A Los Angeles nonprofit was given government land in January 2007 to build a few dozen units of affordable housing. They’re finally hoping to open the building next year.

Lorena Plaza, a 49-unit development rising in the predominantly Latino neighbourhood of Boyle Heights in eastern Los Angeles, is taking longer to complete, a city official said, than practically any other residential building this size in the history of Los Angeles.

The 17 years of false starts and delays are an extreme instance of how difficult it has long been to build affordable housing in California—for both the homeless as well as lower and middle-income workers—and in other states with complex regulations and high costs.

The development has faced nearly every hurdle that California laws allow opponents to place in the way of affordable housing. Approvals by politicians and commissions took years, often held up by a single determined opponent on the city council. It took the developers more time to win over skeptical neighbours who were particularly opposed to nearby housing for the mentally ill and homeless. Financing hurdles and other costs piled up along the way. Construction finally began about a year ago.

In California, affordable housing developers typically abide by a host of requirements when they take public subsidies, such as tougher energy-efficiency standards and higher wages for construction workers. They often need to build amenities such as offices for social workers and transit-boosting features such as bike storage.

Even home builders who are sympathetic to these priorities say those same objectives undermine the state’s ability to produce enough affordable housing. That means California will continue to suffer stubbornly high rates of homelessness that plague the Golden State and are evident on the tent-filled streets of cities like L.A.

“We’re really committed to things like climate change and we’re very committed to transit-oriented development,” said Linda Mandolini, president of Bay Area-based Eden Housing, a nonprofit low-income housing builder. “But those goals don’t come for free.”

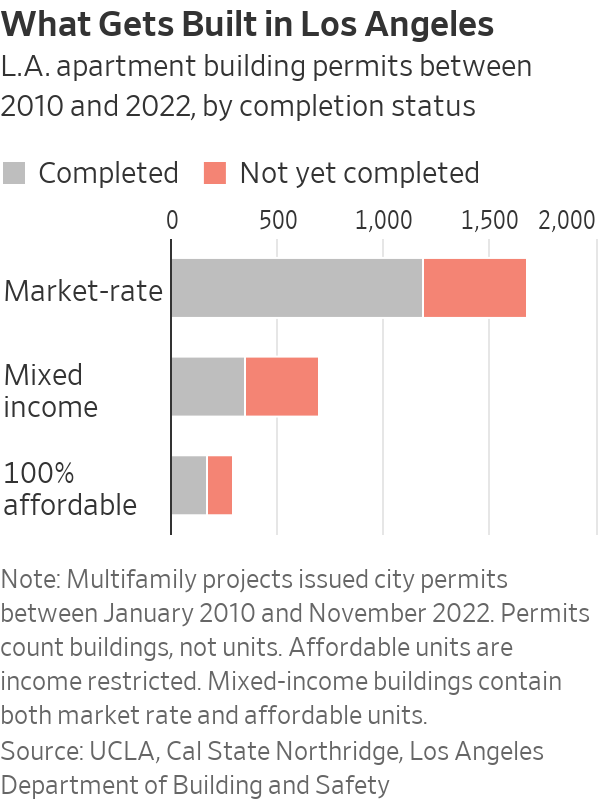

Housing costs and homelessness have become the top political issue in the state, prompting officials to set ambitious goals to build more housing, faster. Los Angeles is aiming to construct more than 450,000 new homes by 2029, a feat that would require five times as much construction as occurred in the previous decade, according to a May report from researchers at the University of California Los Angeles’ Ziman Center for Real Estate and California State University Northridge.

Los Angeles Mayor Karen Bass has pointed to the delays with Lorena Plaza as an example of what the city is trying to fix. The mayor is expediting permits for projects in which all of the units are considered affordable and cutting other red tape that has sidelined projects.

“How on earth could we expect to house 40,000 [homeless] people if we continue to do business as usual?” the Democrat asked in a speech at the development’s construction site last year.

There are still serious impediments to building enough housing in Los Angeles and the state. Existing subsidies that fund affordable housing construction are oversubscribed. And cities keep looking for ways to block new housing, market-rate or affordable.

The Bay Area suburb of Woodside, for example, last year tried to declare that its entire city was a mountain lion refuge to prevent apartment development. The town, which later reversed the decision, didn’t return a request for comment.

Affordable housing faces hurdles outside of California, too. In New York City, a developer’s plan to build low-income apartments at the site of a community garden in lower Manhattan has been held up for a decade by city review processes and lawsuits filed by opponents. In Dallas, a mixed-income apartment complex planned for an empty field in the northern part of the city was delayed for more than three years by deed restrictions that allowed neighbouring property owners to dictate land use.

An apartment building takes an average of four years to build in L.A., according to a UCLA and CSU-Northridge analysis of building permits from 2010 to 2022. Two-and-a-half of those four years come after the approvals process.

About 36% of projects that received permits in California between 2010 and 2022 had not yet been completed, according to UCLA.

“Thinking about building in a city like Los Angeles and dealing with the politics, navigating the bureaucracy, it’s the last place I want to be,” said Caleb Roope, chief executive of the Pacific Companies, a West Coast affordable housing builder based in Idaho.

California Gov. Gavin Newsom is pushing changes at the state level, as are the mayors of other cities where housing construction has been painfully slow and homelessness has risen.

In San Jose, Calif., the average cost to build just one unit of low-income housing shot up by 24% in 2022 alone, hitting a new high of $938,700, or roughly what it costs to buy a three-bedroom bungalow there, according to an October report commissioned by the city.

San Francisco permitted 856 housing units this year through October. New Braunfels, Texas, which is one-eighth the size of San Francisco by population, permitted 1,940 units in the same period, according to data compiled by the U.S. Department of Housing and Urban Development.

In Los Angeles, Lorena Plaza, if all goes as planned from here, will open in the late summer. Its 49 units will consist of studios up to three-bedroom apartments. They will measure between about 420 and 1,050 square feet and feature full-size kitchens. The rentals will be priced so that people making less than 50% of the area median income can afford them. The units cost $34.2 million to build.

The project’s wood beams are stacking up in Boyle Heights. It’s a neighbourhood that over the past century has made homeownership possible to a rotating cast: Irish and Jewish immigrants at the turn of the century gave way to Black residents barred from buying elsewhere, before becoming the predominantly Latino neighbourhood it is today. Vendors hawk elote, tamales and flowers on street corners.

The neighbourhood has also seen gentrification in recent years, which has turned this barrio into a hotbed of housing activism. On the surrounding blocks, taco trucks coexist with $45 men’s haircuts. A Starbucks drive-through sits on what was once a Unocal service station and the historic Boyle Hotel, which once boarded mariachi musicians, now houses a La Monarca, the local chain of upscale Mexican-American bakeries.

Some 74% of the neighbourhood’s residents are renters, and for more than two decades, rents have risen faster than in the rest of Los Angeles, according to one city government-commissioned study, amid an influx of higher-earning residents.

In 2007, A Community of Friends, a nonprofit developer known as ACOF, proposed to build permanent supportive housing, a type of project designed for low-income people with specific needs. In the case of Lorena Plaza, it meant some units would be set aside for those who had experienced homelessness or mental health issues, and who would rely on services such as social work and healthcare provided by on-site staff.

The Los Angeles County Metropolitan Transportation Authority agreed to provide the land, but was slow to make it available, in large part because it was being used as a staging area during the construction of a train line. A global financial crisis further derailed plans. By the time the economy began rebounding in 2012, the deepest troubles for the 49 could-be apartments were setting in.

The city councilman representing the neighbourhood, Jose Huizar, had broad powers to delay projects on his turf. To get a city subsidy, the developers would need a signed letter from Huizar, who sat on the MTA board and remained opposed to the project for years.

Dora Leong Gallo, executive director of ACOF, recalled a nervous 2013 meeting with Huizar’s staff. Huizar’s staff wanted more commercial space, Gallo said. Once that was satisfied, they requested the approval of the Boyle Heights Neighborhood Council, a community advisory group.

“He moved the goal posts,” Gallo said.

Huizar is currently awaiting sentencing after pleading guilty to corruption charges unrelated to Lorena Plaza. His attorney said that “asking for additional commercial space and support from the neighbourhood council seem not only like routine asks, but responsible ones.”

In a series of heated community meetings, some area homeowners and renters including vendors at El Mercado, a bustling, three-story indoor market next door, chafed at the idea of sharing the neighbourhood with mentally ill and homeless residents.

“They’re trying to bring mentally ill people to put our children at risk,” Pedro Rosado, the owner of El Mercado, said during a 2013 hearing. Rosado died in 2015 and his children, Tony and Marlene, continued his appeals. They didn’t respond to requests for comment.

In 2015, the development got a boost after the neighbourhood council voted 15-1 to let ACOF proceed. It took about another year to receive city approval on all the necessary zoning and environmental reviews.

State law provided an opportunity to stall Lorena Plaza further. The Rosados appealed the project’s city-approved environmental review, claiming it was too dense for an already-overcrowded area, according to the filing.

A landmark state law called the California Environmental Quality Act, passed in 1970 and signed by Gov. Ronald Reagan, allows any opponent to use appeals to slow down development if they claim environmental reviews are flawed. In Los Angeles, appeals are heard by the city council’s Planning and Land Use Management Committee. That body was chaired by Huizar.

“He had double power,” said Jose Torres, the project manager for Lorena Plaza at the time. “One as a council member of his own district, and the other as the chair of PLUM.”

The committee didn’t schedule a hearing on the appeal for more than a year. When the project did get a hearing, Huizar sided with the Rosados, saying an abandoned oil well on the site posed a potential hazard.

By 2017, California’s housing crisis was worsening. Economists estimated there was a shortage of three million homes statewide. On the campaign trail, gubernatorial hopeful Newsom was vowing to spearhead an effort to alleviate homelessness and slow down home prices by building 3.5 million homes within eight years. While housing production has ticked up in recent years, it still sits well below half the pace needed to hit that figure.

Media attention zeroed in on the Lorena Plaza project and its years long saga, prompting the Chamber of Commerce and the United Way to rally behind it. In early 2018, Huizar called up the Los Angeles Times to say he had changed his mind after the developer made concessions and would push for the project’s approval.

The owners of El Mercado then turned to the courts, filing a lawsuit alleging ACOF didn’t properly address potential soil contamination. The case dragged on until ACOF and the business owners settled in 2020.

By 2021, when the Lorena Plaza developers secured all the necessary funding, the project’s costs had shot up by $9 million, or about one-third, in the five years after it first received approvals to build, Gallo said.

“It’s unfortunate what happened, but I think it’s very illustrative,” Gallo said. “I think a lot of things have changed as a result of this particular project.”

Much of what stifled construction of Lorena Plaza likely wouldn’t have happened now due to recent law changes. Developers no longer need a letter of support from their city council member to receive affordable housing funding.

Environmental appeals have to be heard within 75 days. Zoning approvals for affordable projects, which took more than a year at Lorena Plaza, are now happening as quickly as a few months-time under a Mayor Bass executive order.

David Aghaei, co-founder of Eleos Ventures, a developer with a pipeline of more than 20 all-affordable housing projects in Los Angeles, said the changes have significantly improved the timeline for four of his larger projects. One of them, which will bring 222 units of affordable housing to South Los Angeles, received planning approvals in five months. Historically, Aghaei said, that could have taken as long as two years.

The new rules mean Lorena Plaza may permanently hold the title for perhaps the city’s longest-running development. ACOF plans to start taking applications from prospective tenants in the spring.