follow, spawning end-to-end supply chains close to the mineral bounty.

The smelters came, and Indonesia’s nickel industry witnessed explosive growth. But powering it is a coal binge that is throwing off the country’s climate goals. And Indonesians are still waiting for EV makers to lay down production lines.

As President Joko Widodo prepares to leave office this year after a decade—the most he can serve—he is exhorting his potential successors to stick with the policy that is at the centre of his economic legacy. Indonesia holds presidential elections on Feb. 14, and a new leader will take charge in October.

Widodo has cast his plan, referred to in economist-speak as downstreaming, as the answer to the question of how Indonesia will become a rich nation. He says the country is reversing a 400-year pattern dating back to colonial times of being exploited for its natural resources and getting little in return. He has prodded other developing nations to follow its lead.

Last year, officials escorted delegations from mineral-rich Papua New Guinea and the Democratic Republic of Congo to one of Indonesia’s largest nickel industrial parks to show them the scale of Indonesia’s achievements. New Chinese-built smelters dot the archipelago. The value of Indonesia’s nickel exports is up four times since 2019 to around $33 billion.

Not everyone believes the silver metal is a silver bullet.

Nickel smelters have led to a surge in coal use, with new coal plants coming up at a time when the world is trying to phase out the fossil fuel. A January report by Climate Rights International, a U.S. environmental group, said that a single nickel-focused industrial park located on eastern Indonesia’s Maluku islands will burn more coal than Spain or Brazil when it is fully operational.

“We are sacrificing the environment and society, while at the same time getting limited profits for the country,” Muhaimin Iskandar, a vice-presidential candidate in the coming election, said during a televised debate with his political opponents.

Other candidates have pledged to carry forward the president’s nickel policies, including the front-runner for president, Prabowo Subianto, who has said it is much better to export electric-vehicle batteries than raw nickel.

The “dirty nickel” reputation is threatening the very economic opportunities Indonesia covets. In October, nine U.S. senators signed a letter opposing a proposed free-trade agreement to source critical minerals from Indonesia, citing environmental and safety concerns. Without a free-trade deal, EV batteries with substantial quantities of Indonesia-processed nickel won’t be eligible for a major U.S. tax credit.

That makes the country’s nickel less attractive to Western EV makers, who are already battling questions from green groups about the environmental fallout of the country’s sprawling nickel operations.

In a sign of the growing unease, a deputy director for batteries and critical materials at the U.S. Energy Department, Ashley Zumwalt-Forbes, voiced concern in a LinkedIn post last month about what she called the grip of dirty Indonesian nickel on the market. Indonesia accounts for half the global nickel supply, up from a quarter in 2018.

The problems with nickel are also pushing EV makers to rework car batteries and go nickel-free. A lithium-iron-phosphate alternative is gaining traction, though it remains less powerful than batteries containing nickel.

Then there is the question of whether the policy is taking Indonesia toward Widodo’s goal of downstreaming—that is, a shift to higher-value manufacturing. Widodo has long said the endgame isn’t localising nickel processing but rather attracting EV and battery factories. Anything less, he says, could put Indonesia on the same track as some commodity-rich Latin American economies that have languished.

But so far, EV makers haven’t rushed into Indonesia. Tesla, which Widodo has assiduously courted, including on a 2022 trip to Texas to meet with founder Elon Musk, hasn’t shown any signs it plans to set up a factory in the country. No other Western automakers have built EV factories either, though General Motors has a stake in one China-based automaker producing electric cars in Indonesia. Some, like Ford, have made deals to tie up nickel supply.

Korean automaker Hyundai has since 2021 operated one of Indonesia’s only EV factories, focused on the domestic market. The unit can produce 150,000 vehicles a year, but made fewer than 9,500 in 2022 and 2023. Hyundai and Korea’s LG expect to begin producing battery cells at a plant in West Java this year.

Automakers generally look to set up battery and EV plants in the markets where people are already buying electric cars. That puts Indonesia, where few consumers have switched from combustion-engine vehicles, at a disadvantage. The country has a limited charging network and gasoline is heavily subsidised.

Indonesian policymakers who believe the country’s nickel bounty gives it leverage over carmakers are mistaken, said Tom Lembong, a former trade minister under Widodo. He pointed to the growth of nickel-free batteries as a warning against betting big on nickel.

Lembong, who is advising presidential candidate Anies Baswedan—whose ticket advocates focusing on promoting labor-intensive industries—said Indonesia has made limited progress moving up the value chain.

“The irony about this is they call it downstreaming, but we’re still very upstream,” he said.

Septian Hario Seto, a senior Indonesian official involved in nickel policymaking, acknowledged that EV battery and car factories have been slower to come than nickel smelters. The government has brought new regulations to address that, he said, such as one that makes it easier for EV makers to import cars into Indonesia on the condition they later build a factory.

Last month, Chinese EV giant BYD said it would begin car sales in Indonesia, and break ground on a manufacturing unit later this year.

Overall, Seto said the nickel policy has been successful, boosting economic growth in less-developed eastern regions where the nickel is found, and providing jobs and tax revenue. The government has taken steps to limit environmental degradation, such as by banning companies from jettisoning mining waste into the ocean, and will try to bring hydropower projects online as an alternative to coal, he said.

Cullen Hendrix, a senior fellow at the Peterson Institute for International Economics in Washington, D.C., said there are two ways to assess Indonesia’s industrial policy.

“It’s been successful at driving foreign investment and building nickel processing capacity,” he said. “So far it hasn’t achieved the fully integrated mine-to-EV battery assembly to which it aspires.”

Sarah Tucker-Ray, a partner in McKinsey’s Washington, D.C., office, felt a lot of trepidation when she took a six-month parental leave in 2022.

“There is fear about, ‘Am I going to get written out of the story?’ ” says the 36-year-old Tucker-Ray, whose daughter, Viviana, was born in August 2022. “Is someone going to step in for me and take over? How will I come back?”

She addressed those fears in a reintegration plan that she drafted before going on leave. It included instructions for those who would be covering her workload while she was out, and it laid out what she wanted her job to look like when she returned. For example, Tucker-Ray didn’t want her role to change significantly, but she asked to not be given any internal projects—those focused on McKinsey’s own operations versus those of outside clients—during her first six months back. She also thought about small stuff, such as writing down all of her passwords, and she connected with other working mothers at the company who served as peer counsellors before she went on leave.

“They told me that the goal for week one is to get dressed, have breakfast with my baby, get into a suit without getting spilled on and get out the door,” she says. “It sounds so basic but I hadn’t had to do that yet.”

The days, weeks, and months after a new parent returns to work after leave can be a critical and challenging time for an employee. Many experience anxiety about how they are going to manage work and parenting, and some end up feeling like a failure at both.

To address that, some organisations have launched formal “reboarding” programs that structure those first months back after leave so they aren’t overwhelming for new parents, while also providing them with emotional support. McKinsey tested such a program in Europe and then expanded it globally

Many see it as a business imperative. Organisations are making substantial investments in paid maternity and paternity leave—in 2023, 40% of organisations in a Society for Human Resource Management survey offered paid maternity leave and 32% offered paid paternity leave—and they want to ensure new parents return to work and are productive and content when they do.

Tucker-Ray was happy to learn that McKinsey would cover the cost of her daughter and her husband to join her on a business trip. PHOTO: ELIZABETH FRANTZ FOR THE WALL STREET JOURNAL

Creating a plan

A successful reboarding program requires planning, and it and starts long before an employee goes on leave, consultants and HR leaders say. It begins with mapping out a comprehensive work-coverage plan, including if and under what circumstances the employee wants to be contacted about work while out on leave. The plan also should create clear expectations about what the return-to-work will look like, including the employee’s job description post-leave and even an explanation of what that first daunting day back might entail.

Many reboarding programs also connect new moms with experienced working parents or colleagues who have recently returned from parental leaves, as well as a coach (often an outside consultant) who can help set priorities and guidance on best practices.

When Maria del Mar Martinez became head of McKinsey’s diversity, equity and inclusion efforts in Europe in 2018, she learned that working moms left the management-consulting firm at nearly double the rate of their childless female peers with similar tenure. In exit interviews, women shared common grievances, including the challenge of balancing parenthood with a demanding job, a lack of support from their managers and few role models.

She heard similar sentiments in Asia and the U.S.

“That was a business problem,” says del Mar Martinez, now the global head of DEI at McKinsey. “I don’t want to lose those amazing women coming up the pipeline.”

To combat attrition, del Mar Martinez created a reboarding pilot program in Europe that included coaching employees before, during and after a parental leave. (Men are eligible to take part in the program if they have taken 12 weeks or more of leave.)

Built into the plan was a guarantee that new parents would have “meaningful work” upon their return, with the option of slowing down if that’s what they wanted, says del Mar Martinez. One issue, she and others say, is that managers often incorrectly assume that new mothers want lighter workloads or don’t want to travel, which is why it’s important for employees to spell out their preferences in a reboarding plan.

The McKinsey pilot required managers to confirm they understood their employee’s reintegration plan and to calibrate goals in performance reviews to ensure the person taking leave wouldn’t be penalised.

It worked. McKinsey closed the European attrition gap in 18 months, del Mar Martinez says, and later expanded the program globally.

The manager’s role

Other companies are increasing the support they offer to new parents, too, including Wall Street’s Morgan Stanley, which in 2019 appointed Allyson Bronner head of family advocacy at the company’s institutional division, a full-time position that focuses on supporting employees before, during and after parental leaves.

Bronner says one of the best ways to ensure a successful return experience for new parents is to include managers in the process.

To that end, she meets with an expecting employee’s manager between the 25th and 30th week of pregnancy to preview what the employee’s return-to-work will look like and discuss best practices for easing the transition.

“It’s important to set the scene and give them tools to manage their employees,” she says.

She says her next meeting with the manager occurs about a month before the employee is due back to discuss how the first month should be structured. She suggests the manager call the new parent two to three weeks ahead to preview what the first few days back will look like—namely, checking email and showing colleagues baby pictures.

The support continues throughout the first several months, with managers having weekly check-ins with the employee for the first six weeks and then monthly check-ins after that. Bronner encourages managers to ask new parents how they are doing and how their child care is going to determine whether they would benefit from more support or advice in that area.

Since Morgan Stanley created the family advocacy role, “it feels like there has been a culture shift,” Bronner says. “It’s hard to quantify in numbers, but culturally it feels like we’re moving in a more positive direction.”

A culture shift is also under way at chip-equipment maker ASML, which recently expanded the paid parental leave it offers and in May joined forces with employee-benefits firm Parentaly to create a support system for new parents.

ASML is in a male-dominated industry, says Karen Reinhardt, the firm’s chief human-resource officer in the U.S., so retaining women is critical to having a diverse workforce.

As of December, 82 employees had registered for the reboarding program, “more people than we expected,” Reinhardt says.

Among them is Meredith Polm Sheain of San Diego, a knowledge-management developer who went out on maternity leave in late August. In her reboarding plan, she made clear that she wanted to be notified while on leave about any bumps in a recently launched product. She also laid out her priorities for the first two months of her return.

“I felt so much better about the concept of returning to work once I gave my team this plan,” says Polm Sheain, who returned to work on Dec. 22. “I left them and myself in the best position I could.”

Reboarding isn’t the only new benefit companies are offering to make life easier for new parents.

McKinsey’s Tucker-Ray was asked to attend a partner conference in Atlanta about six weeks after returning from maternity leave. The firm covered the cost of her daughter and caregiver (her husband) to join her on the trip since she was still breast-feeding.

“I would have been torn about going away for nearly a week for an internal event but it became a nonevent,” she says. “It got rid of the barrier to feeling you can’t participate fully in parenting and be a leader.”

It’s an area already popular with the likes of Oprah Winfrey, Ellen DeGeneres, Prince Harry and Meghan Markle.

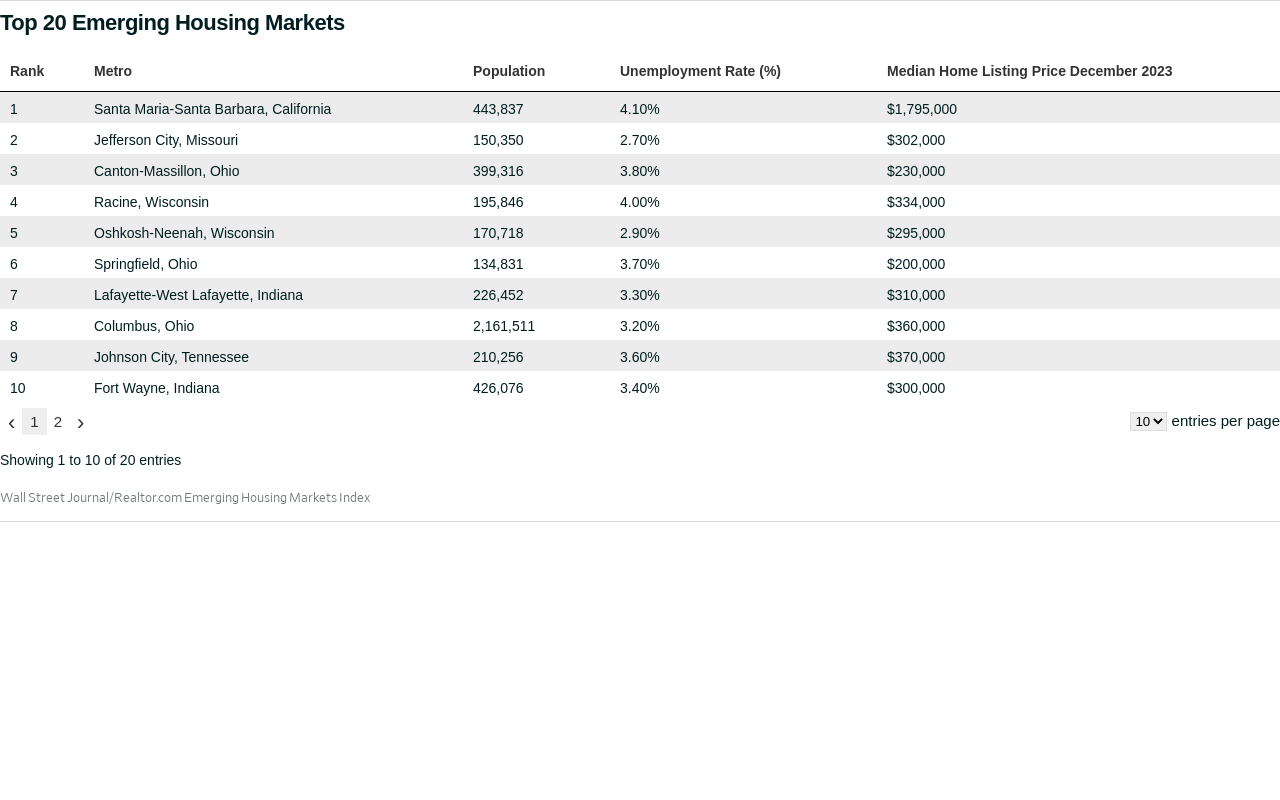

But now the affluent Santa Maria-Santa Barbara metropolitan area on the Central Coast of California nestled between the Santa Ynez Mountains and the Pacific Ocean has ranked as the top housing market in the latest Wall Street Journal/Realtor.com Emerging Housing Markets Index, released Wednesday.

It’s a surprise result for the quarterly index, which has, until now, typically seen more affordable cities rank at the top—Topeka, Kansas, took first place in the prior iteration of the report, released in fall, and Lafayette, Indiana, in the summer ranking.

“Santa Maria-Santa Barbara topping the list serves to highlight the division in today’s housing market,” said Danielle Hale, chief economist at Realtor.com. It’s the one and only West Coast market in the top 20, and, with a median listing price of $1.795 million in December, the highest-priced market by more than $1 million.

The top five cities in the index were rounded out by Jefferson City, Missouri, where the median listing price was $302,000 in December; the Canton-Massillon metro area in Ohio ($230,000); Racine, Wisconsin ($334,000); and the Oshkosh-Neenah metro area in Wisconsin ($295,000).

“Many housing markets cooled off after the pandemic’s run-up in prices and inventory-depleting demand,” Hale explained. “The markets that have continued to chug along, and even gain steam, are either priced low enough that buyers can compete, or priced high enough that the typical affordability constraints are not of concern to the market’s buyers.”

The latter is the scenario that’s playing out in Santa Barbara.

The index analyses key housing market data, as well as economic vitality and lifestyle metrics for the largest 300 metropolitan areas in the country to highlight emerging housing markets that offer a high quality of life and are expected to see future home price appreciation. It identifies markets that those considering a home purchase should add to their shortlist—whether the goal is to live in it or rent.

Santa Barbara “offers perhaps the finest lifestyle in the U.S.,” said local agent Luke Ebbin of The Ebbin Group at Compass. “Three-hundred days of sunshine and warm weather, a relaxed pace of living, proximity to uncrowded beaches, mountain hikes, fine food and wine, and incredible cultural offerings more often found in major metropolitan areas.”

However, with that median listing price of $1.79 million—more than four times the national median—the price tag attached to the idyllic locale is well out of range for many would-be buyers.

“Though Santa Barbara is among the highest-priced large housing markets in the U.S., buyers in the area have seen similar trends to buyers in other more affordable markets,” Hale said. “For-sale inventory fell rapidly during the early days of the pandemic, and has not recovered much as demand waned in the area and homeowners chose not to sell.”

As a result, “buyers hoping to snag a median-priced home are facing more competition, which has driven prices higher,” she said.

In December, 71% of homes on the market in the metro were priced at $1 million or higher, up from the same time in 2019, when the metric stood at 62%.

“Buyers who have been eager to purchase here and have been on the sidelines due to low inventory and high interest rates are entering the market as rates decline and more inventory becomes available,” Ebbin said. That “low inventory and high demand are keeping prices elevated.”

It should come as no surprise then that Santa Barbara boasts an affluent population who “are drawn to the area’s lifestyle, amenities and upscale housing options,” said Santa Barbara-based agent Jason Streatfeild of Douglas Elliman.

Santa Barbara has “long been a popular destination for retirees, especially those seeking a mild climate, beautiful scenery and a relaxed coastal lifestyle,” Streatfeild said, noting that many migrate from colder regions of the country, as well as from other parts of California.

Not only charmed by the balmy wealth, individuals from far and wide are equally wooed to the area by its thriving entrepreneurial community, and Santa Barbara’s “robust job market, including opportunities in technology, healthcare, finance and education, attracts professionals from various parts of the country,” Streatfeild said. “Some may relocate from major metropolitan areas like Los Angeles, San Francisco or New York in search of a more balanced and less crowded lifestyle.”

Indeed, out-of-towners appear to be driving demand in the coastal enclave, according to search data from Realtor.com. More than three-quarters (79.5%) of views to Santa Barbara home listings on the site came from outside of the metro in the fourth quarter, with a notable amount of attention coming from the Los Angeles (32.8%) area, according to the index. House hunters from Silicon Valley, Atlanta and New York City were also shopping in the area, according to Realtor.com data.

Meanwhile, Prince Harry and Megan Markle are prime examples that “Santa Barbara’s appeal extends beyond U.S. borders,” Streatfeild said.

The University of California, Santa Barbara, also attracts a global cohort—along with plenty of domestic new residents—who move to the area to pursue higher education.

The Santa Barbara metro area “attracted a sizeable 3.3% of its listing viewership from shoppers outside of the U.S.,” Hale said in the report. “Suggesting that international demand is applying pressure to already high prices.”

For comparison, “the average international viewership share across the 300 ranked markets was less than half (1.4%) the viewership share in Santa Barbara,” she added.

Europe’s economy stagnated in the final three months of last year, expanding a divide between a booming U.S. economy and a European continent that is increasingly left behind.

The fresh economic data showed higher borrowing costs had compounded the earlier impact of higher energy prices in the wake of Russia’s invasion of Ukraine.

By contrast, the U.S. economy has been expanding robustly and enjoyed its strongest performance relative to the eurozone since 2013—with the exception of the Covid-19 pandemic.

One factor that is threatening to weigh further on the European economy is its proximity to geopolitical flashpoints. Russia’s war on Ukraine sent energy prices rocketing in 2022, hitting European manufacturers. The U.S., as an energy producer, was comparatively unaffected, and its natural-gas industry even benefited when it became Europe’s energy supplier of last resort after Russia throttled gas deliveries to the region.

Now the crisis in the Middle East, which has gummed up cargo traffic through the Red Sea, is adding costs to European importers and disrupting European supply chains. There too, the U.S. hasn’t suffered as much since it has alternative routes for goods coming from Asia.

Europe’s Stoxx 600 index rose 12.64% last year, a little over half the performance of the S&P 500, which rose 24.23% over the same period.

The European Union’s statistics agency Tuesday said gross domestic product in the eurozone was unchanged in the final three months of last year. That followed a decline in the three months through September. During 2023 as a whole, Eurostat recorded growth of just 0.5%, while the U.S. economy expanded by 2.5%.

Still, the divergence between the giant economic blocs is more a story of surprising U.S. strength than unanticipated weakness in the eurozone. The U.S. grew much faster than economists had expected it would at the start of 2023, while the eurozone was about as badly hit by high energy prices and rising interest rates as had been expected. Economists forecast the growth gap will narrow somewhat in the course of the year.

Europe’s policymakers don’t expect the stagnation in output to extend deep into 2024. Instead, they see a pickup in activity as wages rise faster than prices, reversing the declines in real incomes that followed the war in Ukraine and a rise in energy and food bills.

“We have the conditions for recovery that are coming into place,” said European Central Bank President Christine Lagarde Thursday. “I’m not suggesting that it’s going to pick up radically, but it’s coming into place from what we see.”

Helping Europe is the fact that energy prices are falling from post-invasion highs faster than policymakers had expected. That should help boost household spending on other goods and services and lower costs for Europe’s hard-pressed factories.

With inflation easing, the ECB is expected to lower its key interest rate later this year, which would also jolt growth by easing the pressure on household spending and business investment.

Yet the eurozone faces fresh threats too, mainly from the conflict that began with the attack on Israel by Hamas on Oct. 7. Disruptions to shipping in the Red Sea have pushed freight costs sharply higher and led to delays for European manufacturers that rely on Asian suppliers for parts. A further escalation of the conflict could reverse the decline in energy costs and stall the anticipated recovery.

The International Monetary Fund now expects the eurozone to grow by 0.9% this year, a downgrade from its previous 1.2% growth estimate, according to the Fund’s quarterly World Economic Outlook report published on Tuesday. By contrast, it sees the U.S. growing by 2.1% against its earlier 1.5% forecast.

Strong U.S. growth and an estimated 4.6% increase in China’s GDP according to the IMF should more than offset Europe’s disappointing performance and translate into a soft landing for the world economy this year. The IMF now sees the world economy growing at 3.1% this year, the same rate as last year and faster than the 2.9% growth projected in October.

“We find that the global economy continues to display remarkable resilience,” Pierre-Olivier Gourinchas, IMF Chief Economist, told reporters, pointing to the speed at which inflation had receded as a positive surprise.

He warned, however, that geopolitical distortions could reignite price increases. Core inflation—which excludes volatile energy and food prices—isn’t quite back to the prepandemic trend, particularly for services sector prices, he said.

IMF economists also cautioned that financial markets have been overly optimistic in anticipating early rate cuts by central banks. They project policy interest rates to remain at current levels for the U.S. Federal Reserve, the European Central Bank, and the Bank of England until the second half of 2024, before gradually declining as inflation moves closer to targets. Some investors and analysts expect a Federal Reserve rate cut in the first half of this year.

Back in Europe, Tuesday’s GDP data showed Germany was the weakest of Europe’s large economies at the end of last year, with output falling in the final quarter. However, revised figures showed it avoided a contraction in the three months through September.

“The economy remains stuck in the twilight zone between recession and stagnation,” said Carsten Brzeski, an economist at ING Bank.

While Italy’s economy expanded slightly, the French economy flatlined for the second straight quarter. Ireland, which had been a major source of growth for the eurozone over the previous decade, saw its GDP fall by 1.9% in 2023 as a pandemic-driven boom in its key pharmaceutical industry ended.

In a rare bright spot, Spain finished the year with another strong quarter and matched the U.S. growth rate over 2023 as a whole, thanks to a surge in international tourism as the last of the Covid-19 restrictions were lifted.

The highest quality office buildings have had much better success navigating the industry’s turmoil. Now, even premier towers are starting to wobble.

Rents at the highest-end buildings have been falling, while the rate of leasing has been slowing. Tenants have become more sensitive to costs in a world of higher interest rates and lingering concerns about a possible economic slowdown, market participants say.

Owners of the most elite buildings escaped this fate for a while by convincing the market they had created a new class of office tower—one that surpassed the traditional Class A building at the top of the pecking order.

These landlords persuaded blue-chip tenants that reluctant workers would return if only their offices sparkled with lush roof decks, fully loaded gyms and food prepared by Michelin-starred chefs. Owners invested heavily in these properties, which were usually new developments with the best locations, views, air quality and modern designs.

But that strategy is losing steam as more companies have accepted the reality of hybrid work schedules and, for the most part, have given up on compelling workers to be in five days a week.

“The ship has sailed on full return to the office for most companies,” said Rob Sadow, chief executive of Scoop Technologies, a software firm that developed an index that tracks workplace strategies. “They’re not going to go from three days a week to five days a week by making their space nicer.”

That is one reason why few office developers are considering new ground breakings. Current rents don’t pencil out for building expensive space. The U.S. had only 31 million square feet in office construction starts last year, the lowest level since 2010. New buildings will represent only 1% of inventory by 2027, the lowest in at least 25 years, according to CoStar.

“New starts have essentially ground to a halt,” said Dylan Burzinski, analyst at real-estate analytics firm Green Street.

Premium, amenity-rich office space has outperformed in terms of rent and occupancy throughout the pandemic. In New York, SL Green Realty opened a new office tower called One Vanderbilt across the street from Grand Central Terminal in the fall of 2020. It boasted a 4,000-square-foot terrace and cafe and a menu overseen by star chef Daniel Boulud. The 93-story building quickly filled up even though its top asking rents were near record levels at more than $300 a square foot.

That sort of exceptionalism is beginning to wane. Asking rents for prime space in 16 U.S. markets declined in the third quarter after increasing on average from about $61 a square foot in mid-2021 to close to about $70 in the second quarter of last year, according to CBRE Econometric Advisors. They were just under $69 in the fourth quarter, CBRE said.

The share of leasing activity is also falling among the premier towers. The office properties that data firm CoStar Group defines as five-star buildings accounted for 8% of the market in 2022 and 2023, down from 10% in 2019. Meanwhile, new leases in five-star buildings were on average 43% smaller than 2019, CoStar said, reflecting how companies are becoming more efficient in their space use and tolerating some degree of work from home.

In the fourth quarter, 62% of companies offered some form of remote work, up from 51% one year ago, according to Scoop. On average, those companies with hybrid strategies required workers in the office 2.5 days a week in October, Scoop said. In 2021 and 2022, many companies still expected to bring workers back five days a week and were leasing space with that in mind.

Office buildings that have opened recently have done well, but not by One Vanderbilt’s standards. In Boston, for example, Millennium Partners has leased about 60% of the 812,000 square feet of office space that hit the market last year in the new Winthrop Center project with such tenants as Cambridge Associates and consulting giant McKinsey. But rents are about 10% less than what Millennium originally forecast, said Joe Larkin, principal of MP Boston, the developer’s local arm.

Larkin said that Millennium expects to achieve its goal of taking three years to lease the building. “What we lost in the last couple of years is the hope to exceed how we planned this building,” he said.

High interest rates and concerns about a possible recession are also giving companies second thoughts about trading up to higher quality spaces. Moves are expensive especially when borrowing costs are higher than they’ve been in decades.

Cost-conscious companies are noticing that the gap between asking rents in top buildings and lower quality buildings is widening. The result: Renewals were 42% of the leasing volume last year, compared with 31% in 2018 and 2019 combined, according to CBRE.

“If companies aren’t going to have people in the office full time, maybe taking the lower-grade space might be a better economic decision,” Sadow said.

Fans of The Crown will soon have the opportunity to own a piece of the royal drama as Bonhams is auctioning off a range of items from the Netflix series, which ended its six-season run in December.

More than 300 lots are currently available for online bidding through Feb. 8, and an additional 160 will go under the hammer during a live sale at Bonhams’ London headquarters on Feb. 7.

Since its debut in late 2016, The Crown has captivated viewers around the world with its visually stunning approach and dramatic portrayal of the British royal family’s tales of heartbreak. Throughout the show’s 60 episodes, viewers followed the twists and turns of the royals.

“The iconic costumes, props, and set pieces from The Crown are extensively researched and made with truly impressive attention to detail by master craftspeople,” Charlie Thomas, Bonhams U.K. group director for house sales and private and iconic collections, said in a statement. “Not only is this an incredible opportunity to own pieces from the landmark show, it is also the closest anyone can come to owning the real thing—be it the facade of 10 Downing Street or Princess Diana’s engagement ring.”

Highlights of the auction include recreations of Princess Diana’s iconic items, such as the sapphire engagement ring that actress Emma Corrin debuted as Diana in season 4 (presale estimate: £2,000 (US$2,537) to £3,000); the revenge dress actress Elizabeth Debicki wore as Diana during her split from then-Prince Charles in season 5 (estimate: £8,000 to £12,000); and the leopard swimsuit Debicki sported in season 6 while on vacation during Charles’ 50th birthday party for then-Camilla Parker Bowles (estimate: £800 to £1,000).

Expected to fetch the highest prices are a pair of life-size replicas from the set: the Gold State Coach, which is estimated to sell for between £30,000 and £50,000, and a facade of 10 Downing Street, the British prime minister’s office and residence (estimate: £20,000 to £30,000).

Described by Bonhams as a “rococo masterpiece,” the actual royal coach was built in 1762 for King George III and has been used at every coronation since 1831, when King William IV succeeded to the throne.

“We wanted to make something special, and Netflix had the money, ambition, and ability to go the whole hog. The Gold State Coach is fabulous,” said Andy Harries, CEO Left Bank Pictures and executive producer of The Crown, in the auction notes.

Gene D’Cruze, the series’ head of construction, said the items for sale are among the most impressive and accurate recreations ever committed to film.

“I’ve built every single set on every series—more than 1,000 of them—and employed 140 people. It’s all done old-school. I’ve done 80 TV series, but The Crown is the best—best production, best art department, best locations, best series, best people,” said D’Cruze in the auction notes. “I especially love the 10 Downing Street facade. Most sets only last six months, but this stood for seven years.”

Proceeds from the live auction will go toward establishing a new scholarship for students at the National Film and Television School (NTFS). According to the auction house, the program will support students at the globally renowned school over the next 20 years.

“The Crown’s huge global success has much to do with working with the best creative and production talent in this country and we want to invest the proceeds of this magnificent auction into the next generation of film and TV talent,” said Harries in a statement.

A special exhibition of items from the auction has been on a global tour—having already appeared in New York, Los Angeles, and Paris—and will remain on display at Bonhams London through Feb 5.

About the author: Desmond Lachman is a senior fellow at the American Enterprise Institute. He was previously a deputy director in the International Monetary Fund’s Policy Development and Review Department and the chief emerging market economic strategist at Salomon Smith Barney.

Today, a Hong Kong court ordered the liquidation of Evergrande, a Chinese company that was one of the world’s largest property developers. After years of fruitless negotiations between the company and its creditors over the restructuring of its $300 billion debt mountain, a Chinese court said that “enough was enough.” In a blow to an already troubled Chinese housing market, it ordered that the company’s assets be liquidated to pay back its creditors.

How mainland China handles Hong Kong’s court order could have major implications for Chinese property prices and foreign investor confidence. If it enforces the court’s order, that could see an acceleration in Chinese home-price declines by adding to supply in an already glutted market. It could also heighten social tensions by disappointing around 1.5 million Chinese households who have put down large deposits for homes that are yet to be completed.

If it ignores the Hong Kong court’s order, it risks dealing a further blow to waning investor confidence. Questions would arise about China’s willingness to abide by the rule of law and to offer a safe economic environment for investors.

The Evergrande liquidation comes at an awkward time for the Chinese economy. It is already in deep trouble and could be headed for a Japanese-style lost economic decade. The news also suggests that China will disappoint the consensus view that the Chinese economy is headed for only a minor economic slowdown this year. This could have major implications for the U.S. and world economic outlook, considering that China is the world’s second-largest economy and until recently was its main engine of economic growth.

Even before Evergrande’s liquidation order, a whole set of indicators suggested that the former Chinese economic growth model was dead. Chinese home prices have been falling for more than a year; both wholesale and consumer prices have been falling; stock prices have plummeted as foreign investors have taken fright; and youth unemployment has risen to around 20%.

There have also been questions about President Xi Jinping’s economic stewardship. First, his disastrous zero-tolerance Covid policy contributed to the country’s slowest economic growth in 30 years. Now his increased economic intervention is undermining the underpinnings of the Chinese economic growth miracle unleashed by Deng Xiaoping’s economic reforms in the 1980s.

Chinese stocks rose last week on news that authorities are taking steps to stimulate the economy. But anyone thinking that the Chinese economy will respond favorably to yet another round of policy stimulus has not been paying attention to the size of that country’s housing and credit market bubble that has now burst. Nor have they been paying attention to the troubling degree to which that country’s economy has become unbalanced.

According to Harvard’s Ken Rogoff, the Chinese property market now accounts for almost 30% of that country’s GDP. That is around 50% more than that in most developed economies. Meanwhile, over the past decade Chinese credit to its non financial private sector expanded by 100% of GDP, according to the Bank for International Settlements. That is a larger rate of credit expansion than that which preceded Japan’s lost economic decade in the 1990s and that which preceded the 2008 bursting of the U.S. subprime and housing market.

The overall Chinese economy is highly unbalanced in the sense that it has become overly reliant on investment demand. The Chinese investment-to-GDP ratio is over 40%, according to the Organization for Economic Cooperation and Development. That’s sharply higher than the more normal 25% ratio in most other developed and mid-sized emerging market economies.

The consensus forecast is that Chinese economic growth this year will continue at a 5% clip. Anyone relying on that forecast should reflect on the many failures by the U.S. Federal Reserve and other central bankers to foresee the grave problems of the subprime housing market in the U.S. in early 2008. It would seem that most economists are downplaying indications of major Chinese economic problems that are plain sight. Chinese economic problems could unleash serious deflationary forces for the U.S. and global economy. The Federal Reserve would be ignoring them at its peril.

Guest commentaries like this one are written by authors outside the Barron’s and MarketWatch newsroom. They reflect the perspective and opinions of the authors.

Leigh Thompson is the J. Jay Gerber Professor of Dispute Resolution and Organizations and a director of executive-education programs at Northwestern University’s Kellogg School of Management. She is the author of several books, including “Negotiating the Sweet Spot: The Art of Leaving Nothing on the Table.”

I’m an extrovert and I admit I’ve benefited from it.

Outgoing people are more likely to be noticed, selected as leaders and awarded “halo” traits—meaning that other people just assume extroverts are more likeable, intelligent and have other positive qualities. But as a social scientist, I can’t ignore the research: Most of these beliefs about extroverts simply aren’t true.

Studies show that introverts and extroverts are equally effective in academic and corporate environments, and that there is no actual relation between CEO charisma and firm performance.

Yet the misconceptions about extroverts persist, making them more likely to be chosen as leaders over their more introverted peers. That’s unfortunate because in our post pandemic world, replete with remote work, hybrid communication, far-flung team members, artificial intelligence and global disruption, introverts are particularly well-equipped to lead.

That may be hard to believe because of two persistent myths.

First is the widely held stereotype that effective leaders are gregarious, alpha and comfortable in the spotlight, even craving that attention. In reality, the social skills that extroverts display aren’t necessarily predictive of capable leadership.

Second is the belief that quieter people lack leadership skills. They are seen as less social, unassertive, sad and disconnected. Indeed, in a recent study in which people in different groups were instructed to “act like an extrovert” or “act like an introvert” regardless of their actual personalities, those who acted extroverted were disproportionately selected for leadership. And, interestingly, those who pretended to be introverted in that study reported feeling sad.

Both of these myths ignore the reality that introversion, far from being simply a lack of extroversion, is a distinct set of traits with its own large merits. This was true well before the pandemic, but the remote-work environment illuminated the bias even more and highlighted the need to change our perceptions.

Here are five reasons why introverts could be ideal leaders in the redefined workplace.

1.Remote-work performance. Extroverts’ job performance declined when the pandemic forced many businesses to go remote. A study of remote workers found that extroverted employees became less productive, less engaged and less satisfied with their jobs. A separate study found that team average extroversion had a large negative effective on team performance—that is, the more extroverted the team members were as a group, the worse they performed.

2. Dealing with adversity and change. Introverts show a greater capacity to engage, think through and make wise choices during periods of adversity and change. A recent investigation found that introverts had more positive attitudes toward AI and using AI overall than did extroverts. A separate study found that during periods of high conflict, extroverts develop fewer energising relationships with their teammates and aren’t viewed as proactively contributing to the team. Introverts, however, often possess a predisposition for things like empathy and thoughtful communication—all critical for navigating team dynamics and conflict in tough times.

3. Creativity. Introverts’ creativity flows well in the quiet aftermath of group interactions, positioning them as formidable leaders for innovative and reflective tasks. In studies of communication and conflict, introverts’ tendency to think before speaking was seen to yield more creative solutions.

4.Avoiding avoidance. Most humans approach positive things and avoid negative things. Sounds like a good policy—unless we’re talking about workplace challenges. Research has shown that extroverts commit more passive avoidance errors—that is, when the going gets tough, they tend to avoid the situation altogether; meanwhile introverts are more likely to inspect the half-empty glass or the disappointing customer-satisfaction data, generating insights and solutions.

5. Resilience against quitting. A study of over 200 people revealed a correlation between extroversion and burnout—that is, the more extroverted a person reported themselves to be, the more likely they were to burn out. Introversion, on the other hand, was uncorrelated with burnout, suggesting better immunity.