Global demand for electricity is set to grow at a faster rate over the next three years, but with record power generation from renewables and nuclear expected to cover the surge, emissions will likely go into structural decline, according to the International Energy Agency.

Electricity demand is on track to rise by an average of 3.4% a year through 2026, driven by robust growth in emerging economies, AI, cryptocurrencies and data centres, according to the Paris-based organization’s latest report. However, global carbon-dioxide emissions from power generation are expected to fall, as low-emission energy sources—wind, solar, hydro and nuclear, among others—are likely to account for almost half of the world’s electricity generation by 2026, up from just under 40% last year.

“It’s encouraging that the rapid growth of renewables and a steady expansion of nuclear power are together on course to match all the increase in global electricity demand over the next three years,” IEA’s executive director Fatih Birol said on Wednesday.

“This is largely thanks to the huge momentum behind renewables, with ever cheaper solar leading the way, and support from the important comeback of nuclear power, whose generation is set to reach a historic high by 2025.”

In 2023, global CO emissions from electricity generation increased by 1%, but the IEA predicts a fall of more than 2% this year and smaller decreases in the next two years. Generation from cleaner energy sources is expected to rise at twice the annual growth rate seen between 2018 and 2023, while coal-fired generation is forecast to fall by an average of 1.7% annually through 2026, the IEA said.

Rapid growth of renewables will be supported by nuclear power. According to the report, nuclear generation is set to rise by roughly 3% a year on average to the end of 2026, despite a number of countries phasing out nuclear power or closing plants early.

France and Japan will restart several plants while new reactors begin operating in Europe, China, India and Korea. Asia will likely remain the main driver of growth, reaching a 30% share of global nuclear generation in 2026, the IEA said.

For years, nuclear power has been at the centre of the clean-energy debate. Proponents including France argue that it is a reliable, low-carbon alternative to fossil fuels, while opponents such as Germany say costs and risks from reactor accidents and waste are too high.

At the United Nations’ COP28 climate summit last year, the U.S. and 21 other nations pledged to triple nuclear power capacity by the middle of the century.

Most of the increase in electricity demand forecast by the IEA is set to come from emerging markets. China is expected to be the largest contributor to growth—with consumption boosted by the production of solar PV modules, electric vehicles and the processing of raw materials—while India is forecast to grow the fastest among major economies.

Rapid expansion of artificial intelligence, data centres and cryptocurrencies will also be a driver of growth, according to the agency, which predicts their power demand could double to roughly the equivalent of electricity consumption in Japan.

Last year, electricity demand growth slowed to 2.2% from 2.4% in 2022, as advanced economies suffered the impact of high inflation and lower industrial output, the IEA said.

Demand in the U.S. decreased by 1.6% after rising 2.6% in 2022, mainly because milder weather reduced the use of heaters and coolers, but demand is expected to recover this year to 2026. European Union power demand declined for the second consecutive year in 2023—despite a fall in energy prices—and isn’t expected to return to high levels until 2026 at the earliest, the IEA said.

Parents have always supported their children into adulthood, from funding weddings to buying a home. Now the financial umbilical cord extends much later into adulthood.

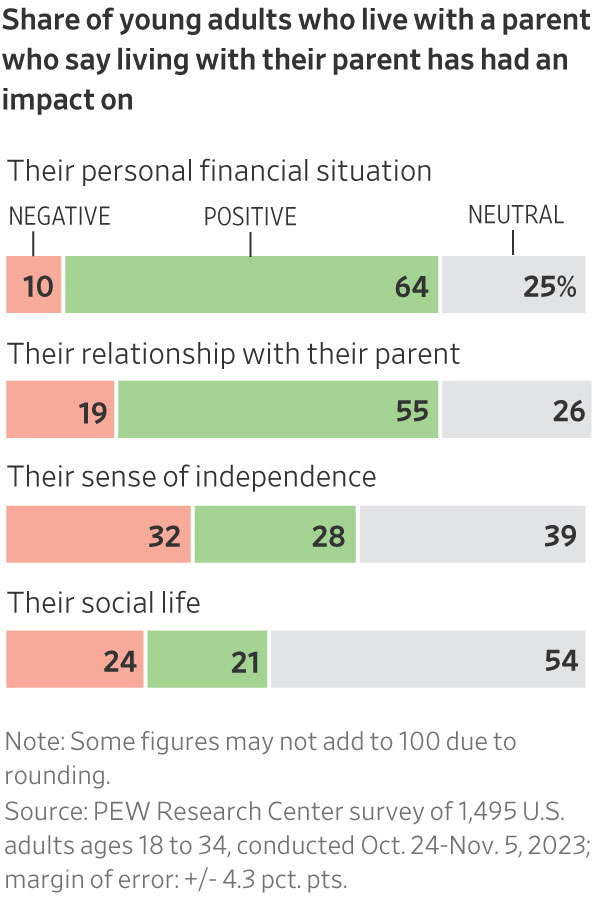

About 59% of parents said they helped their young adult children financially in the past year, according to a report released Thursday by the Pew Research Center that focused on adults under age 35. (This question hadn’t been asked in prior surveys.) More young adults are also living with their parents. Among adults under age 25, 57% live with their parents, up from 53% in 1993.

Parental support is continuing later in life because younger people now take longer to reach many adult milestones—and getting there is more expensive than it has been for past generations, economists and researchers said. There is also a larger wealth gap between older Americans and younger ones, giving some parents more means and reason to help. In short, adulthood no longer means moving off the parental payroll.

“That transition has gotten later and later, for a lot of different reasons. Now it’s age 25, 30, 35, 40,” said Sarah Behr, founder of Simplify Financial Planning in San Francisco.

Kami Loukipoudis, a 39-year-old director of design, and husband Adam Stojanik, a 39-year-old high-school teacher, knew they would need parental assistance to buy in New York’s expensive home market.

“We could pay a mortgage, but that down payment was the absolute crusher,” Stojanik said. “The idea of trying to save up on our own—as long as we were paying rents in NY, would’ve taken 300 years.”

Loukipoudis’s mother gave them the money for a 10% down payment on a two-bedroom apartment in the New York borough of Queens.

The young-adult allowance

Adult children aren’t necessarily getting larger checks from their parents, but they are staying on the parental payroll for longer than previous generations, according to Marla Ripoll, professor of economics at the University of Pittsburgh who studied the trend by analysing payments from parents to adult children over a 20-year span.

Ripoll found that 14% of adult children receive a transfer of money from their parents at least once in any given year, and roughly half get financial help at some point within that period. Those rates have been stable for years. What has changed is that the transfers now continue for much longer, she found. This longer-term help might be a drag on social mobility, as it becomes even harder for young people from lower-income families to catch up, researchers said.

Of the young adult children who said they received financial help from a parent in the past year, most said they put it toward day-to-day household expenses, such as phone bills and subscriptions to streaming services like Netflix, according to the Pew survey.

The amount of money and the frequency of help varies by age; those on the older end of the 18-to-34 cohort are far likelier to say they are completely financially independent from their parents compared with younger adult children, as many in the latter group are completing their education. Nearly a third of young adult children between the ages of 30 and 34 say they still get parental help.

Heather McAfee, a 33-year-old physical therapist in Austin, Texas, said she lived at home between 2019 and 2021; otherwise she wouldn’t have been able to make progress paying down her student loans while rent prices in her area remained so high. The plan worked—she has since reduced her student-debt balance from $83,000 to $15,000.

“It helped tremendously,” she said. “I didn’t have to take out more loans to pay for apartment living or anything like that. That stress was gone.”

Setting limits on financial help

A little more than half of parents surveyed said that having their adult children home brought them closer together or improved their relationship, but nearly 20% said it dented their personal finances.

Financial advisers often find themselves in the tricky position of speaking to both ends of the equation: adult children who need assistance and the parents determined to help children well into middle age, within limits.

Whereas previous generations would step into a greater sense of financial independence in their early 20s, young adult children today are often unable to reach similar markers of such independence—living on their own or buying their first home, for example—without greater financial resources.

Families typically don’t set concrete rules around when financial help will happen and what the money is used for, which can result in surprises down the road, Behr said.

In one case, Behr’s clients received the down payment they needed to purchase a condo from a generous mother-in-law. Years later, that same mother-in-law told them she expected a payout once the couple sold the home.

The hand-me-down payment

Down-payment help from parents—a given for many first-time home buyers—is growing thanks to higher home prices and elevated mortgage rates.

About a fifth of first-time home buyers said they got help from a relative or friend when pulling together the money needed for a down payment, according to a 2023 survey of home buyers and sellers from the National Association of Realtors. And 38% of home buyers under age 30 received help with the down payment from their parents, according to a survey this spring by Redfin.

Wealthy families often go further than helping with the down payment. They become a true bank of mom and dad and write a mortgage. The Internal Revenue Service sets minimum levels of interest for such loans, which remain significantly cheaper than current mortgage rates.

Timothy Burke, chief executive at National Family Mortgage, which facilitates such loans, said parents are often frustrated on behalf of their house-hunting children. High interest rates and the cutthroat housing market are holding their children back from reaching a milestone the parents themselves were more easily able to access.

Mei Chao, a 41-year-old stay-at-home mom, and her husband, William Chao, a 44-year-old information-technology specialist, bought their first house as a couple in 2017. They relied on financial help from her husband’s two sisters and his mother to help them bridge a gap in their house-buying timeline. While they waited to sell William’s Manhattan condo, they used the money from the family to purchase the new house in Queens.

The structure of the agreements got tricky. After selling the condo in Manhattan, Mei and her husband were able to repay his sisters in full. But they didn’t have enough money left over from the sale to do the same for Mei’s mother-in-law. So they kept the mother-in-law’s name on the deed to the house—a concession Mei said they were both more than happy to make.

“Ultimately, it all worked out. I’m glad his mother pushed us,” Mei said. “Without her help, I could not say we would have this home.”

The fastest cars you can buy are all electric. Cars with zero-to-60 times under two seconds are the Rimac Nevera and its close relative the Pininfarina Battista, the Tesla Model S Plaid Edition, and the Lucid Air Sapphire.

Now, add one more: the British-made McMurtry Spéirling. At a Silverstone track event in December, Mat Watson of the YouTube channel Carwows drove the electric, rear-wheel drive Spéirling PURE model to 60 miles an hour in 1.4 seconds, with zero to 100 in 2.63 and a quarter mile in 7.97. The PURE is a racer in an edition of 100, but McMurtry said it will eventually be producing a street-legal version.

The price in the U.K. for the handmade PURE is £895,000, and in the U.S. around US$1 million. McMurtry Automotive was founded in 2016 and based in England’s posh Cotswolds region of Gloucestershire. Managing Director Thomas Yates comes from Formula 1, and the company’s focus is on race-bred technology. Testing, in secret, occurred in the U.K. at tracks such as Castle Combe and Donington Park. The first reveal to the public was at the Goodwood Festival of Speed in 2021, with racers Derek Bell and Alex Summers giving demonstration runs. The next year, the PURE set a hill climb record at Goodwood (going up in 39.08 seconds).

Miller Motorcars of Greenwich, Connecticut, which also handles Ferrari, Bugatti, Maserati, Rolls-Royce, and other luxury brands, announced it was taking on McMurtry in January. The record-breaking car was shown by its battery supplier at CES in Las Vegas earlier this month, but will also be making an appearance in Greenwich, with an open house Feb. 3. The West Coast dealer is O’Gara Motorsport, and the star car was in California at Thermal Raceway earlier this month for a demonstration.

The record-setting McMurtry Spéirling PURE on display at CES this year. Jim Motavalli

Evan Cygler, director of special projects at Miller, tells Penta he was “completely dumbfounded” to encounter the rear-wheel drive McMurtry PURE in England. “They purposely came out with a finished car at Goodwood to break a record, and achieved the goal,” Cygler says. “The sound of it is incredible, as is the tiny size. We are passionate about our business, so we told them that if there was an opportunity to sell these cars, we’d love to be involved.”

Miller will support these track-only cars with its own track days at Connecticut’s Lime Rock Park, Cygler says. “It is less than two hours away and a fun place to host our customers for a day,” he says. “The Spéirling PURE is a cool weekend racer, and definitely something different. Whether you are into EV products or not, you have to love this.” Miller expects to get one or two PURE cars in 2025, he added. McMurtry will also host customers at private track events in the U.K.

The Spéirling reportedly offers 1,000 horsepower and 1,033 pound-feet of torque from two electric motors. Keeping it on the track are a pair of huge turbines (adapted from Formula 1 and Can Am) located behind the single occupant that extract air from under the car and produce more than 4,000 pounds of downforce. The battery is relatively small at 60 kilowatt-hours, but the carbon fiber-bodied car is so light at approximately 2,200 pounds that it has an estimated 300 miles of range (driven lightly, and on the forgiving European WLTP cycle). Top speed is around 200 mph.

The battery pack in the PURE prototype uses Molicel cells that can fast charge in 20 minutes, with rapid cell cooling. A charge can get the car around Silverstone track for 10 laps. Customer cars will use next-generation cells that are still in development.

The cockpit of the Spéirling PURE is a tight fit, and entry is made easier by a removable steering wheel. The single occupant sits on the rear fender and swings his or her body through the narrow opening, then drops into place. It’s a racer’s view forward, with no infotainment or anything else extraneous to ultra-high-speed driving. The Spéirling PURE may not be useful for getting groceries, but it offers the ultimate acceleration experience.

China’s real-estate crisis has dragged down the economy, caused massive layoffs and pushed multibillion-dollar companies to the point of collapse.

Economists think it is about to get worse.

Sales of newly built homes in China fell 6% last year, returning to a level not seen since 2016, according to China’s statistics bureau. Secondhand home prices in its four wealthiest cities—Beijing, Shanghai, Guangzhou and Shenzhen—declined by between 11% and 14% in December from the year before, according to the broker Centaline Property.

Developers are starting fewer projects. Homeowners are paying back their mortgages early and borrowing less. Once-thriving property companies are stuck in protracted negotiations with foreign investors, following defaults on about $125 billion of overseas bonds between 2020 and late 2023, according to figures from S&P Global Ratings.

Chinese developers and local governments are so desperate to attract home buyers that some have resorted to bizarre marketing strategies.

A property company in Tianjin ran a video advertisement featuring the slogan “buy a house, get a wife for free.” It was a play on words, using the same Chinese characters as the phrase “buy a house, and give it to your wife”—but presented in a sentence structure typically used to offer freebies for home buyers. In September, the company was fined $4,184 for the ad.

A residential compound in eastern China’s Zhejiang province promised last year to give home buyers a 10-gram gold bar.

Earlier this month, Sheng Songcheng, former head of the statistics department at the People’s Bank of China, told a local conference that the housing downturn would last another two years. He thinks new-home sales will fall more than 5% in both 2024 and 2025.

Wall Street economists are also ringing alarm bells about how long the real-estate slump will last.

“Not too many people are buying, can buy or want to buy,” said Raymond Yeung, chief China economist at ANZ. He said there had been a fundamental shift in the way Chinese people view the property sector, with housing no longer seen as a safe investment.

China’s real-estate sector and related industries once accounted for around a quarter of gross domestic product and the sector’s slump has been a significant drag on the world’s second-largest economy. That has increased calls for Beijing to do more to prop up the sector, but so far Chinese officials have stuck to piecemeal policies rather than introducing a landmark stimulus package.

A number of economists are making comparisons to Japan, which spent decades trying to rebound from a crash in real-estate and stock prices. China’s stock market is in a years-long slump.

China’s central bank can help make the situation less painful, but it will need to be aggressive, said Li-gang Liu, head of Asia Pacific economic analysis at Citi Global Wealth Investments. The central bank still has policy room and could take one big step to make a significant impact, he said.

Liu Yuan, head of property research at Centaline, said that without the government’s help, new-home prices will need to drop by another 50% from current levels before they reach a bottom. This is based on the assumption that the tipping point will only come when it is cheaper to buy than to rent houses, Liu said.

China’s real-estate downturn has claimed dozens of victims. More than 50 developers—mostly privately owned—have defaulted on their debt. Developers still have millions of unfinished homes that were sold but not delivered. Chinese authorities have set aside billions of dollars to help builders complete apartments but the logjam is growing.

The crisis has drained the coffers of some Chinese local governments, which previously relied on land sales as a main source of income. Economists estimate they have hidden debt worth anything from $400 billion to more than $800 billion. To quiet talk of potential defaults, the central government has set up debt-swap programs to help some of them refinance.

Some economists are optimistic. In the first half of this year, buyers of secondhand homes will gradually return to the new-home market and prop up the sector, said Helen Qiao, chief China economist at Bank of America. “Things will slowly get better from here,” Qiao said.

But most are still expecting more pain, and investors are bearish. A benchmark of Hong Kong-listed property stocks had fallen for four years in a row before the start of this year. Since Jan. 1, it is down another 15%.

A 23-year-old Sacramento, Calif., woman was arrested after allegedly stealing nearly $2,500 worth of Stanley cups from a retail store, local police said. The woman allegedly filled her shopping cart with Stanley Quenchers—the insulated cups that have thrown social-media into a frenzy in recent months—and left without paying.

When police tracked her down, they found her car filled with 65 of the cups, according to Lt. Chris Ciampa of the Roseville Police Department. She was arrested on charges of grand theft and driving under the influence, Ciampa said.

The arrest was the latest episode in the viral craze over the water bottles. The stainless-steel tumblers—the popular, 40-ounce version of which sells for $45—have become a status symbol for many women and teens, sparking chaos at retailers and launching a resale market where certain colours sell for more than $200 apiece. The hashtag #stanleytumbler has more than a billion views on TikTok and has been used more than 180,000 times on Instagram.

Stanley, which has been in business for more than a century, has long been a popular brand for hikers, teachers and construction workers. But as the Quencher’s popularity skyrocketed in recent years, its maker capitalised on the new demand with collaborations and a wider, pastel-driven colour palette.

“We were a brand that was a $70 million brand that appealed to guys with a green bottle that was 107 years old and is one of the greatest products in history,” Stanley’s president, Terence Reilly, said in an interview earlier this month. He added: “There was a big opportunity to reposition the brand and appeal to new consumers. And that’s just what we set out to do in 2020.”

In 2022, the company said there was a 150,000-person long wait list for the Quencher and sales had more than tripled from the prior year.

The cups have sparked a collectors’ craze, with devotees amassing dozens of colours and fighting over limited-edition releases. Ahead of one such release, for the Starbucks x Stanley pink Quencher, shoppers camped overnight outside Target locations to ensure they got a cup. The products sold out in minutes at some stores, and a viral video of frenzied shoppers rushing a display in one location sparked consternation online.

Those limited-edition pink cups, which are currently not available on Target or Stanley’s website, are now retailing for hundreds of dollars on resale sites like eBay and StockX.

Ciampa, the police lieutenant, said he believes the woman likely intended to resell online the 65 cups that were in her car. The department warned any potential thieves against repeating her behaviour.

“While Stanley Quenchers are all the rage, we strongly advise against turning to crime to fulfil your hydration habits,” it said in a statement.

Hundreds of businesses have volunteered to measure and report their impact on the natural world, as they recognise the growing risks to their own operations from environmental degradation, including a denuded Amazon rainforest and dying coral reefs.

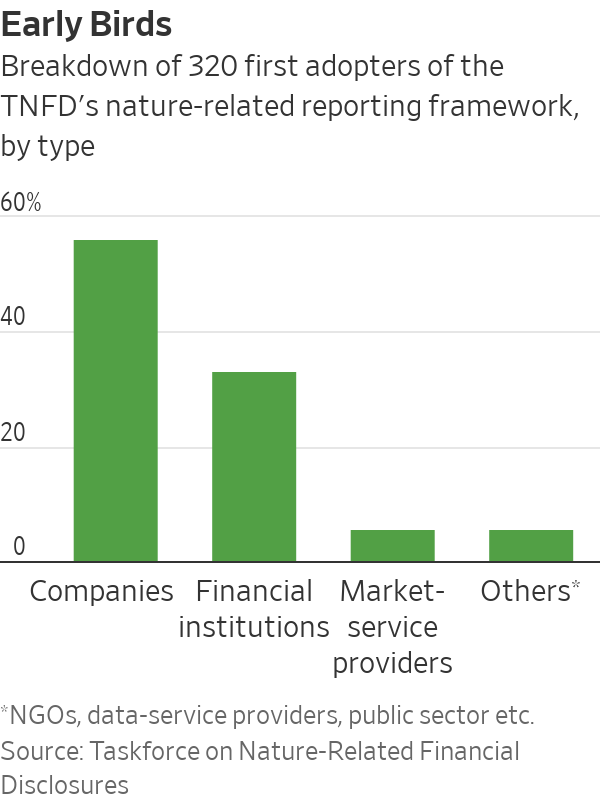

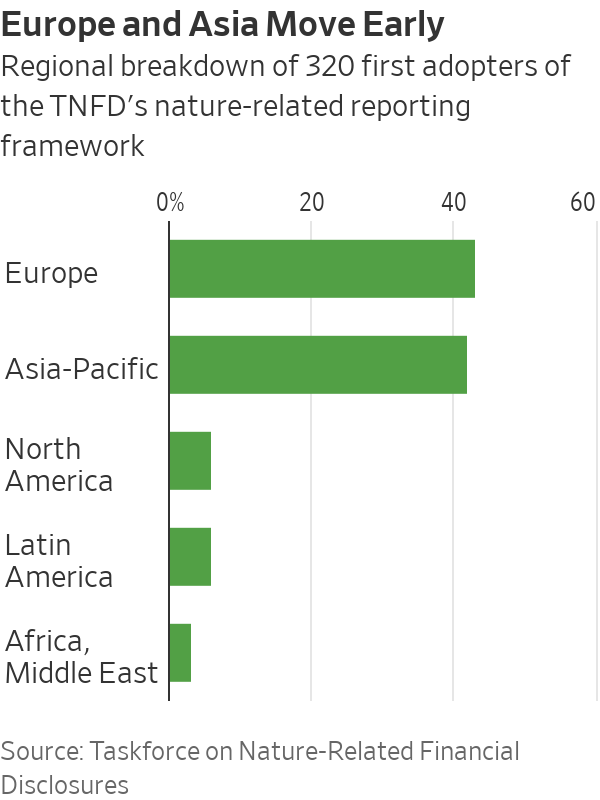

While many businesses are struggling to meet coming requirements to report their climate impact, more than 300 banks and companies are pledging to go much further. Early movers from across sectors and countries have promised to regularly publish nature-impact information as set out by the Taskforce on Nature-Related Financial Disclosures, or TNFD, a United Nations-backed initiative.

The first adopters represent $4 trillion in market capitalisation and around $14 trillion in assets under management. They include seven of the world’s 29 globally systemic banks, Japanese investor SoftBank, Norway’s sovereign-wealth fund, Gucci parent Kering, miner Anglo American and pharmaceutical majors GSK, AstraZeneca and Novo Nordisk.

Take-up by sector leaders should encourage peers to accelerate their efforts, said Tony Goldner, executive director of the TNFD. The framework is aligned to the Kunming-Montreal Global Biodiversity Framework agreed to in 2022 by nearly 200 countries. It recommends disclosures in governance, strategy, risk and impact management, as well as sector-specific metrics and targets for reducing impact.

Biodiversity impact is both a new type of risk and a new opportunity, said Valentin Alfaya, sustainability director at Spanish-listed infrastructure group Ferrovial, one of the first movers. “As a consequence of the implementation of the TNFD and our own natural capital assessment program, sometimes investments are going to be left aside,” Alfaya said.

“When you are interacting with those protected areas that are very relevant in terms of ecological value…it’s really risky for the company, not just in terms of reputation but also in terms of operations and even finance,” he said.

Using the framework will guide investment and help integrate nature into financial decision making, said Marisa Drew, chief sustainability officer at lender Standard Chartered. The move is a “significant opportunity for us to facilitate financial flows toward nature-positive outcomes,” Drew said.

Gauging impact is central to business decisions and managing risk, said Jennifer Motles, chief sustainability officer at tobacco giant Philip Morris International. “The TNFD recommendations and guidance will support us as we continue to focus on nature-related dependencies, impacts, risks, and opportunities,” Motles said.

The ramp-up in disclosure comes amid heightened awareness of the threat posed to the world by such natural degradation. The top four medium-term risks are all environmental, according to the World Economic Forum’s global risk report published earlier this month. They include extreme weather events, critical changes to the Earth’s systems, a collapse of the ecosystem and natural-resource shortages. “The collective ability to adapt to these impacts may be overwhelmed,” the report warns.

The World Bank estimates that the global economy could lose $2.7 trillion by 2030—which would mean a 10% drop, on average, in the economic output produced across all nations—if certain at-risk ecosystems collapse, such as fisheries or pollination by bees.

Adoption of the TNFD is “a clear signal that investors, lenders, insurers and companies are recognising that their business models and portfolios are highly dependent on both nature and climate,” the taskforce’s co-chair, David Craig, said. Natural risk should be treated both as a strategic risk and an investment opportunity, Craig said.

But reporting the damage done to the natural world isn’t the same as stopping it, said John Tobin-de la Puente, a professor of corporate sustainability at Cornell University. Disclosure is less about encouraging companies to change than it is about giving investors clear information on risk, he said.

Unlike carbon emissions, which can be assessed in terms of metric tons, there isn’t consensus on how to gauge environmental impact—whether, for example, in terms of protected species, general biodiversity, or a bundle of measures, said Tobin, a tropical ecologist and corporate lawyer by training. Some efforts have been made to create units of ecosystem impact, but for now, no universal metric exists, he said.

Alternatives to current business models will also need to be created, just as renewable energy has been developed to replace fossil fuels, Tobin said. “Will we get there at some point soon, before it’s too late for the biosphere?” he asked. “That question is still open.”

If Kelli and Fei Wang’s house had a soul, it would be the walk-in closet.

The house, in Chicago’s Ukrainian Village neighbourhood, is designed around the couple’s love for fashion and includes a 300-square-foot custom closet, with charcoal-suede wall covering and cerused-oak shelves, amplified by a vanity within a 40 x 60 inch mirror. There is a separate accessories side room, modelled after a showroom, where Kelli’s collection of designer bags and shoes sit on shelves and where she hangs out on a silver love seat.

In the couple’s previous home in Chicago’s Lincoln Park, they had to change out their wardrobes every season, hauling clothes from their apartment to their storage unit in the building’s basement, because there wasn’t room for it all upstairs.

“I wanted to never do a closet swap again,” says Kelli, 42, dressed in a floaty, cream-coloured shirt dress from Sandro Paris and light pink Manolo Blahnik pumps. “The closet was the first thing I thought about for the house.”

The Wangs bought their Ukrainian Village property for $511,000 in 2016 and tore down the existing 2,500-square-foot, three-bedroom, old brick home on it. The new house, finished in 2021, is 5,000 square feet, has three bedrooms and cost $1.8 million, with about $100,000 of millwork, carpet and furnishings going into the primary closet alone.

To design the house, the couple hired Dan Mazzarini, the principal of New York-based BHDM Design, who was a director of store design at Ralph Lauren for six years and also worked on Michael Kors, Calvin Klein and Kate Spade retail spaces.

Mazzarini knew Kelli from college, and understood the couple’s love for fashion: they’d shopped together many times in New York, where Fei had a special affinity for the Ralph Lauren store on Madison Avenue.

“I wanted to live in the Ralph Lauren store,” says Fei, 46, dressed in a custom-made Pini Parma shirt and a Boggi sweater. “It makes you feel elegant, elevated, and classy.”

As a guide for the house’s overall aesthetic, they decided on “Ralph Lauren meets Tom Ford, a mixture of buttoned up and timeless sophistication and sexy, modern, crisp elegance,” says Mazzarini. That meant a lot of black, white and charcoal.

That mixture can be seen throughout the house. In the living room, open from the kitchen on the main floor, a Ralph Lauren influence can be seen in the classic white sofa, while the angles of the coffee table and the chairs are more Tom Ford, says Mazzarini.

Tom Ford comes out in the kitchen, where the black granite counters, black-matte open shelves and stainless-steel appliances have a “refined industrialism,” says Mazzarini. The dining room has a crafty Ralph Lauren chandelier and white leather chairs.

On the second floor, Fei’s office is “menswear-oriented” It has a modern, crisp, geometric style, with a glass coffee table, an oversize black linen sofa, and dark grey flannel curtains, like a suit, says Mazzarini. The red fox fur and brown velvet pillows, the rosewood desk and the nubby rug add more classic textures.

The primary suite, with its bathroom and the centrepiece closet, takes up the entire third floor. It is designed in part after the Bulgari Hotel Milano, where the couple stayed on one of their first trips to Italy. The furnishings include grey-velvet drapes, an ebony headboard, a leather bench and a large brown-velvet armchair.

When designing the closet, Mazzarini says he asked the couple how many suits, shoes, bags and accessories they had—and that number kept growing as the home-building process progressed, going from around 50 to more than 100 pairs of shoes for each. While the overarching goal was beauty and style, it also had to be comfortable—and to reflect what Mazzarini calls the couple’s “Midwestern warmth and hospitality.”

Fei was born in Shanghai and grew up in Chicago, where his father was getting a Ph.D. in chemistry. Living on a teacher assistant’s budget didn’t leave much for buying designer clothes, but Fei says he “always had an eye for fashion—it was innate.” He says his parents, who grew up when many Chinese people wore blue worker’s suits, weren’t interested in subsidising his passion, so he started working in a clothing store when he was 14 years old. The first suit he bought himself was from Banana Republic.

He graduated from Illinois State University in 1999 and then from the University of Chicago with an M.B.A. in 2004. He went to work in asset management at Morgan Stanley, then to J.P. Morgan Asset Management and UBS before landing again at Morgan Stanley in 2021, where he is now a senior vice president in family wealth management.

Kelli also remembers a passion for fashion from a young age. Growing up in Piqua, Ohio, north of Dayton, she couldn’t afford to buy designer clothes, so she mixed and matched, she says. She graduated from Miami University in Oxford, Ohio, and went to work at J.P. Morgan Asset Management before moving on to Merrill Lynch and Centric Wealth Management in 2018, where she is currently director of financial planning.

Fashion is central to the couple’s relationship. When they first met in 2008, when they were both working in J.P. Morgan’s wealth management unit in Chicago, each noticed the other’s clothes. “She was chic and classy,” says Fei. “I pay attention to style.” Kelli remembers the first time she saw her now-husband walk by in a suit. “He looked the Wall Street-financier part,” she says.

After their wedding in Lake Como, Italy, the couple honeymooned at JK Place (now called The Place), in Florence, a hotel that also influenced the design of their home. They started traveling to Italy and France every year because they love traveling and shopping together, and they both appreciate the goal of having the best experience possible, whether it is food, art, clothing or design. “The downside of that is there’s no voice of reason,” jokes Fei.

The Wangs say they have passed their fashion appreciation on to their 2½-year-old daughter, Gemma, who loves to hang out in the accessory room of the closet, where she tries on her mom’s shoes. In Gemma’s own bedroom, a shelf is filled with miniature designer bags: Gucci, Chanel, Prada, Louis Vuitton. “She has a better sense of style than both of us,” says Kelli.

Wall Street entered 2024 betting the year would go perfectly, but an up-and-down start for stocks and bonds suggests the going won’t be easy.

Stocks have climbed to records, driven by cooling inflation that has spurred investors to anticipate as many as six interest-rate cuts. Falling rates often boost share prices by reducing the relative appeal of bonds and making it cheaper for companies and consumers to borrow, lifting corporate profits.

But despite Friday’s record close in the S&P 500, the rally in major indexes has stalled in recent weeks—the benchmark index is up less than 2% from where it was a month ago—while the labour market and economy show few signs of slowing. Bond yields have ticked up in the new year after falling sharply at the end of 2023.

This dynamic is prompting some analysts and portfolio managers to warn that further stock gains might be halting because the rate cuts that are widely expected to power the market higher might not arrive as quickly as bullish investors had wagered.

“Clearly, the consensus is that inflation is under control and we’re heading for a soft landing,” said Doug Fincher, a portfolio manager at New York City-based hedge fund Ionic Capital Management. “It’s certainly possible—but a lot of that is priced in.”

The S&P 500 is up 1.5% this year, but analysts see more signs of caution under the hood.

Investors have retreated this year from shares of banks, smaller companies and real-estate firms that posted big gains during the fourth-quarter rally, which was kicked off by investor belief that the Federal Reserve had pivoted in November to a rate-cutting stance. Bond yields, which rise when prices fall, have climbed as traders have pared back bets that Fed officials will start cutting rates in March.

There is a greater than 50% chance the central bank keeps rates where they are at its March meeting, according to the CME FedWatch tool. At the start of the year, traders expected rates to end December around 3.85%. Now they expect closer to 4.1%, per futures contracts tied to the fed-funds rate.

Behind those moves: data showing persistent economic strength that could lift inflation. Treasury yields, a benchmark for borrowing costs, surged last week after Fed governor Christopher Waller cautioned against rushing to cut rates. Yields’ climb continued after data on retail sales, housing starts and unemployment filings all beat economists’ projections. The 10-year U.S. Treasury yield finished the week at 4.145% after starting the year at 3.860%.

Traders are now betting inflation will average above 2.4% over the next five years, the highest level since November, based on swap contracts tied to the consumer-price index.

The Russell 2000 index of small-cap stocks—which gained 22% in the last two months of the year—is down 4.1% in January. Speculative stocks have taken a beating; both Rivian and Coinbase have lost more than 25% after rising during the Fed-pivot rally. A KBW index of regional banks, which added 31% in November and December, has slid more than 3%. Shares of real-estate and utility companies are down even more, also having surged in those months.

The Bloomberg Barclays aggregate bond index, which soared in the final months of last year, is down 1.4% to start 2024.

“People tried to front-run the rate cuts by buying long-duration assets, like tech stocks and bonds,” said Nancy Davis, founder of asset management firm Quadratic Capital Management. “What if the Fed doesn’t cut that much or that quickly? Those people get hung out to dry.”

The Atlanta Fed’s GDPNow model shows the economy likely grew at a 2.4% inflation-adjusted pace in the fourth quarter. That is nowhere near the conditions that have historically necessitated rates coming down 1.5 percentage points—which traders were betting on heading into 2024.

The extra compensation investors receive for buying high-quality corporate bonds over Treasurys is slimmer than before the Fed began raising rates, now around a percentage point. Credit spreads on junk bonds are similarly tight, signaling little concern over company defaults. Leveraged loans—used to fund private-equity buyouts or finance poorly rated companies—are in such high demand that companies are slashing their borrowing costs.

Some investors believe a strong economy could still boost stocks.

Sophia Drossos, an economist and strategist at Stamford, Conn.-based hedge fund Point72, expects robust consumer spending—and a proactive Fed—to help avert a recession and prop up corporate profits. The strong underlying U.S. economy “means risky assets can benefit,” Drossos said.

Not everyone is optimistic. Some fear new sources of inflationary pressure, such as trade disruptions from the Houthi attacks in the Red Sea and a drought in the Panama Canal.

And technical factors also could undermine the market gains. Interest-rate bets often represent investors protecting their portfolios against the risk of a recession or crisis that requires sudden rate cuts. Without a major slowdown, investors might remove those hedges, raising market rates. That could tighten financial conditions and disrupt stocks without any fundamental changes to the economic outlook.

But considering the strength of the economy, many doubt rate cuts will be as aggressive as investors hoped just a few weeks ago, threatening one of the rally’s biggest pillars of support.

“You’d think the wheels would have to come off to see that number of cuts,” said Fincher.

Every January, I usually purge old snail mail, clothes and unwanted knickknacks to start the year anew. This time, I focused on my digital spaces instead.

My virtual Marie Kondo-ing forced me to think about the indispensable apps and features on my devices—and on the flip side, the time thieves that make it hard to leave the couch. (Looking at you, YouTube.)

What did I learn? The most important thing we can do to improve our digital spaces is kill the wormholes. After culling apps on my devices, deleting Instagram from my iPad made the biggest impact. But there were many more.

I also learned that small tweaks—such as adding helpful shortcuts and setting up your screen only around essential apps—can make a difference. I’ve been spending less time on my devices, and I’m now more efficient at work. Here are some takeaways from the exercise that can help you turn distracting devices into time savers.

Digital decluttering

Cal Newport’s book “Digital Minimalism: Choosing a Focused Life in a Noisy World” inspired me to get rid of the junk on my phone and laptop. Clutter, even in digital form, is stressful, Newport writes. I could relate: I felt overwhelmed every time I turned on my devices.

Digital clutter includes unnecessary files on your computer desktop, promotional emails clogging your inbox and unused apps on your phone. I found that the most satisfying cleanse was clearing my phone’s default home screen—what I see as soon as I unlock the device.

An iPhone app called Blank Spaces (one-week free trial, then $14 annually or a $23 one-time fee) enabled the transformation. I picked my five most-important apps—Kindle, Signal, Messages, Maps and Docs—and let the app do its work. Blank Spaces replaced the usual grid of icons with an empty white background and large tappable text that can launch my chosen apps. I love the new Zen vibes and find myself mindlessly using my phone less often. If needed, I can still get back to my old layout by swiping left.

I spend most of my laptop time in a web browser, which is my most disorganised digital space. I am a terrible tab hoarder, and often have dozens open at once—something that makes my laptop slower.

One Tab, a free browser extension for Chrome, Safari and Firefox, has changed my hoarding habits. With one click, the extension closes all the tabs in an open window and saves the sites as a list of links on a dedicated page. It frees up memory needed for faster computer performance, and makes sure you don’t lose your links.

Timesaving shortcuts

Smartphone widgets are amazing. Instead of the tiny icons with the service’s logo, they’re bigger tiles that show you information like the current weather or what’s next on your calendar without having to open the apps.

My favourites include a multi-city world clock for managing colleagues in different time zones, a quick link to Google Translate’s camera function and a list of my tasks via the to-do app Twos.

On iOS, you can touch and hold any area on the home screen until your app icons jiggle. Tap the + button to look at all apps that have widgets available. You can also add a few to your lock screen to access information without opening your phone. And widgets can now be added to desktops on Macs running the latest software. On Android, touch and hold an empty space on the home screen, then tap Widgets.

You can take this timesaving even further with automations. Shortcuts is a powerful built-in app on iOS and Mac for creating custom workflows. For example, the Start Pomodoro shortcut triggers a 25-minute timer and enables Do Not Disturb for that period. I use the automation for short periods of focus. If you find the Shortcuts interface too intimidating, there’s a gallery with pre-made options.

Android users can set up automated routines with Google Assistant. Tasker ($3.49) is a more advanced—though more complex—Android alternative.

A souped-up clipboard

There are two benefits to having a clipboard manager. It saves everything you copy—that is, command + C on a Mac—so you don’t lose anything to copy-and-paste heaven if you accidentally use the shortcut on something else. It’s also a handy tool for quickly accessing often-repeated text.

The Copy ’Em Mac app costs a $15 one-time fee, and it’s worth every penny. It saves clipboard text and images on your device, and can create keyboard shortcuts for frequently pasted text, such as the short introductory paragraph I email people when reaching out for the first time.

If you’re on Windows, ClipClip is a good alternative. Chromebooks already save the last five copied items. Select the search or “Everything Button” + V to access copy history.

Apple’s Universal Clipboard is fantastic for copying-and-pasting between its devices, such as entering a code from your iPhone’s authentication app on your Mac. Enable Handoff in settings, then make sure the devices are signed in with the same Apple ID and have Bluetooth and Wi-Fi turned on.

Between Android and Windows machines, you can use Nearby Share (soon to be renamed Quick Share) to share text across those devices.

An AI helper

Some workplaces may be banning AI-powered chatbots, such as OpenAI’s ChatGPT and Google’s Bard, but they can shave hours off dreaded personal tasks.

The key to coaxing a high-quality response is starting with a specific, detailed prompt. Try: “Plan a three-course dinner for six people with easy gluten-free and vegetarian recipes. Identify any steps that can be prepared in advance and create a timeline for cooking the recipes. Arrange the ingredients in a list, organised by grocery store aisles.”

I love using chatbots for mixing up my workouts: “Create a five-day exercise plan for someone who is just getting back into shape,” and add any available equipment or necessary modifications.

Just remember, these systems can be wrong, so you may need to double check their work. Still, you’ll have plenty of freed-up time to ask ChatGPT what to binge-watch next.

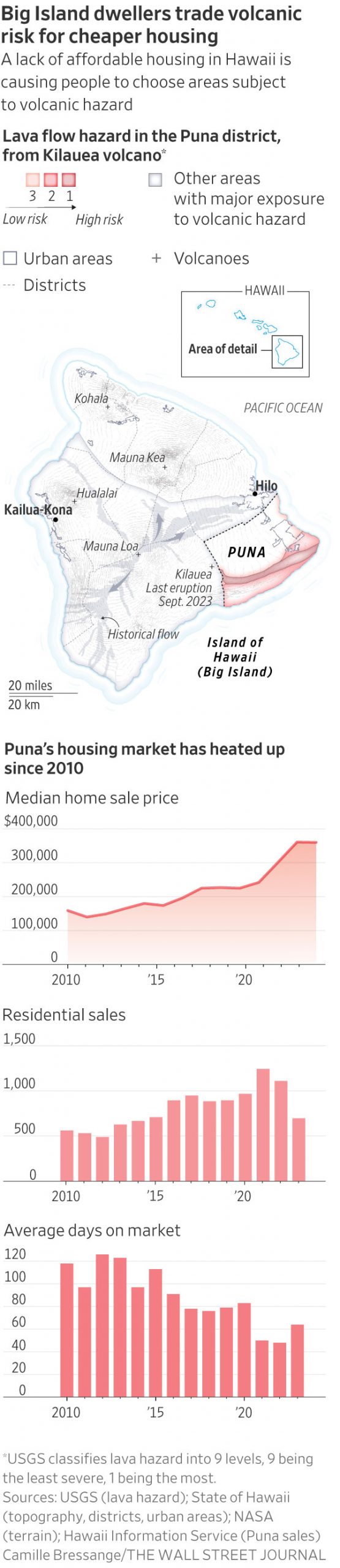

PUNA, Hawaii—In 2018, a large volcanic eruption spewed lava, rock and ash into the middle of a subdivision here, gobbling up more than 700 homes and displacing thousands of residents in a slow-motion disaster. Today, it is Hawaii’s fastest-growing region.

Land in an active lava zone, it turns out, is relatively cheap. Lured by a shot at attainable homeownership in paradise, island dwellers and mainland transplants alike have been flocking to this area in the shadow of Kilauea, driving up prices in the Puna District. Still, the area remains one of the last affordable refuges on the cheapest island in Hawaii, America’s most expensive state.

“In terms of the last bastion of affordability, Puna is it,” said Jared C. Gates, a Realtor who was raised on Oahu and came to the Big Island for college in the 1990s. He purchased his first home in 2005, a modest fixer-upper in Puna, on his salary as a waiter.

Over the past few years, he has been getting more business in Leilani Estates, the neighbourhood where the 2018 eruption began.

None of the homes that were inundated by lava have been rebuilt. Many homeowners have sold their properties to neighbours or the county in a federally funded buyback program, but that land remains vacant for now. The land has been so transformed that it is hard for remaining owners to know even where their property begins and ends.

“It took out roughly a third of the subdivision; totally surreal,” Gates said last fall. “And houses are selling there again.”

Among Gates’s listings that day was a three-bedroom, two-bath home with lush landscaping, two blocks from the mile-wide lava field where heat and steam still radiate from vents in the petrified landscape. “It’s a beaut,” he said. “It will sell.”

Three weeks later it did, for $325,000, cash.

The story of how serene-looking slices of suburbia came to inhabit an active volcanic rift zone is well-known here. In the 1960s, land speculators—aided by a new county government hungry for tax revenue—bought thousands of acres and carved it into lots of an acre or more that were snapped up by investors.

There were virtually no requirements that developers pave roads, place utility lines or build other essential infrastructure. To this day, there is no wastewater treatment plant or hospital. Many of the district’s 51,000 residents rely on filtered rainwater and cesspools to dispose of sewage.

Early buyers included Native Hawaiians looking for an affordable place to call home and mainland hippies intent on off-grid living. As home prices rose in Hawaii and across the nation, however, more working families and mainland retirees went hunting for deals on the Big Island.

County Councilwoman Ashley Kierkiewicz, who represents Puna, said rush-hour traffic on the rural, two-lane highway that connects Puna to Hilo, the county seat roughly 20 miles away, is so bad that she leaves her home 1.5 hours early to get to work.

County officials say rules tied to federal funding bar local government from building affordable housing in lava zones 1 and 2, which are the riskiest and make up most of lower Puna. State law also prohibits them from spending most local money on private subdivisions, meaning that roads are largely maintained by owner associations.

Hawaii County Mayor Mitch Roth said that while the county has added a new firehouse, police station and park facilities there in recent years, the county has limited funds to make major investments in high-risk areas.

“Are we going to invest public money in a high-risk place…knowing that whatever you build could be taken out by lava at any time?” said Roth.

The lack of some modern conveniences has scarcely slowed the flow of newcomers.

Like many places in the U.S., an influx of remote workers during the pandemic has helped send the housing market here into overdrive.

Among the recent arrivals are David Booth and his partner, Juan Polanco. The former Phoenix residents had been brainstorming tropical locations where they could slash their living expenses and ease into retirement.

“The attraction to the Big Island was affordability,” said Booth, 61, who now works remotely. He and Polanco, 59, paid cash for a 1,500-square-foot home that had been split into three units with separate entrances. “You can’t have this on any other island for this price point.”

The property sits on a 1-acre lot in Hawaiian Paradise Park, a subdivision located in the less-risky lava zone 3. Homes with repeated sales in the neighbourhood have seen a nearly 800% appreciation in price since 2000, according to data from the University of Hawaii Economic Research Organization.

Properties in lava zones 1 and 2—some with sweeping oceanfront views—were far cheaper, Booth said. In the end, the risk of losing their nest egg to a natural disaster, and the difference in insurance rates, were deal breakers.

They are getting used to bringing in their drinking water and dealing with vicious fire ants. The slow-paced lifestyle and prospect of early retirement are worth it, he said.

They have listed the two other units as vacation rentals, and their first guests arrive next week.

“We are overwhelmed with the amount of beauty here and just how much more relaxed we feel,” said Booth. “We’re building a whole new life here.”

Three years ago, Travis Edwards, 48, was driving delivery trucks and living with his mother in Southern California’s Inland Empire.

He was sick of the traffic, wildfires and car thefts, he said. Upon retiring, his mother sold her house and paid cash for a 1-acre lot with two units in Leilani Estates, surrounded by avocado and citrus trees. Lava insurance rates in lava zone 1, the riskiest area that encompasses the entire subdivision, were so high that they simply stopped paying for it, he said.

He mostly shrugs off the dangers, reasoning that they would be reckoning with fires and earthquakes on top of a lower quality of life back in Southern California.

“It’s just paradise,” said Edwards, who now drives limousines part-time. “The rest of the world doesn’t exist when you’re here.”

Rising prices on the east side have left Puna native Chantel Takabayashi feeling stuck. A single mother of three, she works 16 hours a day as a state prison guard in Hilo. She would like to buy a home closer to work and better schools but has been priced out of most neighbourhoods she has considered.

“I make pretty decent money and I work long, endless hours, and I still can’t afford better housing,” she said.

A home in the Kalapana Gardens neighbourhood.

Liz Fusco, who manages more than 100 rental properties for Hilo Bay Realty in Pahoa, said that during the pandemic, she saw three-bedroom homes in parts of Puna that once fetched $1,500 a month rent for as much as $2,300.

Most of the applicants were mainlanders, she said, with stellar rental histories, plenty of income and pristine credit. Units that would typically take more than a month to rent were getting leased in three days.

Tina Garber, who has lived in the Puna area for 21 years, has been displaced twice in the past 18 months after the homes she was renting went up for sale.

Currently, she is paying $750 a month—three-quarters of her monthly income as a housecleaner—for a 400-square-foot studio surrounded on three sides by cooled lava. Her landlord just told her it will be listed for sale in April.

“People that come over here with money, they do not realise that it is so hard to make it here,” Garber said. “They think, ‘Oh, a good deal in Hawaii.’ But it puts a lot of pain and suffering on local folks.”